Graham Corporation Shows Where Defense Spending Meets The Machine Shop

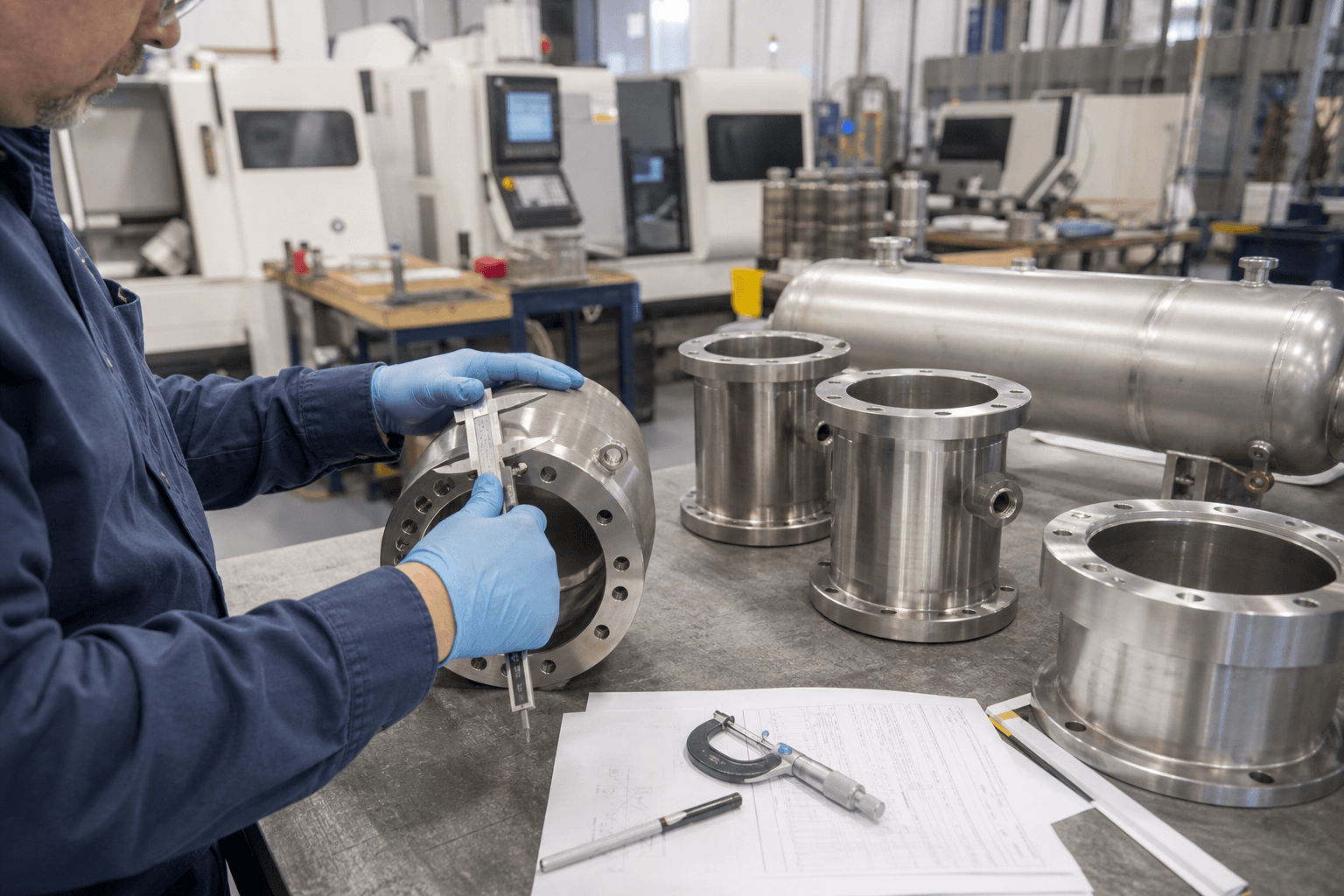

TL;DR: Graham Corporation reported fiscal 2026 results on June 8 with record annual revenue, a $533 million backlog, and fresh guidance for another growth year. The point is not that one small industrial supplier had a good quarter. It is that defense, energy/process, and space customers are pushing real demand into specialized factory floors, where the scarce asset is not the contract announcement but the ability to turn complex orders into inspected, shipped hardware. #What Graham's Backlog Really Says Graham Corporation's fiscal 2026 release had the usual public-company markers: fourth-quarter revenue up 37% year over year, fiscal-year revenue up 22%, and fiscal 2027 guidance for revenue of $275 million to $290 million. The more useful number is backlog. Graham ended March 31, 2026 with $532.6 million of remaining performance obligations, according to its fiscal 2026 Form 10-K. The company expects only about 35% to 40% of that backlog to convert into revenue within one year. That is a different kind of signal than a software pipeline or a retail order book. It tells investors that demand is already spoken for, but capacity, labor, engineering review, inspection, customer acceptance, and working capital decide how fast it becomes sales. #Why The Machine Shop Is The Market Story The market usually talks about defense spending, energy infrastructure, and space programs as budget lines. Graham forces a more practical view. Somewhere after the purchase order, a machinist is measuring a stainless-steel component on a factory floor. An engineer is checking drawings. Someone in production control is deciding whether one delayed part pushes another customer slot into the next quarter. That is where industrial spending gets real. Why backlog is not the same as revenue Backlog is comforting becau