When Geopolitics Stalls and Macro Speaks: Why Stocks Stay Elevated Without an Iran Deal in Sight

TL;DR: The headline of market records with no Iran resolution is not a paradox when you strip geopolitics down to its market-usable signal. Investors are assigning unresolved regional risk a finite discount rate while anchoring on near-term liquidity, earnings, and a hard macro calendar. In a week loaded with high-sensitivity releases, data-driven repricing can outweigh headline noise quickly. The edge is to treat every major event as either a probability shift (geopolitics) or a valuation-shift input (macro, demand, inflation); only the latter tends to force fast portfolio changes. For finance readers, this means disciplined positioning around cash-flow uncertainty and duration is still more important than reading every diplomatic headline. Why “No Iran Resolution” Does Not Equal “No Market Move” The phrase “no resolution” sounds like a threat to stability, but markets do not require complete geopolitical clarity to continue upward drift. They need, instead, a lower-risk path for near-term cash flows. If financing costs and credit channels remain intact, and if corporate earnings still look defensible, equity risk assets can hold record levels even when headlines are unresolved. A useful lens: markets can tolerate friction, even ongoing uncertainty, when it is familiar and already reflected in positioning. What changes this dynamic is when uncertainty becomes a forcing event—through sanctions impacts, new supply disruption, energy rerouting pressure, or policy response risk—and then only later, through real flow effects. In short, geopolitical risk becomes “priced ambiguity” when it is uncertain but slow-moving. It turns into “priced shock” only when there is a credible path to immediate earnings, margin, or liquidity impact. What Is Really Setting the Tone: The Macro Clock The stronger signal in the near term is not symbolic headlines but the macro calendar. This can be seen in two ways: what moves expectations, and what confirms or denies them. Price Drivers Are Usually Flowable Variables The market can act on rates expectations, inflation trend clues, and payroll-linked labor data because those inputs map directly into corporate margin assumpt

Why Records Hold Without a Geopolitical Fix: How June’s Data Calendar Rewrites Risk Pricing

TL;DR: Markets can stay elevated even while geopolitics looks unsettled because price-setting is increasingly governed by data-driven expectations, not headlines alone. The unresolved Iran thread from the candidate headlines still matters, but as long as policy reaction functions remain intact, equities can trade near record zones. In the coming week, finance and business teams should treat the macro calendar as the primary control point, separate headline noise from pricing signals, and stress-test portfolios for liquidity shocks, not just headline downside. This creates a practical edge during uncertainty without forcing a binary bullish/bearish call. Why records can hold while diplomacy stalls A headline can sound dramatic and still fail to move valuations if it does not alter expected policy paths. The first candidate headline signals that broad market levels are still high despite no immediate geopolitical resolution. In practice, that typically means participants are assuming that any adverse development will be priced into risk premia before fully derailing growth and earnings assumptions. The same reaction appears when participants view conflict as a manageable, uncertain input rather than a new macro regime. That distinction is crucial: an unresolved issue changes the distribution of outcomes, while a changed policy regime shifts valuations faster and deeper. Diplomacy as a variable, not a valuation engine If diplomacy were the primary driver, markets would likely exhibit abrupt repricing each day. Instead, many participants behave as though the Federal Reserve and economic data remain the binding constraints. The J.P. Morgan-linked headline framing suggests a persistent re

No Iran Deal, No Pause: Why Equities Can Hold the Line Into This Week’s Data Tests

TL;DR: This week’s setup is less about one dramatic headline and more about process: whether fresh U.S. data lifts or drains confidence while a geopolitical story remains unresolved. The key implication from both source themes is that investors may continue discounting uncertainty if earnings resilience, inflation trend stability, and liquidity conditions stay supportive. That means opportunities come from positioning and risk rules, not from trying to predict geopolitical theater. Build plans around scenario-based reactions to data and valuation stretch, with strict downside triggers. The market’s current paradox: record levels, unresolved diplomacy The two headlines frame a familiar contradiction. One asks what to watch in the data calendar; the other asks why equities sit near record highs even without a formal Iran resolution. Together, they imply this: markets are increasingly event-order aware. Instead of anchoring on a single geopolitical outcome, they are weighing the sequence of upcoming information. Kiplinger-like checklists for the week emphasize what is actually measurable—new macro prints, sentiment, and policy cues—while the J.P. Morgan framing highlights that a missing headline can stop being a headline if nothing else changes in risk valuation. In short, uncertainty is being tolerated unless fresh facts challenge the assumptions behind cash-flow and rate expectations. Why records can keep climbing without a headline The missing event is not the same as bad fundamentals When a major geopolitical item stalls, markets can still rise if the incremental risk premium for that uncertainty narrows. Two conditions help this happen: Balance-sheet quality of major institutions remains stable enough to absorb volatility. Corporate guidance and hiring decisions continue to suggest demand and margin resilience. The first point is usually visible in credit conditions, financing accessibility, and earnings guidance discipline. The second is visible in revenue commentary and capex willingness acr

AI Returns Meet the Payrolls Question: Reading This Week’s Data as the Real Test of AI-Linked Valuation

TL;DR: The week of June 15-19 looks less like a headline-chasing sprint and more like a calibration exercise for capital markets. Macro data is likely to stress-test AI enthusiasm by forcing investors to separate durable business economics from narrative momentum. The winners will be firms where AI clearly lifts operating efficiency and recurring cash flow, not just headline growth. In a higher-rate environment, the critical question is not whether AI is exciting, but whether it improves free cash generation faster than macro data raises financing and risk premiums. The market is running a two-track exam The first track is macro timing. Economic print season around this week is shaping the risk floor: employment momentum, inflation trends, housing-sensitive indicators, and related financial conditions. These are the inputs that decide whether liquidity stays easy enough for fast-moving AI narratives to remain bid. The second track is business quality. Even with strong AI demand, investors increasingly ask a stricter question: can firms compound margins after accounting for data infrastructure, compute intensity, and scaling costs? If the macro signal weakens risk sentiment, this second track can dominate. At a strategic level, the week acts like a stress test where valuation headlines are repriced by hard numbers from labor, price stability, and credit conditions. That is why the same AI story can look wildly different from one day to the next: the macro scorecard does not reject innovation, it simply changes discount rates and capital allocation priorities. You can think of it as a market-level credit desk for ideas. Why the AI narrative can look strong while balance sheets stay weak The candidate headline about an AI boom “carrying more than investors admit” suggests a familiar market mechanism: some upside gets locked into valuations before accounting follows. For finance and business readers, this is not bearish; it is a demand for proof. The hidden side of AI growth AI programs often look suc

Beyond the Tension: Why Equities Stay Elevated as Geopolitical Risk Becomes a Side Bet

