AI Software Is Becoming a Margin Story, Not a Seat Story

Workday and Zoom both gave investors encouraging earnings updates this week, but the usual AI headline misses what matters. This is not really a story about software suddenly finding a new growth engine. It is a story about mature software companies learning how to turn AI into better margins, better customer retention, and a stronger grip on existing workflows.

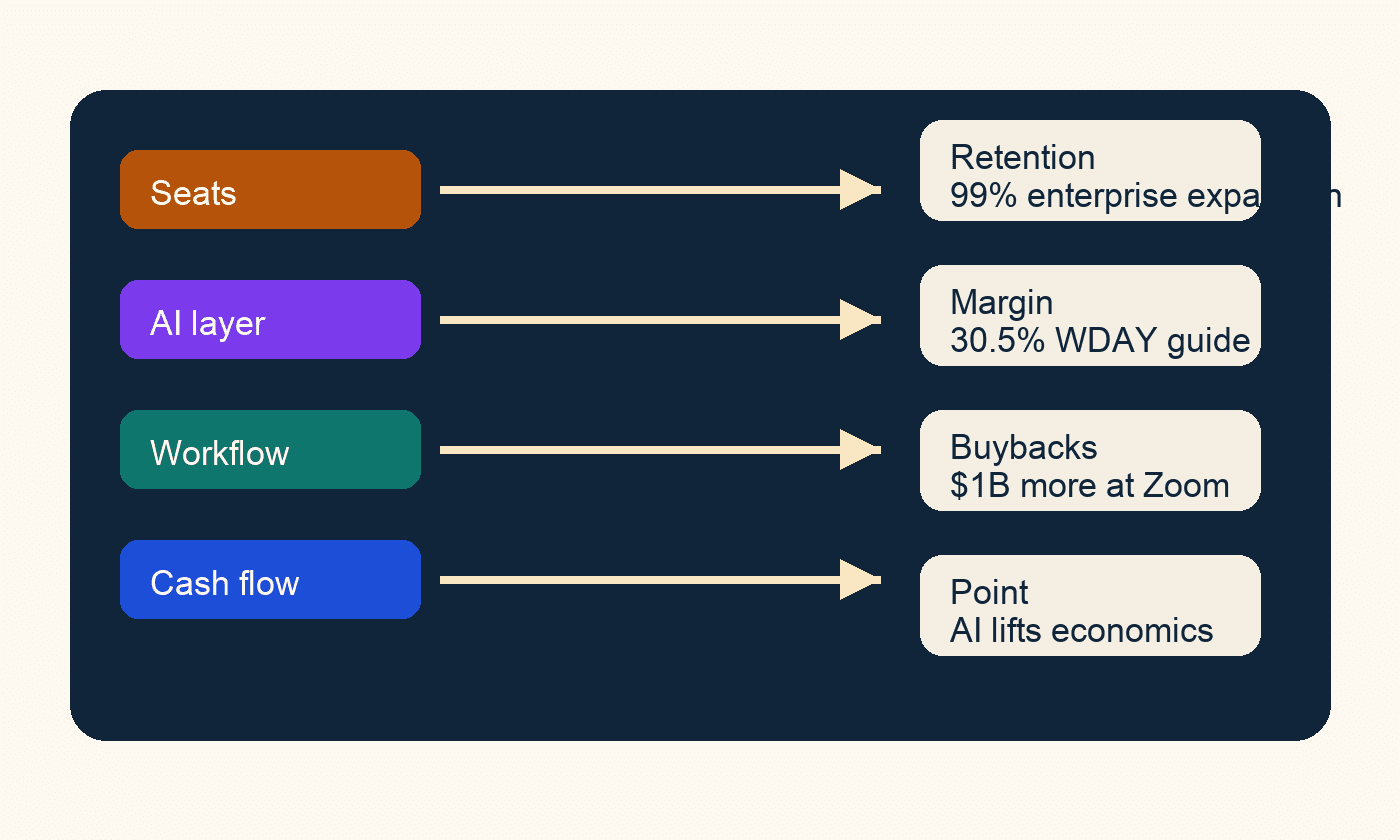

Workday reported fiscal first-quarter revenue of $2.542 billion, up 13.5% from a year earlier, while subscription revenue rose 14.3%. Just as important, it lifted its full-year non-GAAP operating margin outlook to 30.5% while keeping subscription-revenue guidance roughly intact. Zoom, meanwhile, posted first-quarter revenue of $1.239 billion, up 5.5%, with enterprise revenue up 7.2%, and raised its annual revenue and profit outlook while authorizing another $1 billion in buybacks.

What casual readers may be missing is that these companies are showing where the first durable AI payoff in enterprise software may actually land: not in explosive new seat growth, but in the unit economics of the installed base. AI is starting to look less like a separate product cycle and more like a way to charge more for the workflow, hold on to customers longer, and deliver profit growth even when headline revenue growth stays merely respectable.

That is why Workday’s quarter was more revealing than a standard beat-and-raise story. The company said more than 4,000 customers are now using at least one of its organically developed agents, more than double the prior quarter, and that its Recruiting Agent supported 14 million hiring processes in the period, up 44% year over year. Yet the bigger financial signal was not a dramatic jump in annual sales guidance. It was the ability to protect growth while expanding margin. In other words, AI is helping Workday become more valuable without needing to become much faster-growing.

Zoom’s results point in the same direction from a different starting point. This is a company that already lived through the comedown from its pandemic boom, so investors no longer need to be convinced it can attract attention. They need to be convinced it can deepen monetization. Management said paid users of AI Companion grew 184% year over year, enterprise revenue outpaced the broader business, and operating margins improved sharply. The extra buyback authorization also matters. A company does not emphasize repurchases when it thinks AI is still just a distant science project. It does that when it believes the business can throw off enough cash to invest and still return capital.

The hidden connection between Workday and Zoom is that both are selling AI into places where the customer already keeps score in dollars, hours, and throughput. Workday sits inside hiring, HR, finance, and approvals. Zoom increasingly wants to sit not just in meetings, but in the actions that follow them. That makes AI monetization more credible because the product does not have to feel magical. It has to reduce friction in expensive white-collar routines that companies already want to streamline.

This is also a warning for investors who keep waiting for AI software winners to look like the old cloud winners. The classic software trade was built on seat expansion and broad adoption curves. The next phase may look narrower and financially cleaner. Vendors that already own a trusted workflow can add AI, raise wallet share, defend renewal rates, and widen margins before the market sees a dramatic reacceleration in total revenue.

That has real implications for valuation. If AI in enterprise software first shows up as efficiency, retention, and pricing architecture, then some of the best-positioned companies may be the ones investors dismissed as ex-growth or merely steady. A slower top line does not necessarily mean a weaker AI story if the company can convert automation into cash flow and buybacks faster than its competitors can convert hype into revenue.

The sharper takeaway is that enterprise AI is becoming a financial-engineering story inside the software stack, not just a product story. Workday and Zoom are both suggesting that the most bankable AI model may be boring in appearance and powerful in effect: embed the tool inside a workflow customers cannot easily leave, make that workflow more productive, and let the margin do the talking.