Intuit Is Climbing the CFO Org Chart

Intuit’s latest quarter looked confusing on the surface. The company raised full-year guidance, grew revenue 10% to $8.6 billion, and posted 19% growth in its online business ecosystem. Then the stock sold off anyway, helped along by news that Intuit will cut 17% of its full-time workforce.

The obvious explanation is that investors are still fixated on whether generative AI will weaken TurboTax’s moat. That risk is real enough. Reuters reported that Intuit trimmed its annual TurboTax revenue outlook and that investors remain worried large language models can imitate premium tax guidance. But that framing misses the more important shift inside the company.

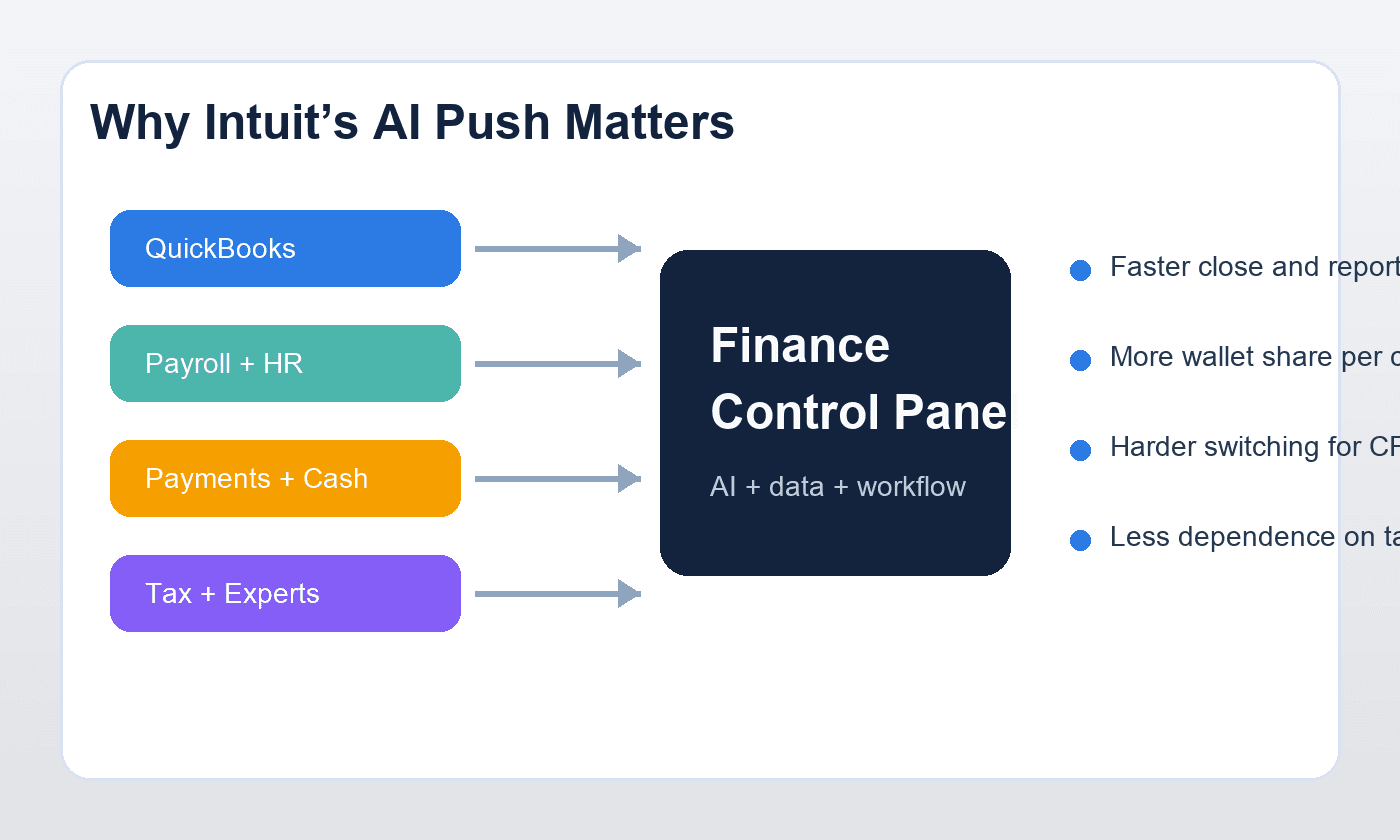

What casual readers may be missing is that Intuit is trying to move the center of gravity of its business away from standalone tax preparation and toward the office of the CFO. The real AI story here is not a smarter tax chatbot. It is an attempt to turn QuickBooks, payments, payroll, HR, and multi-entity reporting into one operating layer for growing businesses. If that works, Intuit stops being valued mainly as a seasonal tax franchise and starts looking more like a finance-workflow platform.

That is why the more revealing number in the quarter was not TurboTax at all. Intuit said Global Business Solutions revenue rose 15% and Online Ecosystem revenue rose 19%, or 22% excluding Mailchimp. QuickBooks Online Accounting grew 22%, while money and payroll offerings also helped drive growth. At the same time, management said it is serving mid-market businesses growing north of 30%.

Those lines connect directly to a second announcement that got much less attention than the earnings print. Earlier in May, Intuit said its Enterprise Suite now brings together financial, operational, and workforce data in one place, with multi-entity close automation, dimensional reporting, integrated human capital management, and a platform capable of managing more than 200 entities. In plain English, Intuit is trying to capture companies before they graduate into heavier ERP systems and convince finance teams they do not need a costly migration to get enterprise-grade control.

That matters because AI is likely to commoditize pieces of tax advice faster than it commoditizes messy, cross-functional execution. Filing help can get cheaper. But the daily work of closing books, managing payroll, moving cash, tracking project profitability, and stitching workforce decisions to financial results is harder to replace with a generic model. The more of that workflow Intuit owns, the less the company depends on any single product line, including TurboTax.

The workforce reduction fits that logic too. It looks less like a simple defensive cost cut and more like an admission that the company wants to reallocate resources toward a leaner, AI-centered platform model. Management is effectively saying that some labor-heavy parts of the old business matter less than speed, integration, and data advantage in the new one. That is uncomfortable in the short run, but strategically coherent.

This is also why the selloff may be reading the wrong scoreboard. Investors focused on whether AI will pressure pricing in consumer tax software. They may be underweighting the possibility that AI actually helps Intuit move upmarket, increase wallet share, and become more embedded in business operations where budgets are larger and switching is harder.

The sharper takeaway is that Intuit is no longer just defending a tax franchise from AI disruption. It is using AI to climb higher into the finance stack. If the company can make itself the default control panel for growing businesses, the more important question will not be whether tax prep got cheaper. It will be whether Intuit turned that pressure into a reason to own more of the customer’s operating system.