TL;DR: Two separate messages are arriving this week. The calendar signal is that investors are focused on high-frequency economic inputs, while the geopolitics signal is that conflict headlines are no longer treated as a direct trigger for immediate de-rating in equities. Even if a resolution is still absent, markets can remain constructive when inflation, growth and liquidity conditions look manageable. For finance and business audiences, the practical takeaway is to stop asking whether this week proves a trend and start pricing whether each incoming data point changes risk/reward versus what is already priced into corporate cash-flow expectations. Why these two headlines frame the same decision problem The first headline from Kiplinger points readers toward a near-term economic agenda for June 15-19, while the J.P. Morgan headline highlights a classic market paradox: stock indices at records without a fresh diplomacy breakthrough. Taken together, they imply that the market is distinguishing between narrative intensity and data quality. The macro calendar is now the first-order filter The financial press cycle this week is not just about “good versus bad” news; it is about sequencing. When institutions read a weekly economic preview, they prioritize indicators that affect discount rates, earnings revisions, and liquidity expectations before they revisit geopolitical headlines. In plain terms, they are treating uncertainty as persistent but manageable while waiting for hard numbers to justify repricing. In that frame, jobs, inflation expectations, and guidance from major central banks matter more than headline conflict slogans. The record-high equity message is a valuation test, not a certainty test [J.P. Morgan’s note on market resilience](https://news.google.com/rss/articles/CBMizgFBVV95cUxNQ3o0YTF6TDN4XzFLLXRCOFFJelJRWjBiY1dRV0hiZXI3NUdnVm5zcVRibDNrODd2UjFLTDhieExrVFZaUE1rUWdYZlZjVU1wbW40ZENodDQ2cGtkNkVZZ3Y0VGptRXlJOW9zWW5RcVFfNDN1SmlpZ2hfTFVDUmh5RmJ2MUN1a2pSdHVmanZLaHVuQ3BQQzB0eVZyMkZlWEx1UE5GY3h

Data Windows and Rocket Capital: Why June 15‑19 May Reshape AI-Related Risk Pricing

TL;DR: This week is likely to be a valuation stress test disguised as ordinary macro noise. The data calendar from June 15‑19 sets a floor for risk sentiment, while the SpaceX IPO frame puts a bright spotlight on AI-linked growth stories. For investors and readers tracking finance, the real test is whether AI narratives can absorb weaker macro signals without blowing up unit economics. If economic releases improve confidence, AI risk assets may re-rate on perceived resilience; if they fail, multiple discipline and cash discipline will dominate, and people-heavy, business-use-ready execution narratives will matter more than marketing velocity. Why this week is a pricing hinge, not a simple news cycle Markets rarely move only on what is announced; they react to what can be monetized after the headline fades. A weekly data watch like the one outlined by Kiplinger, the market is usually deciding two things at once: immediate cyclical direction and the quality of downside protection in long-duration growth names. The first question is not "AI up or down" The first question is whether inflation, labor, and growth data support stable discount rates and borrowing assumptions. Investors may still own AI stories, but their pricing uses discount rates first and narrative later. The second question is whether companies can prove demand intensity Even in a positive macro backdrop, capital markets now punish the model that cannot explain margin durability, especially if capital intensity rises with competition. This is why a calm macro print can still coincide with selective downgrades in AI-related equities. AI, space, and the balance-sheet lens after the IPO conversation The Guardian framing suggests a broader shift: public market appe

AI Hype Meets the Payroll Clock: Why June 15–19 Data Could Reprice the AI Story

TL;DR: This week’s finance outlook is less about one scary macro print and more about how quickly narratives can flip: if data on inflation and jobs points to softness, credit conditions likely ease; if it surprises to the upside, AI-fueled risk appetite cools. In either case, the central question is not whether AI still exists, but which sectors can justify expensive valuations with durable cash flow once expectations meet the next earnings and liquidity cycle. Timing from economic data and confidence in AI monetization are now intertwined. Why This Week Feels Like a Decision Fork in the Road The headline list sets up a tension investors keep facing: one story is short-cycle macro, the other is long-cycle sentiment. A weekly economic-data calendar puts immediate pressure on policy expectations, while AI-euphoria concerns force markets to ask whether current multiples are priced for uninterrupted expansion. These aren’t separate debates; they interact directly. The Kiplinger lead-in for June 15–19, the practical implication for investors is simple: every payroll-style or inflation signal can tighten or loosen the market’s discount rate assumptions, often immediately. At the same time, BIG’s question about an AI bubble popping reframes risk: is AI a new productivity regime, or just synchronized future optimism? A 2x2 Framework for the Week Ahead Scenario A: Data Softens and the AI Multiple Regains Breadth If inflation and labor data drift lower than expected, two consequences usually follow: rate fears cool and duration risk rises. This is where AI equities often revive first, but n

From Hype Cycle to Balance Sheet: Why the Real AI Story Is in Who Controls Cashflow, Not Just Narratives

TL;DR: The two headlines point to the same core lesson: AI is moving from a sector story into a household and business balance-sheet story. The “AI bubble” question is not only about whether valuations fall, but about who still produces dependable margins when sentiment shifts. The likely inflection is not a single chart crash, but a re-pricing of cash-flow quality, governance, and who can convert compute into defensible recurring revenue. If you publish after AI headlines, your edge is portfolio architecture, not prediction timing. The headlines are not opposites The two source themes seem contradictory at first glance: one asks what a collapse would look like, another says major public offerings like SpaceX will bind financial futures to AI. Together, they describe both ends of the same market contract. The AI-bubble framing is a stress question, while the IPO narrative about SpaceX and AI-linked macro exposure is a structural claim about capital formation. A shared market logic Both signal that investors now price AI through expectations of durable advantage and macro spillover. In a benign cycle, that supports multiple expansion. In a risk-off cycle, it increases drawdown. The practical lesson for finance teams is simple: do not build a thesis on one-time story lifts; test what happens to valuation and cash cost if AI sentiment compresses. Why this matters more than ever for business readers For finance and strategy leaders, this is no longer a “tech coverage” conversation. It is treasury, capex, and forecasting work. If AI assets become default inputs for productivity, then revenue

Beyond the Headlines: Why 2026 Market Direction Depends on Policy Execution More Than Political Theater

TL;DR: The 2026 market theme appears less about whether one headline is good or bad, and more about whether policy intentions are translated into real behavior: bank lending posture, capital spending, and payroll willingness. In a Trump-era backdrop, investors can overreact to rhetoric while waiting for corporate guidance, budget implementation details, and economic releases to settle. As a practical takeaway, separate narrative noise from credit-channel and earnings-channel signals. That distinction helps readers build resilient investment decisions even when week-to-week headlines are loud, contradictory, and intentionally volatile. The core thesis: from political noise to operational signals The candidate finance theme suggests a familiar setup: market participants are trying to infer where policy will land before policy actually lands. The key correction is to avoid treating “speech risk” as equivalent to “policy risk.” Speech risk moves momentum intraday; policy risk changes cash flows over quarters. When Trump-era policy is in the air, headlines often amplify uncertainty around trade posture, regulation, fiscal rules, and public-sector incentives. But equity valuation still converges on three hard datapoints: How quickly lenders reprice risk. How aggressive management remains on capex, hiring, and buyback guidance. Whether consumers and businesses can still access affordable credit in a normalized inflation/interest-rate environment. This is why a good macro watchlist in 2026 starts with execution friction, not rhetoric. The U.S. Bank piece on market drivers under Trump. What to track now: three layers of macro transmission A weekly economics lens matters because it gives cadence, but it is not the only layer. You need a layered read: mac

