The AI Chip Trade Is Moving Onto Wall Street's P&L

Nvidia's latest quarter looked strong enough on its own. The company reported $81.62 billion in first-quarter revenue, with data center revenue at $75.2 billion, and forecast $91 billion for the current quarter. It also authorized an $80 billion buyback. Those are enormous numbers, but they were never the whole argument investors were trying to solve.

The real question is whether AI infrastructure demand is still mostly a hyperscaler budget cycle. If Microsoft, Amazon, Google and Meta remain the only buyers that matter, then every semiconductor multiple eventually becomes a referendum on a handful of capital-spending committees. That is why one smaller story this week mattered more than it looked.

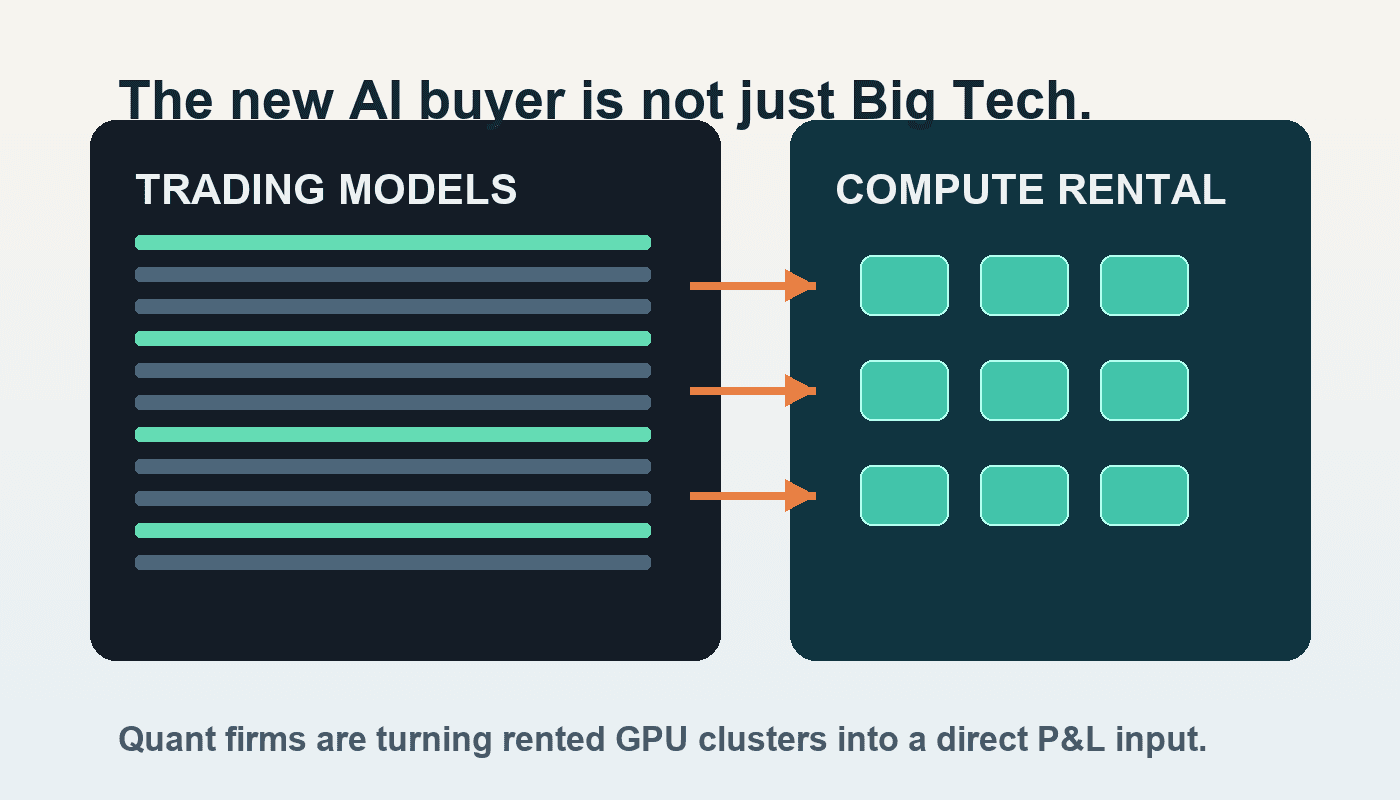

Lambda said Hudson River Trading is renting access to more than 1,000 Nvidia Blackwell systems to power quantitative research and development. That matters because HRT is not an AI lab trying to build the next frontier model. It is a trading firm. The overlooked shift is that GPUs are starting to move from being a tech-company capital project to being a cross-industry revenue input. Once that happens, the AI trade gets broader and harder to unwind than many casual readers assume.

Wall Street has always paid aggressively for speed, data and better prediction. In older cycles that meant microwave towers, colocation and custom networking. In this cycle it increasingly means training models and running large-scale simulations fast enough to improve trading decisions. When a quant firm decides that renting Blackwell capacity is worth it, the signal is not just "AI demand is still hot." The signal is that the return on compute is becoming measurable inside businesses far away from consumer chatbots.

That changes how investors should think about durability. Nvidia management said sales to AI-specific cloud firms were roughly equal to sales to the big cloud providers and were growing faster quarter over quarter. HRT's deal with Lambda helps explain why. A second layer of customers is forming between Nvidia and the end user: specialized cloud operators that package scarce compute for buyers who want results, not data-center ownership. That is a healthier market structure than one dominated only by the hyperscalers, because it opens AI demand to firms that can justify spending but do not want to build infrastructure from scratch.

It also weakens one of the cleaner bear cases against the AI buildout. Bears have argued that once big tech moderates spending, the whole stack will suddenly look overbuilt. But if hedge funds, insurers, banks, industrial firms and healthcare platforms start buying compute the way they already buy cloud software, then demand can keep widening even if the pace of spending at the giants normalizes. The mix changes before the total does.

There is still risk here. Nvidia is expensive, competition from custom chips is real, and management itself acknowledged future supply constraints around Vera Rubin. Lambda and HRT did not disclose the contract's financial terms, and one trading-firm deal does not create an entirely new market on its own. But it does reveal where the next leg of demand may come from: not just from companies building AI, but from companies discovering that AI compute can sit directly inside the profit engine.

That is the part many investors are missing. The AI chip story is no longer only about who can afford the largest data center. It is increasingly about which industries can turn rented compute into margin. When that buyer list expands to firms whose business model already rewards tiny performance edges, GPU demand stops looking like a speculative tech spree and starts looking more like a new cost of doing business.