Hoka Is Exposing a New Fault Line in Consumer Spending

Deckers just delivered the kind of quarter that should make investors rethink how they talk about the U.S. consumer. The company behind Hoka and UGG said fourth-quarter sales rose 10% to $1.12 billion, with Hoka up 14.5% and direct-to-consumer revenue up 13.2%. It also guided fiscal 2027 sales above Wall Street expectations.

On the surface, that looks like a simple premium-brand win. But it landed in the same week that consumer sentiment hit another record low and big retailers kept warning that higher fuel costs are squeezing household budgets. That combination looks contradictory only if you assume consumer weakness has to show up evenly.

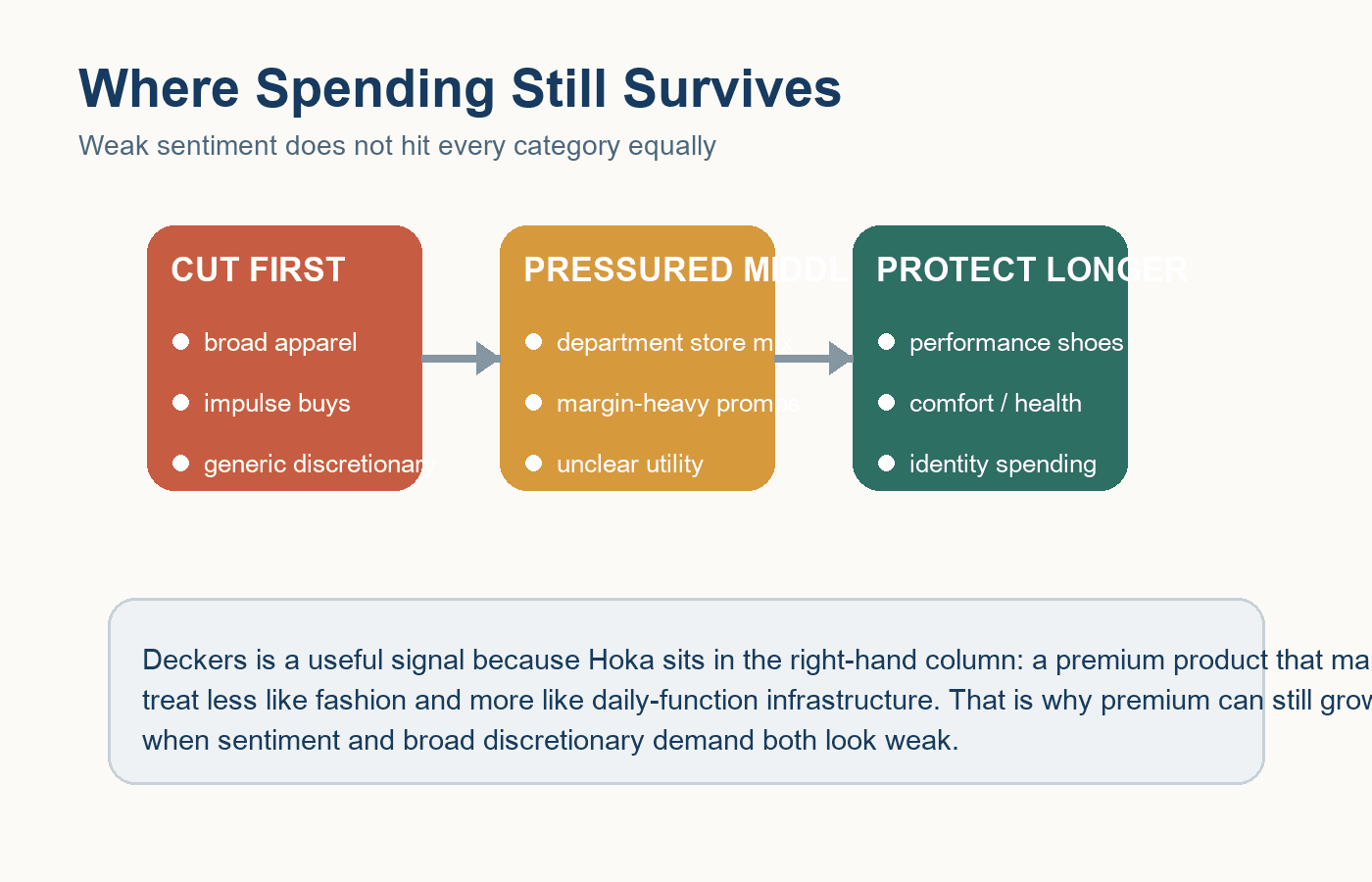

What casual readers may be missing is that the slowdown is starting to look less like a collapse and more like a barbell. Households are cutting broad, low-conviction discretionary spending while protecting a short list of purchases that feel tied to health, comfort, routine, or identity. Hoka sits right in that protected zone. In that sense, Deckers is not escaping the consumer squeeze. It is revealing where the consumer is still willing to spend through it.

That distinction matters because it changes how to read retail earnings. A brand like Hoka is not winning just because affluent shoppers feel fine. It is winning because a growing share of buyers now treats premium performance footwear less like fashion and more like personal infrastructure. If a shoe feels connected to exercise, injury prevention, commuting comfort, or everyday habit, it can survive budget pressure better than a generic apparel or impulse purchase.

That helps explain why Deckers could post 25.5% international growth, strong full-price demand, and better-than-expected guidance while management still acknowledged a pressured lower-income consumer backdrop. It also helps explain why middle-market retail keeps looking harder than the headline economy suggests. The money is not disappearing entirely. It is being concentrated into fewer categories that feel more defensible to the buyer.

You can see a similar pattern elsewhere. Target said first-quarter net sales rose 6.7%, but the most interesting growth came from non-merchandise revenue such as advertising, membership, and marketplace services. Walmart also posted a solid quarter while warning that elevated fuel costs could push retail price inflation higher later this year. In other words, broadline retailers are increasingly leaning on business-model offsets because selling more stuff alone is not enough protection when the consumer gets choosier.

Deckers is showing the product-side version of the same shift. When budgets tighten, the winners are not necessarily the cheapest sellers or the broadest assortments. They are the companies attached to the purchases consumers mentally reclassify from discretionary to justified. That is a subtle but important difference. A premium running shoe that becomes part of someone’s health or daily-function budget can behave very differently from a premium sneaker bought mainly for style.

This is why the read-through matters beyond one footwear stock. If the consumer is barbelled rather than broken, investors should expect more pain in the middle of discretionary retail than at the high-conviction edges. Brands with clear utility, identity, and pricing discipline may keep growing even while sentiment looks terrible. Generalists without that clarity may keep reporting respectable traffic but weaker margin quality and shakier demand visibility.

The sharper takeaway is that weak consumer sentiment does not automatically mean consumers stop spending. It means they become ruthless editors. Deckers just offered evidence that one of the safest places to be is not “premium” in the abstract. It is premium that feels necessary.