From AI Buzz to AI Balance Sheets: How to Value the Next Wave Without a Bubble Premium

TL;DR: Markets are not debating whether artificial intelligence exists anymore; they are debating whether AI hype can convert to durable, scalable cash flow. The two current headlines—one warning about an AI bubble and another about a massive SpaceX IPO—are connected by one thread: investors are now being asked to fund expensive infrastructure bets before returns are fully proven. For finance readers, the edge is to separate narrative from unit economics, price in how fast sentiment can reverse, and buy exposure only where AI demand is linked to recurring operating leverage, not just optionality. Why the bubble question is no longer rhetorical The question in “What Would It Look Like If the AI Bubble Popped?”, people are not only asking if we are in a mania—they are asking what breaks first: funding availability, valuation discipline, or the revenue models that justify high multiples. This is a healthier framing. When markets transition from growth-at-any-cost to margin scrutiny, the first thing to watch is balance-sheet leverage and spending commitments. AI enthusiasm can justify high beta as long as equity and debt markets remain liquid. When macro conditions tighten, the weak links are usually: over-hyped implementation timelines, over-committed capex, and revenue forecasts that depend on sustained enterprise optimism rather than signed contracts. Sentiment cycles now reward optionality less than survivability In prior cycles, investors were often paid for owning a “winner takes all” narrative. In AI, optionality still matters, but the risk profile is different. You are paying today for chips, clusters, data workforces, and integration cycles that have long lead times. If the top-down narrative weakens, the market often reprices these commitments based on near-term cash burn and dilution risk first. The hidden accounting of AI upside The key mistake is to confuse gross AI spending with net earnings potential. Headlines can make every AI-re

AI Multiples Without Geopolitical Peace: Why Margin Quality Beats Headline Drama

TL;DR: US equities can stay near record highs even when a geopolitical story like Iran remains unresolved because investors are increasingly pricing firms on forward AI productivity, not only headline risk. But this is not blind optimism; markets are rewarding evidence that AI spending produces repeatable cash-flow upgrades. The central test is no longer whether AI is exciting, but whether it raises margins and retention in a durable way. In practice, the winners are companies that can turn model deployment into lower unit costs, higher pricing power, and stronger balance-sheet resilience while competitors chase the same narrative without execution. Context: Two headlines, one valuation dilemma The first headline says stocks are at historical highs despite no Iran resolution. The second says the AI boom may be stronger than most investors admit. Put together, this is less a contradiction and more a lens shift. Investors are separating immediate political uncertainty from long-dated earnings power. If this sounds like narrative fatigue, it is not. It is a specific reallocation of what gets paid for: certainty of conflict has moved from price-driving to risk-offsetting. Companies with clear AI operating leverage are treated as “durable demand,” while those with weak execution remain narrative-only. You can see this framing in the J.P. Morgan headline context. What changed in the market reaction When risk is geopolitical and unresolved, the market usually asks two questions: Is the probability of escalation rising? And can firms absorb the downside without hitting cash flow? If earnings calls continue to show expanding software margins, disciplined capex, and retained demand, the answer to the second question can be reassuring. The market as a spread versus a reactor Stocks are not saying “nothing bad can happen”; they are sayi

AI Liquidity and Geopolitics: Why the Tape Keeps Climbing Without a Green Light

TL;DR: Global equities can stay near record highs even while Iran policy is unresolved when AI continues to anchor expectations for durable earnings growth and investors treat geopolitics as a manageable risk variable instead of an immediate break in cash flow. The key is this: if valuation support comes from AI-driven productivity stories, firms that can compound margins may outperform, while those dependent on fragile demand or leverage become the first to absorb the geopolitics discount. For institutions, the edge is less in predicting headlines and more in stress-testing earnings sensitivity, financing flexibility, and regional risk transmission through your portfolio exposures. (Source context: Morgan Stanley and the JPMorgan framing. Why AI Momentum and Geopolitical Friction Can Coexist in the Same Market Tape The two headlines describe a market with competing narratives: strong AI momentum and unresolved geopolitical tension. In public risk-taking terms, this is not contradiction—it is a regime shift in what investors reward and what they merely monitor. When a theme is tied to long-cycle capex, productivity, and margin durability, it receives a higher valuation floor. Geopolitical concerns, by contrast, are often priced as a conditional haircut unless they directly impair demand, credit, or logistics in near-term earnings guidance. The Morgan Stanley framing suggests AI is not only a sentiment trade but increasingly a business model transition. At the same time, JPMorgan’s question about record highs without Iran resolution is a reminder that “headline peace” is not the only path to upside participa

AI as the New Market Floor: Why Stocks Can Stay Elevated Without a Geopolitical Cure

TL;DR: Markets are treating AI as a structural growth argument, not a speculative side story, while Iran headlines without policy closure are increasingly being priced as headline noise. The result is a split market: investors are rewarding cash-flow visibility and AI efficiency multipliers, yet staying sensitive to liquidity, earnings durability, and scenario shocks. The edge this year is to stop trading every headline and instead build portfolios that survive both high-volatility and high-confidence AI demand environments. Why AI Becomes a Market Floor Instead of a Bubble Morgan Stanley’s commentary on AI momentum suggests markets are discounting long-run margin expansion and productivity upside. A practical reading is that buyers are no longer bidding on “AI the idea” but on AI’s expected impact on margins, software demand, and capital efficiency. In practical terms, that makes valuation gaps hinge on execution quality, not merely on sector label. The AI Story Is Now a Cash-Flow Filter For finance leaders and investors, this is important: broad AI demand is no longer enough. The market is rewarding firms that can show repeatable, high-return deployment at scale. This means clean unit economics, defensible data advantages, and predictable subscription or usage retention. AI-heavy spend without margin expansion is now easier to punish than a few years ago. Why Headlines Are Not the Same as Theses The Morgan Stanley framing of global AI momentum fits a pattern we keep seeing after every major macro scare: broad risk-on flow returns quickly when firms can defend earnings power. That does not mean complacency is safe; it means the market has raised its hurdle for what counts as dangerous. Why the “No Iran Resolution” Narrative Is Usually Overpriced J.P. Morgan’s question on record highs without an Iran resolution captures a real investor tension: how much geopolitical ambiguity can risk assets absorb? Empirically, markets often price probabilities of policy outcomes long before headlines announc

AI as the Market's Engine While Diplomacy Waits: Why Records Can Hold Without a Iran Settlement

