The Retail Winners Are Monetizing the Trip, Not the Basket

This week’s retail earnings looked, at first glance, like a familiar resilience story. Walmart posted 7.3% revenue growth in its fiscal first quarter on May 21. Home Depot reported May 19 sales growth of 4.8%. Lowe’s said May 20 comparable sales rose 0.6% despite what it called a challenging housing backdrop. Target, on May 20, said net sales rose 6.7% and comparable sales increased 5.6%.

That sounds like a straightforward message that American demand is holding up. It is only partly true.

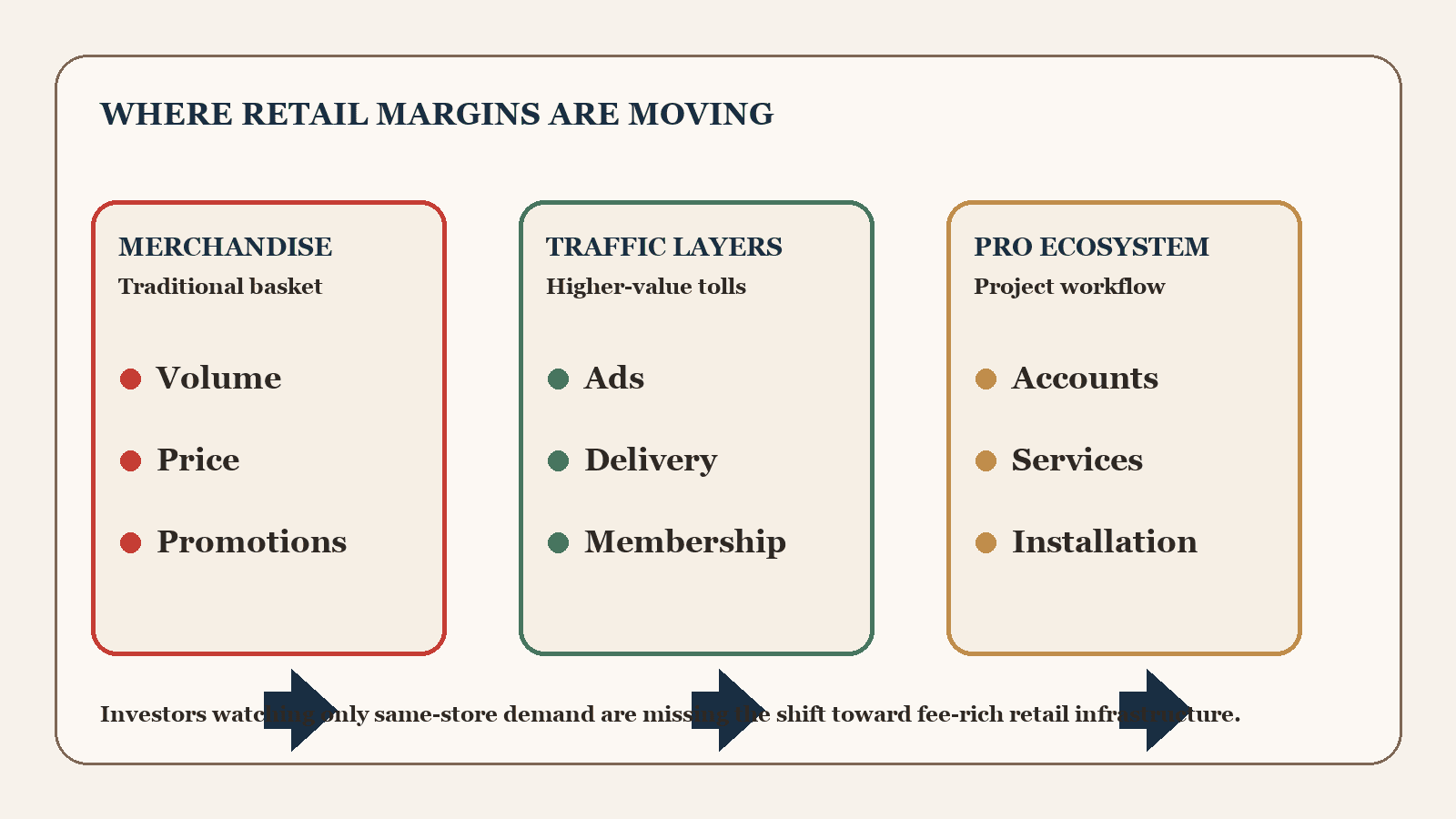

The more important story is that the strongest retailers are becoming toll collectors on consumer and contractor spending, not just merchants living off product markups. Casual readers still treat Walmart, Home Depot, Lowe’s, and Target as barometers for how many goods Americans want to buy. Increasingly, they are platforms that monetize traffic, delivery, advertising, memberships, services, and professional workflows around the purchase.

