Starbucks’ AI Retreat Is a Warning About Retail Margins

Starbucks’ decision this week to retire its AI inventory-counting tool across North America looks small next to the company’s larger turnaround. It is not. For investors, it is one of the clearest recent reminders that in physical retail and food service, the first economic test of AI is not creativity. It is whether the system can count milk correctly at 6 a.m.

Reuters reported that the tool, which had been rolled out last September, frequently miscounted and mislabeled beverage items. Starbucks said it is now standardizing store counting while pushing for more frequent replenishment and broader supply-chain improvements. That sounds operationally mundane. It is also the point.

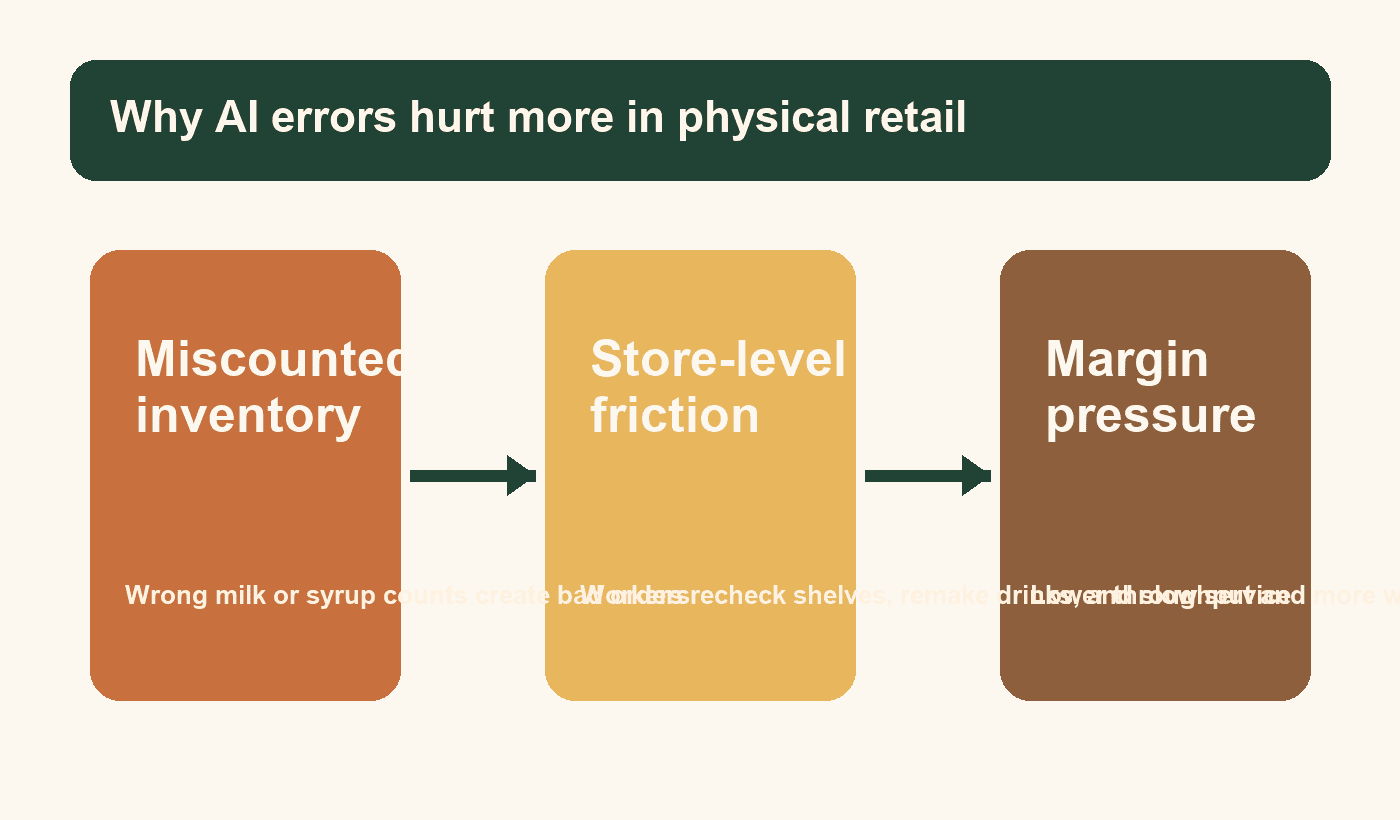

What casual readers may be missing is that Starbucks just drew a line between software that demos well and software that actually widens margin in a labor-heavy chain. In digital businesses, a flawed AI feature may annoy a user. In a coffee chain, a flawed AI count can cascade into stockouts, remakes, slower service, wasted labor, and a customer who simply orders elsewhere. The economics are harsher because the error travels through a real-world operating system.

That matters because Starbucks is trying to recover profit while still spending heavily to fix the business. In its fiscal second quarter, North America comparable sales rose 7.1%, but operating margin in the segment fell to 9.9% from 11.6% a year earlier as labor investments, mix pressure, tariffs, and coffee costs weighed on results. The company has told investors that the turnaround starts with sales, with earnings improvement following later. Scrapping an unreliable AI tool is consistent with that logic: protect execution first, automate second.

There is a broader market takeaway here. A growing share of AI commentary still assumes that every deployment is a labor-saving story. Starbucks suggests the opposite. In messy, high-frequency operating environments, the real bottleneck is often variance: shelf placement, packaging similarity, rushed human workarounds, inconsistent lighting, rushed deliveries, and fragmented systems. AI does not remove those frictions by default. Sometimes it adds one more layer that has to be audited by a worker anyway.

That should also change how investors read software promises aimed at restaurants, grocers, pharmacies, and convenience chains. The winning pitch in those sectors may not be “replace labor.” It may be “reduce exceptions.” That sounds less revolutionary, but it is closer to the real P&L. A system that cuts a few stockouts, trims rework, and shortens rush-hour chaos can be valuable. A system that requires constant human override is just another cost center wearing an innovation label.

That is why this episode is more relevant to enterprise software investors than it appears. The most durable AI vendors in the physical economy may not be the ones promising full automation. They may be the ones that help companies narrow error rates, improve replenishment cadence, and fit into existing workflows without forcing frontline workers to babysit the product. Reliability, not novelty, is the monetizable feature.

Starbucks itself has been explicit that its AI approach should be practical and disciplined. At its annual meeting, the company highlighted tools that support baristas and order sequencing rather than replace the human core of the store. That is a more believable roadmap than the old software pitch that every operational bottleneck can be scanned away. If “Back to Starbucks” works, it may owe less to flashy AI and more to tighter staffing, cleaner routines, better logistics, and a loyalty program that already drives a huge share of U.S. revenue.

The hidden lesson is simple: for consumer companies, AI is not yet a margin substitute for operational discipline. It is an execution tax unless it works with near-boring reliability. Starbucks did not just kill a tool. It quietly told the market what kind of AI spending deserves to survive.