TL;DR: Two recent market commentaries point to a market process that is becoming more selective with geopolitical headlines than with earnings dynamics. In plain terms, investors are increasingly separating temporary diplomacy headlines from durable valuation updates. As long as AI-driven spending and profit expectations keep improving at the margin, equities can remain supported even without a major diplomatic resolution in the headlines. The practical takeaway is not to ignore risk, but to price it: unresolved conflicts are now often a discount factor, while AI-linked cash-flow expansion has become the dominant upside catalyst for incremental upside this cycle. Why the Tape Can Stay Elevated When Headlines Are Not The headline you see vs. the risk you price The Morgan Stanley framing of AI momentum and the JPMorgan question on stock highs despite no Iran resolution both point to one central reality: markets can absorb unresolved risk when the forward story is strong enough. In this context, geopolitical friction may be visible but is no longer the only ruler of returns. That matters because public conversation often assumes a linear reaction model: bad diplomacy equals bad markets. In practice, markets tend to run on probabilities, not certainties. If most participants believe a specific shock has a low incremental probability of derailing earnings, they keep paying for growth narratives. The signal that actually matters A more useful way to read these headlines is: what is being repriced now? If AI-related demand is lifting capex, software demand, and productivity narratives, then those firms get multiple support even in a choppy macro backdrop. If headlines are about stalled diplomacy but no immediate earnings shock, the effect may be mostly a volatility discount, not a valuation reset. That is why market commentary from both houses can coexist: AI remains the price-supporting engine, while geopolitics sits in the discount matrix. AI Momentum as a Valuation Anchor Not a generic bullish story, but a cash-flow story The AI narrative is no longer just “hype”; the more important test is whether firms can convert AI-related spending into sust

Why Equities Stay at Records: How Risk Is Being Repriced, Not Erased

TL;DR: Markets can remain near record highs even with unresolved geopolitical headlines when investors judge cash-flow resilience and financing conditions to be stronger than the headline risk itself. The question raised by both recent finance commentaries—that pessimists may be missing the resilience narrative and that records can coexist with no Iran resolution—suggests a deeper shift: risk is still present, but it is now priced as a spread and duration issue rather than a collapse trigger. In practice, market participants are separating event noise from balance-sheet reality and rewarding models that can earn through volatility. ) The setup: record pricing with open headlines The market contradiction in plain terms The current backdrop is not a contradiction as much as it is a repricing mechanism. One narrative says unresolved geopolitical friction should eventually compress risk assets; the other says markets are looking through immediate headlines because corporate cash generation and sector leadership still hold up. The Invesco angle highlights that many short-term fears may be over-correcting market positioning, while the JP Morgan question captures the unease around not having a clear diplomatic pivot. Yet both frame the same phenomenon: price formation is now driven less by whether one headline happens this week and more by whether earnings, margins, and rates support those headlines. From headline risk to regime risk This is important fo

SoftwareOne's AI Targets Turn Software Sprawl Into A Margin Story

TL;DR: SoftwareOne used its June 9, 2026 capital-markets day to set 2030 targets built around the Crayon integration, AI demand, EBITDA margin above 28%, and free-cash-flow conversion above 60%. The sharper business implication is not that AI magically lifts every software reseller. It is that enterprise AI spending creates a new control problem, and the broker that can clean up licenses, cloud commitments, and vendor sprawl may capture margin from the mess. #What SoftwareOne Is Really Selling SoftwareOne said on June 9 that its 2030 ambition includes high-single-digit revenue CAGR, EBITDA margin above 28%, free-cash-flow conversion above 60%, and a 30% to 50% dividend payout. Reuters summarized the same plan as a bet on AI efficiencies, operating leverage, and Crayon integration. That sounds like a software-company forecast. It is better read as a procurement forecast. SoftwareOne is not trying to be the model maker, chip supplier, or glamorous AI application. It sits closer to the budget desk, where companies ask a less exciting question: why are we paying for five overlapping tools, three cloud contracts, unused seats, duplicate security add-ons, and AI pilots that no one has converted into governed production work? That is where the money can hide. AI does not reduce software sprawl by itself A CIO can approve a new AI assistant in one department, a cloud migration in another, and a data-governance tool somewhere else. Each decision may make sense alone. Together, they create a stack that no single buyer fully understands. The vendor selling optimization becomes useful when the bill stops being legible. SoftwareOne's May trading update said Q1 2026 reported revenue rose [67.4% year over year because of the Crayon acquisition](https://www.softwareone.com/en-au/media-releases/2026/05/12/softwareone-q1-2026-trading-updat

Dexcom's New Trial Moves Glucose Sensors Into The Coverage Workflow

TL;DR: Dexcom's latest study is not just another med-tech efficacy update. It is a business case for moving continuous glucose monitors out of the endocrinology niche and into the reimbursement, pharmacy, and primary-care workflow. If coverage follows the evidence, the bigger fight will be less about sensors and more about who pays to monitor patients earlier. #What Dexcom Actually Proved Dexcom said its CONNECT randomized controlled trial showed that adults with type 2 diabetes who were not using insulin still got a meaningful benefit from wearing the Dexcom G7. Participants using the device saw an average 1.6 percentage point A1C reduction over 26 weeks, which was 0.9 points better than routine care, and the study was run across 22 U.S. primary-care practices rather than a narrow specialist setting. That setting is the whole story. A glucose sensor for insulin users is an established tool. A glucose sensor for people managed mostly with metformin, GLP-1 drugs, SGLT2s, diet changes, and primary-care follow-ups is a coverage question. Dexcom also said 68% of participants using G7 reached A1C below 7.5% at 26 weeks and that time in range was about five hours per day better than the control group. The company explicitly framed the result as evidence that could help establish a new standard of care for non-insulin type 2 diabetes. This was a clinic-workflow study disguised as a product update Look at the scene behind the press release. A patient shows up at a regular primary-care office with an elevated A1C, maybe already on a GLP-1, maybe trying to avoid insulin, and the clinician has to decide whether to escalate drugs, wait longer, or monitor more closely. The sensor changes that visit from a quarterly guess into a daily data stream. #Why The Money Question Starts Here Dexcom is already a large device company, not a speculative startup. In its [first-quarter 2026 results](https://investors.dexcom.com/news/news-details/2026/Dexcom-Reports-First-

Defiance MUZ Turns The Micron AI Trade Into Daily Reset Math

TL;DR: Defiance ETFs launched the Defiance Daily Target 2X Short MU ETF, ticker MUZ, on June 9, 2026, giving traders a fund that seeks -200% of Micron Technology's daily share-price move before fees and expenses. The point is not that Micron suddenly became a worse company. The point is that the AI memory trade is now volatile and popular enough to support specialized short-horizon products built around daily reset math. #What Defiance Actually Launched Defiance's new MUZ ETF is designed to deliver -2 times Micron Technology's daily percentage move, before fees and expenses. That sentence does a lot of work. It means the fund is not a long-term short thesis on memory chips. It is not a cleaner way to "own the opposite of Micron." It is a one-day trading instrument wrapped in an ETF ticker, with compounding and rebalancing doing the real work after the first close. The launch matters because Micron is not a sleepy component supplier anymore. In Micron's latest quarterly filing, the company said AI-driven data-center growth accelerated demand for memory and storage faster than Micron and the broader industry could increase supply, while DRAM and NAND demand stayed tight across the portfolio in its fiscal second-quarter 2026 10-Q. That is exactly the kind of story that attracts both believers and skeptics. #Why The Product Says More About Traders Than Micron The ordinary scene is a desk with two screens, a calculator app, and a trade ticket open before the coffee is cold. One person is not underwriting Micron's next decade of high-bandwidth memory supply. They are trying to express a view before the next earnings whisper, analyst note, export-control headline, or AI-server spending rumor hits the tape. That is the real market for MUZ. Daily reset is

