Factorial's Nasdaq Debut Moves Solid-State Batteries Into The Factory Ledger

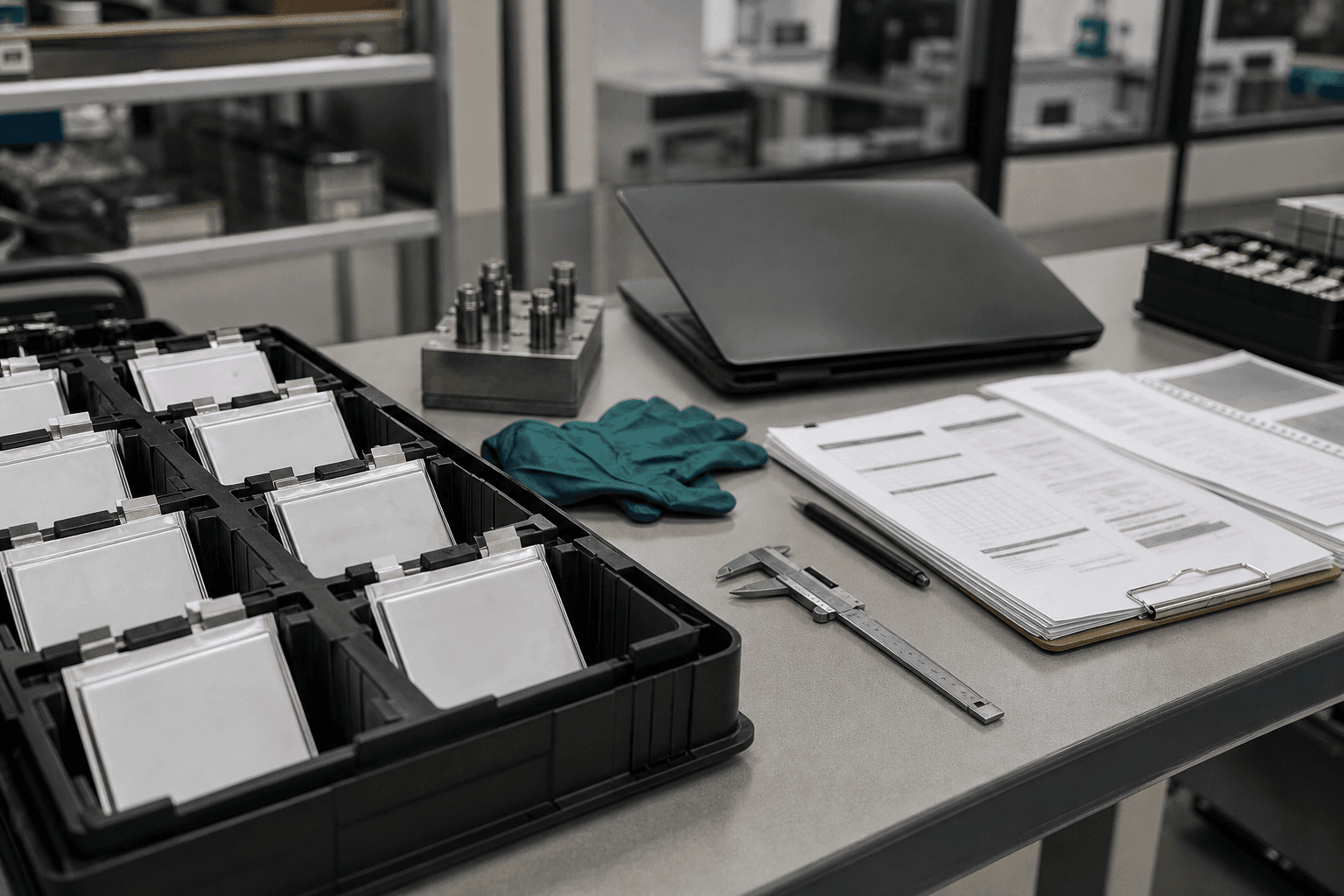

TL;DR: Factorial Energy began trading on Nasdaq on June 8 after completing its Cartesian Growth III SPAC combination, with the company saying the deal implies about $1.3 billion of equity value and brings in more than $100 million of gross proceeds. The important point is not that solid-state batteries have become easy. It is that the financing question has moved from science risk to factory and qualification risk, where public investors are now being asked to fund the slow middle mile. #What Factorial Actually Brought To Nasdaq Factorial Energy is not selling investors a vague clean-tech mood. It came public through a completed business combination with Cartesian Growth Corporation III, and its Series A common stock and warrants were expected to trade on Nasdaq under FAC and FACWW. The company says the transaction implies roughly $1.3 billion of equity value and provides more than $100 million of gross proceeds for commercialization across defense and aerospace, hyperscale data centers, robotics, and e-mobility. That is the clean headline. The messier story is more useful. Solid-state batteries have spent years living in the same investor category as many advanced manufacturing dreams: impressive test cells, famous partners, ambitious energy-density claims, and a brutal gap between a lab result and a repeatable production line. Factorial's Nasdaq debut does not close that gap. It puts a public price tag on it. #Why The Middle Mile Is The Real Business Story The seductive part of the story is the vehicle test. Factorial points to Mercedes-Benz integrating its FEST cells into a lightly modified EQS test vehicle and completing a 1,205-kilometer journey from Stuttgart to Malmo on one charge. It also cites Stellantis lab testing of 77Ah cells and its earlier 100Ah-plus lithium-metal solid-state battery milestone. Those proof points matter. They are not the same as commercial economics. The hard handoff is from demo cell to customer process The next test is not whether a battery can look imp