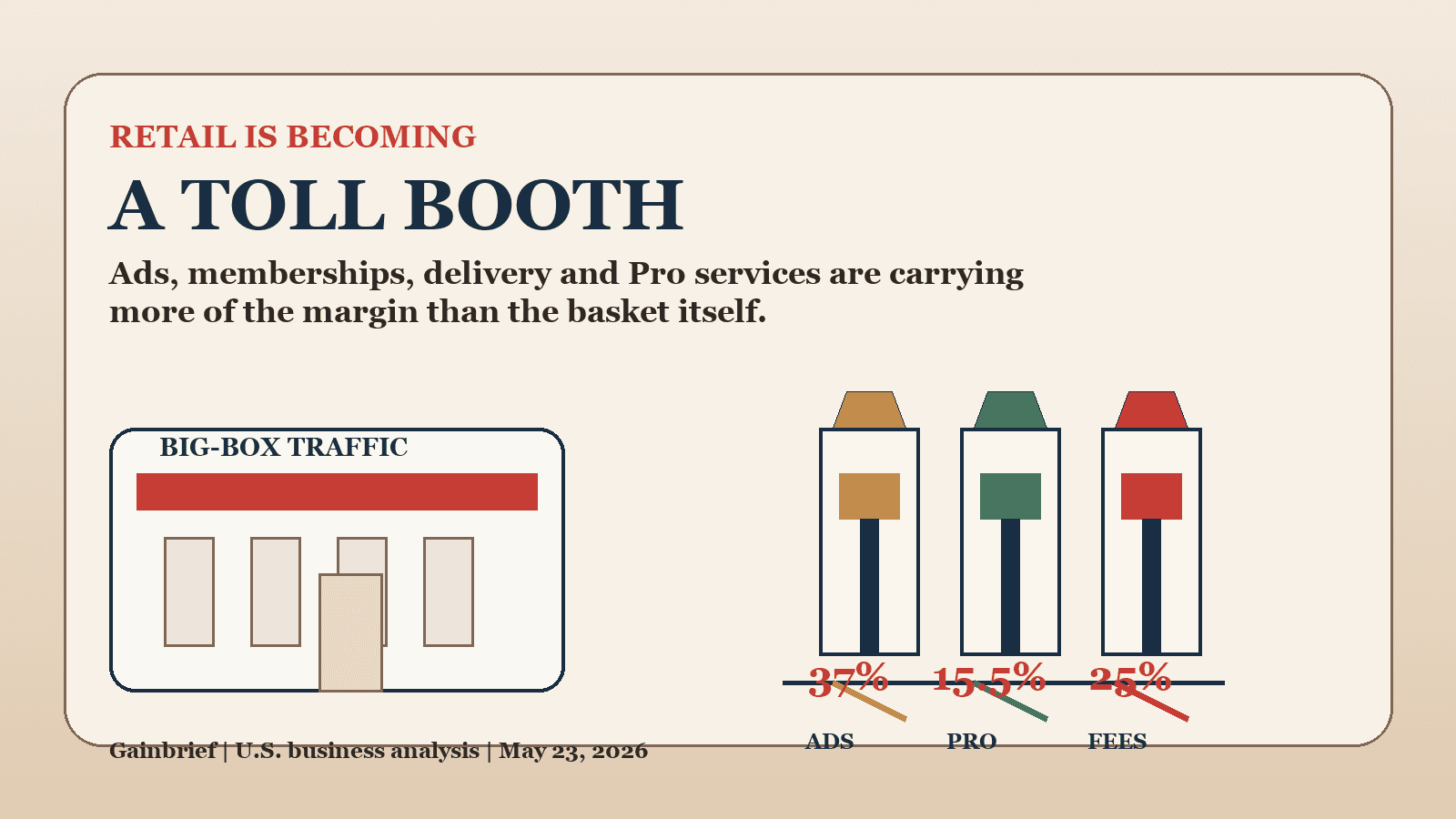

Walmart is the clearest example. Its first-quarter report showed e-commerce growth of 26% and global advertising growth of 37%. That matters because ad dollars, marketplace activity, and membership economics usually carry a different margin profile than selling another pack of paper towels. Walmart can look stronger than the consumer because it is collecting revenue from brands and third-party sellers who need access to its audience, even if shoppers remain price-sensitive.

Target showed the same pattern from a different angle. The headline numbers were solid, but the real tell was that non-merchandise sales, including Roundel advertising, Target Circle 360, and Target Plus, grew nearly 25% in the quarter. That is not just a retailer moving inventory. That is a retailer building fee streams around discovery, fulfillment, and loyalty.

Home Depot and Lowe’s are doing a version of the same thing in home improvement. Home Depot said customer transactions fell 1.3%, yet average ticket increased and revenue still beat expectations, with management pointing to professional customers and spring project demand. Lowe’s said online sales grew 15.5% and called out continued strength in Pro sales, home services, and appliances. In both cases, the companies are leaning harder into contractor relationships, service layers, and larger project ecosystems because the do-it-yourself consumer remains uneven under high mortgage rates and broader affordability pressure.

That changes how investors should read retail earnings. A good quarter at a large retailer no longer cleanly translates into broad consumer health. It can also mean the company is getting better at taxing the commercial activity around spending. The retailer owns the search results, the delivery promise, the sponsored placement, the loyalty funnel, the contractor account, or the installation lead. Those are businesses adjacent to retail, but they are starting to matter as much as retail itself.

It also helps explain why Walmart’s stock still slipped after its report while Reuters noted investors were turning their focus back to yields, inflation, and cautious guidance. The market is trying to decide whether these companies deserve higher multiples for their more durable revenue mix, or lower ones because the macro backdrop is still getting harder. Rising bond yields and fuel prices can hurt consumer sentiment, but they do not erase the fact that the best retailers now make money from the plumbing around demand.

The second-order consequence is easy to miss. If this model keeps working, the pressure shifts upstream. Consumer brands will have to spend more for visibility inside retailer ecosystems. Smaller merchants will depend more on big-box fulfillment and marketplace traffic. Traditional media loses ad dollars to retail media. And investors who still sort these companies into a simple “defensive consumer” bucket will miss that they increasingly look like hybrid infrastructure assets with storefronts attached.

The retail question for the rest of 2026 is not just whether shoppers keep spending. It is whether the biggest chains can keep deepening their control over how spending gets routed. If they can, the winners in retail may be determined less by who sells the cheapest goods and more by who owns the toll booth.