Amazon's Corning Fiber Deal Moves AI Capex Into The Cable Plant

TL;DR: Amazon's June 8 multibillion-dollar agreement with Corning is a reminder that AI infrastructure is not just a GPU auction. The deal commits Corning to supply optical fiber, cable, and connectivity products for Amazon's U.S. data-center buildout while adding 1,000 North Carolina manufacturing jobs. The business implication is blunt: hyperscalers are starting to lock up the boring physical inputs that decide whether AI capex can actually turn into usable capacity. #What Amazon And Corning Actually Announced Amazon said it signed a multiyear, multibillion-dollar agreement with Corning to supply optical fiber, cable, and connectivity products for its expanding U.S. data-center infrastructure. The headline number is jobs: 1,000 advanced manufacturing roles at Corning facilities in North Carolina, plus hundreds of construction jobs. The more important number is hidden in the type of commitment. Amazon is not buying a batch of cable like office supplies. It is reserving industrial capacity in a supply chain that now sits inside the AI capex cycle. That is the part investors should not wave away. AI demand keeps getting discussed as if the bottleneck is one giant semiconductor purchase order. But a data center is a stack of constraints. Power, land, cooling, transformers, networking gear, skilled labor, and fiber all have to arrive in the right sequence. Miss one handoff, and the GPU rack becomes expensive furniture. #Why Fiber Has Become A Capital-Allocation Issue Corning's optical communications business was already moving before this Amazon announcement. In April, Corning reported that first-quarter Optical Communications sales grew 36% year over year, helped by demand tied to generative AI and hyperscale customers. That matters because optical fiber is not a glamorous line item, but it is close to the nervous system of the AI factory. The compute cluster needs high-bandwidth, low-latency connectivity inside and between fac

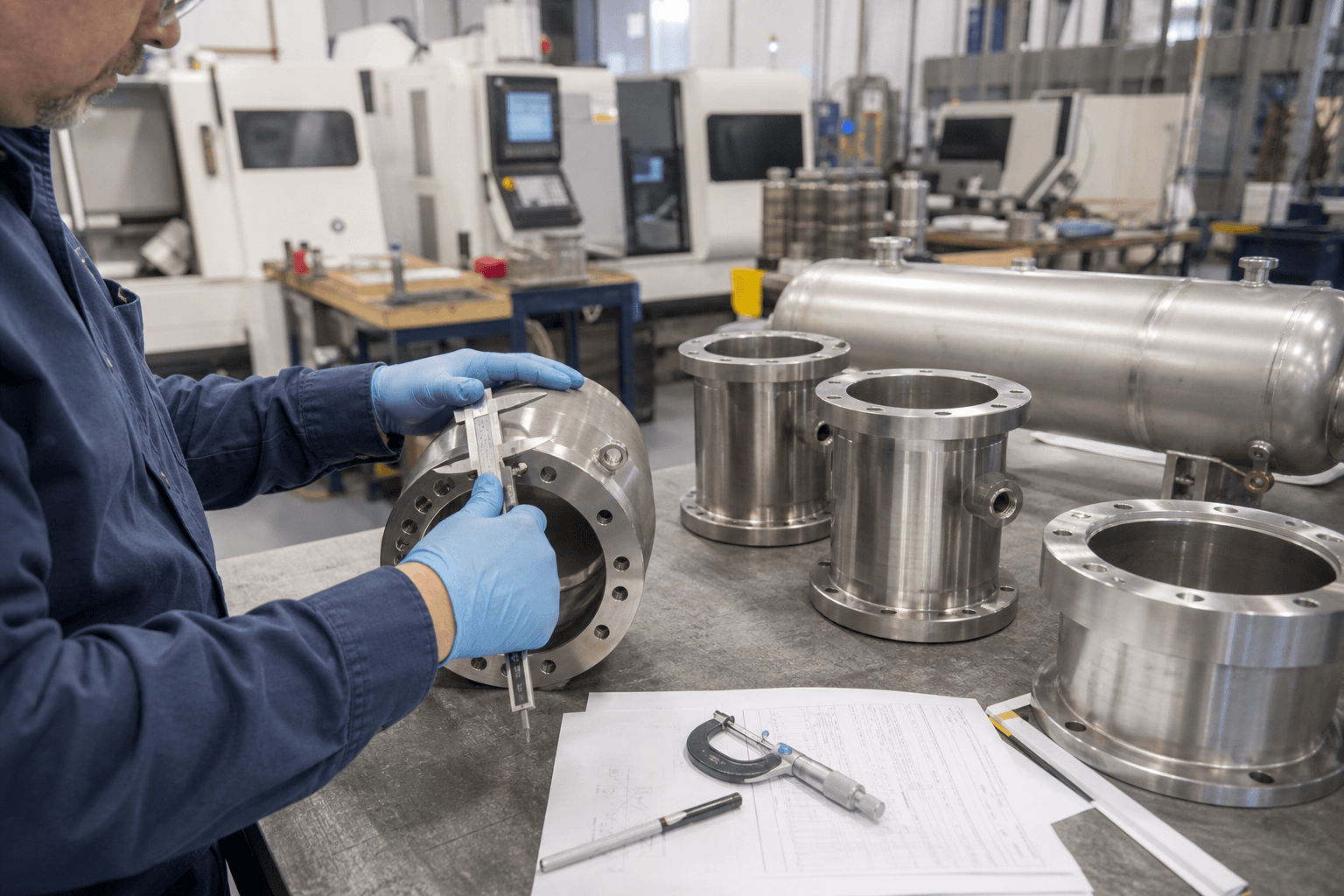

Graham Corporation Shows Where Defense Spending Meets The Machine Shop

TL;DR: Graham Corporation reported fiscal 2026 results on June 8 with record annual revenue, a $533 million backlog, and fresh guidance for another growth year. The point is not that one small industrial supplier had a good quarter. It is that defense, energy/process, and space customers are pushing real demand into specialized factory floors, where the scarce asset is not the contract announcement but the ability to turn complex orders into inspected, shipped hardware. #What Graham's Backlog Really Says Graham Corporation's fiscal 2026 release had the usual public-company markers: fourth-quarter revenue up 37% year over year, fiscal-year revenue up 22%, and fiscal 2027 guidance for revenue of $275 million to $290 million. The more useful number is backlog. Graham ended March 31, 2026 with $532.6 million of remaining performance obligations, according to its fiscal 2026 Form 10-K. The company expects only about 35% to 40% of that backlog to convert into revenue within one year. That is a different kind of signal than a software pipeline or a retail order book. It tells investors that demand is already spoken for, but capacity, labor, engineering review, inspection, customer acceptance, and working capital decide how fast it becomes sales. #Why The Machine Shop Is The Market Story The market usually talks about defense spending, energy infrastructure, and space programs as budget lines. Graham forces a more practical view. Somewhere after the purchase order, a machinist is measuring a stainless-steel component on a factory floor. An engineer is checking drawings. Someone in production control is deciding whether one delayed part pushes another customer slot into the next quarter. That is where industrial spending gets real. Why backlog is not the same as revenue Backlog is comforting becau

