Drug Distributors Are Becoming Specialty-Care Toll Roads

Cencora's updated 2026 outlook this week looked modest on the surface. The drug distributor nudged its adjusted earnings guidance higher after recent share repurchases, and its board authorized a new $2 billion buyback. That is not the sort of announcement that usually produces a new theory about healthcare.

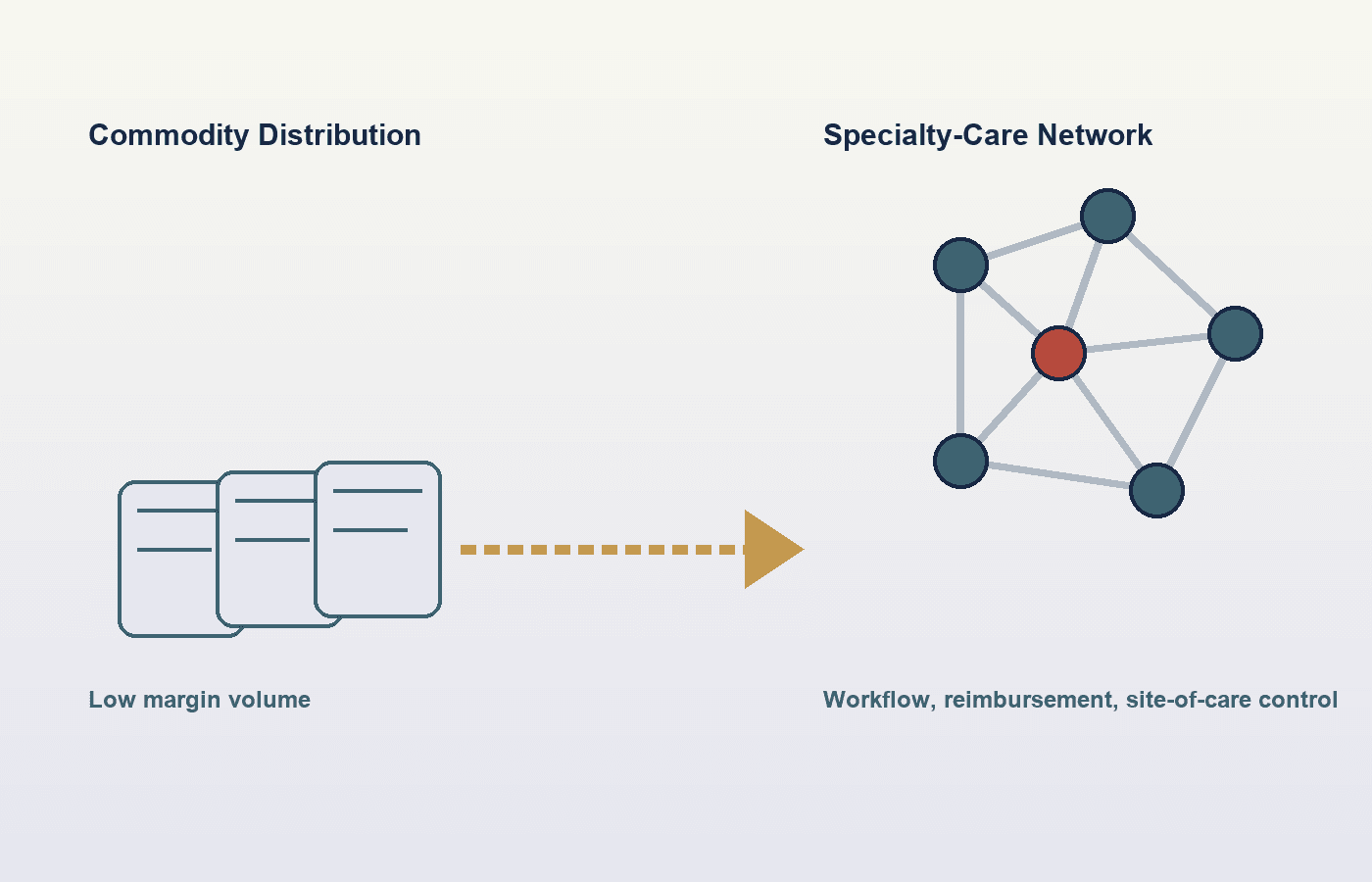

But the more interesting story was buried in the operating details. In its earlier second-quarter release, Cencora said the February acquisition of OneOncology helped lift gross profit margins, even as higher GLP-1 sales diluted margins. In other words, low-margin drug volume is still moving through the system, but the better economics are coming from owning more of the specialty-care workflow around the drugs.

That is the thing most casual readers are missing: big U.S. drug distributors are no longer just trying to move boxes efficiently. They are trying to become toll roads for specialty care, especially oncology, where patient access, physician workflows, reimbursement support, and site-of-care control matter more than pure distribution scale. The business is moving closer to healthcare infrastructure and farther from commodity logistics.

You can see the same pattern across the sector. McKesson used its latest full-year results to highlight expanding specialty provider support, faster patient access through biopharma support services, and the April addition of Cancer Care Northwest to The US Oncology Network. It also kept reshaping the portfolio by separating Medical-Surgical Solutions while buying back stock aggressively. That is what a company does when it believes the highest-return assets are no longer spread evenly across the enterprise.

Cardinal Health is telling a similar story with slightly different words. Its Pharmaceutical and Specialty Solutions segment posted 11% revenue growth and 18% profit growth in the third quarter, then the company raised its full-year outlook again. Cardinal's profit engine is increasingly the part of the business tied to branded and specialty pharmaceuticals, not the more commoditized corners of healthcare distribution.

This matters because specialty drugs are not just another volume category. They reshape who has pricing leverage and who gets paid for complexity. GLP-1 sales can inflate revenue but pressure margins because the products are expensive and economics are thinner. Oncology is different. If a distributor owns physician relationships, infusion support, prior-authorization help, inventory management, and revenue-cycle plumbing around cancer care, it captures a far stickier profit pool than a simple wholesaler can.

That helps explain why buybacks are showing up alongside specialty expansion. Investors often read repurchase announcements as a generic sign of confidence. Here, they may signal something more specific: management teams think the market is still valuing them too much like scale distributors and not enough like specialty-care platforms with recurring workflow advantages. Cencora's new authorization, McKesson's accelerated repurchases, and Cardinal's higher outlook all point in the same direction. These companies are generating enough confidence in future cash flow to return capital while still funding strategic repositioning.

There is also a broader consequence for the healthcare system. As more economic power concentrates around specialty channels, independent physician practices become more valuable acquisition targets, and payers face counterparties with more operational leverage. The distributors are no longer neutral middlemen in that chain. They are choosing where they want to sit: closer to oncology practices, closer to data, and closer to the reimbursement machinery that decides how money moves.

For investors, the takeaway is not that every distributor suddenly deserves a software multiple. It is that the old distribution lens is getting stale. The winning healthcare supply-chain companies are building businesses that look less like freight handlers and more like specialized network operators. If that transition continues, the biggest upside may not come from selling more drugs. It may come from controlling the lanes through which the most profitable treatments, and the paperwork around them, have to travel.