FedEx's $4.88 Dividend Puts The Freight Spin-Off On A Capital-Allocation Clock

TL;DR: FedEx raised its adjusted annual dividend rate to $4.88 after completing the FedEx Freight spin-off, but the real story is not the 5% shareholder-return headline. It is the new capital-allocation bargain: FedEx keeps the dividend signal and a 19.9% Freight stake, while the newly public FedEx Freight now has to prove its less-than-truckload economics can carry a debt-funded separation. #What FedEx Actually Changed FedEx said its board approved a 5% annual dividend increase after adjusting for the FedEx Freight spin-off, setting an annualized rate of $4.88 for the transition period from June 1, 2026 through Dec. 31, 2026. The quarterly cash dividend is $1.22 per FedEx share, payable July 7 to holders of record on June 22. That sounds like an ordinary dividend update. It is not ordinary. It lands one week after FedEx completed the separation of FedEx Freight, which began trading on the NYSE as FDXF on June 1. FedEx kept trading as FDX, but the company that investors are valuing now is different from the company that carried the freight unit last month. The dividend is a message to old FedEx holders The point of the dividend is continuity. FedEx is telling investors that the parent company did not become a weaker income story just because one of its cleaner freight assets moved outside the perimeter. That is the surface message. The deeper question is whether the parent can keep that signal while the market separately prices the freight business, the retained stake, and the debt that helped make the split work. #Why The Freight Spin-Off Is A Balance-Sheet Story FedEx completed the spin-off by distributing 80.1% of FedEx Freight shares to FedEx shareholders. Holders received one FedEx Freight share for every two FedEx shares they owned as of May 15. FedEx retained 19.9% of FedEx Freight. The company says it plans to dispose of that stake within 24 months through debt-for-equity exchanges, dividends, or exchanges for FedEx common stock. That

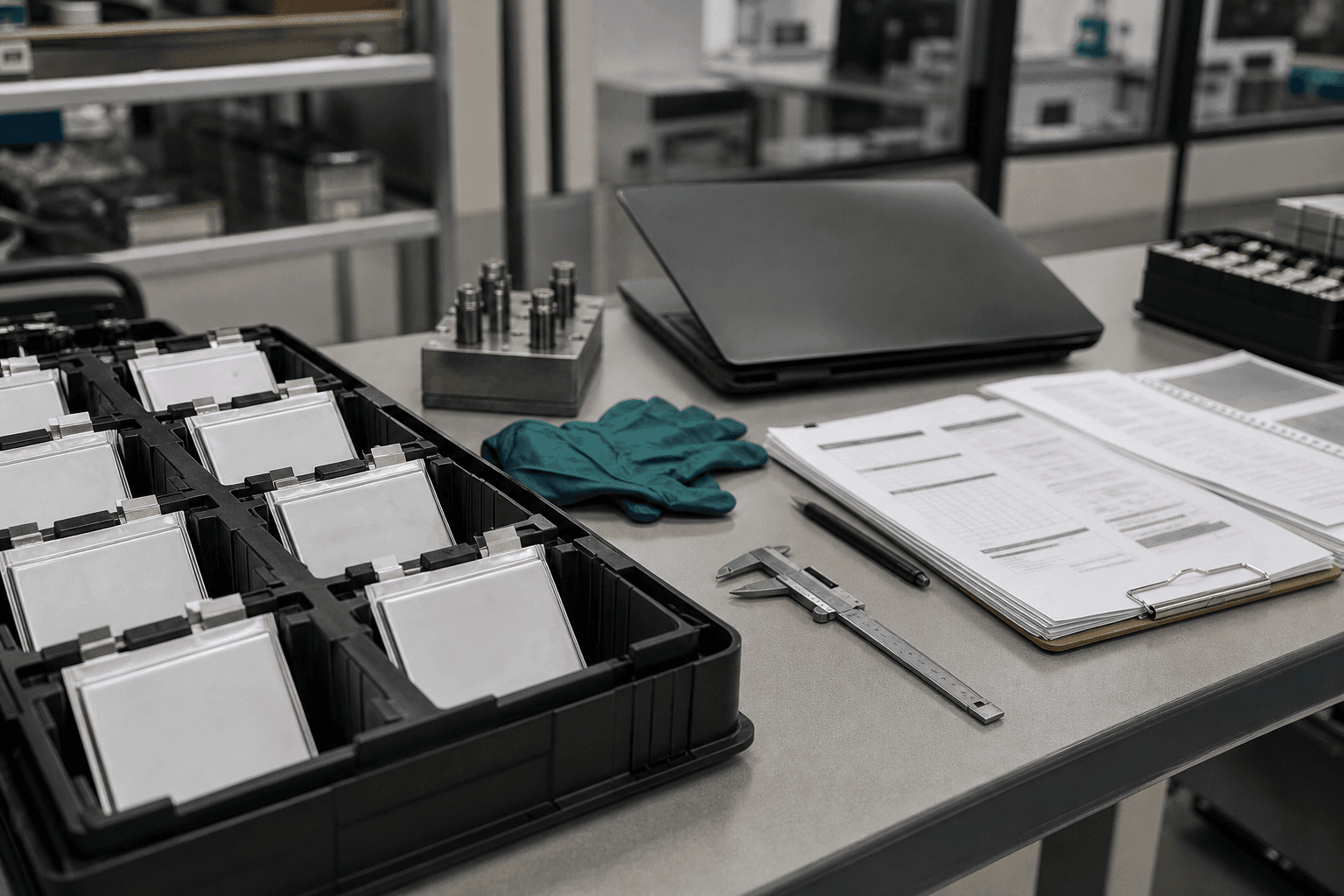

Factorial's Nasdaq Debut Moves Solid-State Batteries Into The Factory Ledger

TL;DR: Factorial Energy began trading on Nasdaq on June 8 after completing its Cartesian Growth III SPAC combination, with the company saying the deal implies about $1.3 billion of equity value and brings in more than $100 million of gross proceeds. The important point is not that solid-state batteries have become easy. It is that the financing question has moved from science risk to factory and qualification risk, where public investors are now being asked to fund the slow middle mile. #What Factorial Actually Brought To Nasdaq Factorial Energy is not selling investors a vague clean-tech mood. It came public through a completed business combination with Cartesian Growth Corporation III, and its Series A common stock and warrants were expected to trade on Nasdaq under FAC and FACWW. The company says the transaction implies roughly $1.3 billion of equity value and provides more than $100 million of gross proceeds for commercialization across defense and aerospace, hyperscale data centers, robotics, and e-mobility. That is the clean headline. The messier story is more useful. Solid-state batteries have spent years living in the same investor category as many advanced manufacturing dreams: impressive test cells, famous partners, ambitious energy-density claims, and a brutal gap between a lab result and a repeatable production line. Factorial's Nasdaq debut does not close that gap. It puts a public price tag on it. #Why The Middle Mile Is The Real Business Story The seductive part of the story is the vehicle test. Factorial points to Mercedes-Benz integrating its FEST cells into a lightly modified EQS test vehicle and completing a 1,205-kilometer journey from Stuttgart to Malmo on one charge. It also cites Stellantis lab testing of 77Ah cells and its earlier 100Ah-plus lithium-metal solid-state battery milestone. Those proof points matter. They are not the same as commercial economics. The hard handoff is from demo cell to customer process The next test is not whether a battery can look imp

REPAY's KUBRA Deal Turns Utility Bills Into A Payments Toll Road

TL;DR: REPAY closed its $372 million cash acquisition of KUBRA, creating a larger consumer bill-payment platform across utilities, government, and insurance. The business implication is not simply "more payments volume." REPAY is buying a place inside boring, recurring household obligations, where bill presentment, reminders, payment processing, and customer communications can become one sticky infrastructure layer. The catch is leverage: this toll road only works if integration savings arrive before debt costs eat the story. #What REPAY Actually Bought REPAY said it completed the KUBRA acquisition for $372 million in cash, after announcing the agreement on March 30, 2026. The headline sounds like another payments deal. It is more specific than that. KUBRA sits in the unglamorous handoff between large billers and households: utility bills, government payments, insurance communications, payment notifications, and customer-service workflows. REPAY says the combined platform will reach over 40% of U.S. and Canadian households every month and process more than $130 billion in combined annual payment volume. That is the part investors should not skim past. Card swipes are discretionary. Utility bills are not. The payment processor that gets embedded into those recurring obligations is not just chasing checkout volume; it is trying to own a tiny operational toll on bills people have to pay. #Why The Boring Bill Is The Product The ordinary household scene is the point: a laptop on the kitchen table, a utility notice, a debit card, a due date, and one more password reset that nobody wanted. For the consumer, that is a chore. For a biller, it is a cost center. For a payments company, it is a repeatable workflow with several monetizable handoffs: presenting the bill clearly enough that it gets paid; nudging the customer before the due date; routing the card, ACH, wallet, or other payment method; handling

Campbell's Q3 Shows Branded Groceries Have A Margin Shelf Problem

TL;DR: Campbell's reported fiscal third-quarter 2026 results on June 8 with net sales down 4% to $2.4 billion and adjusted EPS down 32%, while reaffirming its full-year guidance. The useful read is not simply that soup and snacks had a soft quarter. It is that branded grocery companies are losing the easy version of pricing power: shoppers still want familiar food, but the shelf is forcing volume, discounts, tariffs, and margin protection into the same narrow space. #What Campbell's Q3 Says About The Grocery Shelf Campbell's quarter is a clean little snapshot of the post-inflation consumer. The company said third-quarter net sales fell 4% on a reported and organic basis. Adjusted EBIT fell 24% to $274 million. Adjusted EPS fell 32% to $0.50. Those numbers matter because Campbell's is not selling some fragile luxury product. It sells soup, broth, pasta sauce, crackers, cookies, pretzels, chips, and other pantry habits through brands like Campbell's, Swanson, Prego, Rao's, Goldfish, Pepperidge Farm, Cape Cod, Kettle Brand, and Snyder's of Hanover. If that kind of portfolio cannot pass costs through cleanly, the pressure is not just "weak consumer sentiment." It is shelf math. #Why The Old Trade-Down Story Is Getting Too Simple For a while, packaged-food investors could lean on a comforting story: when shoppers feel squeezed, they eat at home, buy more pantry staples, and trade restaurants for grocery carts. That story is still partly true. It is also incomplete. The harder story is that the grocery aisle has become a three-way negotiation: Consumers want familiar brands, but they notice unit prices. Retailers want traffic and basket size, so they push promotions and private-label comparisons. Manufacturers want to protect gross margin while labor, ingredients, freight, tariffs, and supply-chain costs keep leaking into the P&L. Campbell's second-quarter release in March already showed the pattern: sales were pressured by lower volu

Panasonic's Kansas Battery Plan Puts AI Capex Inside The Power Rack

TL;DR: Panasonic Holdings plans to start mass production of battery cells for data-center applications at its Kansas plant in fiscal 2028, according to a June 8 Reuters report. The business implication is bigger than one factory line: AI infrastructure spending is moving from servers and chips into rack-level power stability, where batteries, capacitors, and supplier qualification can become recurring margin machinery. #What Panasonic Is Really Moving Into Kansas Reuters reported on June 8 that Panasonic Holdings plans to produce battery cells for data-center applications at its Kansas plant in fiscal 2028, which ends in March 2029. That sounds like a manufacturing footnote. It is not. Panasonic is trying to make the power rack a commercial product, not a background utility item. The company is taking a business it already describes as a data-center energy-storage franchise and putting more production closer to the North American hyperscaler buildout. The relevant customer is not a household buying batteries. It is a cloud operator trying to keep AI servers from turning power volatility into downtime, equipment stress, or inefficient capacity planning. #Why The Battery Is Becoming Part Of The AI Budget Panasonic has already framed the problem plainly: high-performance AI servers can draw large amounts of electricity in short bursts, creating peak power swings and unstable voltage. The company says rack-level battery backup units can help cover those peaks and stabilize operations inside AI data centers. That is the useful business clue. When investors talk about AI infrastructure, the conversation still leans toward GPUs, networking gear, custom chips, cooling systems, and utility interconnects. Those matter. But the less glamorous layer is now moving into the same capital-spending argument: battery cells and modules inside the rack peak-shaving systems that reduce demand spikes power-control hardware that protects expensive server utilization supplier relationshi

Honeywell Aerospace's Spin-Off Turns Supply Chains Into A Standalone Balance Sheet

TL;DR: Honeywell set a June 15, 2026 record date and a June 29 distribution date for the Honeywell Aerospace spin-off, with the new company expected to trade on Nasdaq as HONA. The real business story is not the ticker. It is that a large aerospace supplier is being pulled out of a conglomerate wrapper with its own debt stack, capital allocation policy, and investor base. That makes supply-chain execution easier to value and harder to hide. #What Honeywell Is Actually Separating Honeywell's board has now put dates around the split. The company said Honeywell shareowners of record on June 15 are expected to receive one Honeywell Aerospace share for every two Honeywell shares, with the distribution expected at 12:01 a.m. New York time on June 29. One minute later, Honeywell expects to execute a 1-for-2 reverse split of the remaining HON shares. That is a little piece of market plumbing, but it matters because it tells investors this is not a casual carve-out. Honeywell is trying to hand investors a cleaner aerospace stock while keeping the remainco share count from looking mechanically bloated after the separation. The cleaner read is this: Honeywell Aerospace is leaving the parent as a focused aerospace-and-defense supplier, not as a tiny side asset. Honeywell said the Form 10 introduced an aerospace business with $17.4 billion of 2025 net sales, $1.5 billion of pro forma net income, and $4.3 billion of pro forma adjusted EBIT. That is large enough to force dedicated coverage, dedicated benchmarks, and dedicated questions. #Why The Reverse Split Is Not The Interesting Part Reverse splits usually carry a low-quality smell because weak companies use them to stay listed. Honeywell's version is different. It is a share-count reset attached to a blue-chip breakup. That does not make it irrelevant. It just changes the question. What t

Banco BPM's MPS Bid Makes Branch Scale The New Bank Trade

TL;DR: Banco BPM's June 7 approach to Monte dei Paschi di Siena is not just another European bank M&A headline. The real business point is that Italian bank consolidation is turning branches, deposits, insurance distribution, and cost takeout into tradable assets. If a Banco BPM-MPS deal, or a rival Intesa/BPER move, advances, investors should read it as a scale test for domestic banking economics, not as a simple national-champion story. #What Banco BPM Actually Put On The Table Banco BPM said its board unanimously approved opening talks with Banca Monte dei Paschi di Siena on June 7. The proposed combination would be a merger of equals and could create Italy's second-largest bank. That wording matters. A merger of equals is the polite version of a difficult operating problem: two branch networks, two management teams, two local identities, one cost base that has to shrink. The marketable story is consolidation. The harder story is execution. #Why The Branch Network Is The Real Prize Reuters' expanded report said the combined group would have a market value of roughly EUR50 billion, or about $58 billion, and Banco BPM estimated more than EUR1.1 billion of annual pre-tax benefits. Those benefits are not magic. They come from three ordinary banking levers: fewer overlapping costs; better use of customer relationships; more product revenue pushed through the same distribution base. That is why the branch map matters. A bank branch is no longer just a place to collect deposits. It is a distribution point for mortgages, wealth products, insurance, small-business credit, and local relationship pricing. When rates are high, deposits are not passive funding. They are a margin line. Why cost synergies are easier to announce than to bank

Hubbell's NSI Debt Deal Puts A Price On Electrical Shelf Space

TL;DR: Hubbell's $1.9 billion senior-note deal, expected to close on June 8, 2026, is not just acquisition plumbing for its $3 billion NSI Industries purchase. It is a market signal that small electrical parts now carry infrastructure economics: connectors, fittings, timers, and wire-management products can be valuable because they sit inside distributor shelves, contractor habits, and data-center or light-industrial project workflows. #What Hubbell Is Really Buying From NSI Hubbell priced $1.9 billion of senior notes across 2031, 2033, and 2036 maturities to help fund its pending NSI Industries acquisition. The deal is expected to close on June 8, subject to normal conditions. The headline number is easy to treat as balance-sheet trivia. It should not be. Hubbell agreed in May to buy NSI for $3.0 billion in cash, adding a company that sells electrical fittings, connectors, components, timers, and wire-management products. NSI expects about $570 million of 2026 revenue, and Hubbell says the acquisition should be accretive to adjusted EPS in 2026. That makes the bond deal more than financing. It is Hubbell putting long-dated capital behind a very specific bet: the boring replenishment layer of electrification is becoming worth paying up for. #Why Small Electrical Parts Have A Bigger Margin Story Walk into an electrical distributor branch and the visible drama is not dramatic at all. A contractor needs a connector, a fitting, a timer, or a wire-management part before a job can move. The item is small. The delay is not. That is why these products matter commercially. They are not glamorous project announcements. They are the handoff points between design, field labor, inventory, and billing. The shelf matters because the job clock is expensive If a contractor is standing at the

Japan's GDP Revision Puts The BOJ Hike Trade On A Capex Desk

TL;DR: Japan's June 8 GDP revision did not change the big picture: the economy is still too soft to give the Bank of Japan a clean hiking lane, but not weak enough to end the normalization trade. The important business signal is capital spending. If Japanese companies hesitate at the capex desk, the BOJ's next rate move becomes less about inflation confidence and more about whether higher funding costs start choking the very investment Japan needs. #What Japan's GDP Revision Actually Changed Japan's Cabinet Office had the second preliminary estimate for January-March GDP scheduled for June 8 at 8:50 a.m. JST. Reuters reported that the revision showed a slightly smaller first-quarter contraction than initially estimated, helped by firmer capital expenditure. That sounds like a small statistical clean-up. For markets, it is more useful than that. Japan is not a normal rates story. The Bank of Japan is trying to move away from decades of ultra-easy money while companies, households, banks, and foreign investors are still wired around the idea that yen funding is cheap. The revision matters because it puts corporate investment, not the headline GDP print, at the center of the next decision. #Why The Capex Line Is The Real BOJ Test The BOJ said in its April outlook that it would continue to raise the policy interest rate in response to economic activity, prices, and financial conditions. The current policy rate is around 0.75%, already a major psychological shift for a country that spent years near zero. But hiking from here requires a different kind of proof. It is not enough for inflation to be sticky because food, energy, or imported costs are annoying households. The BOJ needs proof that companies are still willing to invest, lift wages, and pass costs through without freezing the domestic demand engine. That is why capex is the desk-level indicator. The CFO version of the story Picture a finance manager at a J

CMS's Medicare GLP-1 Bridge Moves Obesity Drug Risk Into A New Claims Lane

TL;DR: CMS is launching the Medicare GLP-1 Bridge on July 1, 2026, giving eligible Part D beneficiaries access to selected obesity GLP-1 drugs through a temporary program outside the normal Part D payment flow. The quiet business point is not just the $50 copay. CMS is creating a separate claims and payment lane, with Humana as central processor, so plans lose near-term risk while CMS buys operating data on a drug class too expensive to manage by slogan. #What CMS Is Actually Building The Medicare GLP-1 Bridge looks simple at the pharmacy counter: an eligible beneficiary gets access to certain GLP-1 drugs for weight management, with a $50 copay, between July 1, 2026 and December 31, 2027. That is the consumer version. The business version is more interesting. CMS says the bridge will operate outside the Medicare Part D benefit's normal coverage and payment flow. Part D sponsors will not carry risk for eligible GLP-1 drugs furnished through the bridge, and they do not have to opt in for beneficiaries to use it. That is a strange sentence in Medicare finance. It means the government is not just expanding access. It is temporarily removing one of the most politically sensitive drug categories from the usual plan-risk machine. #Why The Processor Matters More Than The Copay At a pharmacy counter, the difference between "covered by your plan" and "covered through a bridge" can feel like paperwork. For the money, it is the whole story. CMS says it will use a single central processor in 2026 to handle prior authorization, claims adjudication, and payment to pharmacies. In separate Part D plan guidance, CMS names Humana, the administrator of the Limited Income Newly Eligible Transition program, as that processor. That puts Humana in an odd but valuable operating position. It is not simply another Medicare Advantage company watching GLP-1 utilization from the outside. It is being used as national infrastructure for the workflow that decides whether a presc