The AI Compute Boom Is Turning Into Project Finance

Wall Street still talks about the AI race as if it were mainly a chip-sales story. This week’s news suggests it is becoming something more durable and more financial: a new class of infrastructure that looks increasingly like power plants, pipelines, and cell towers.

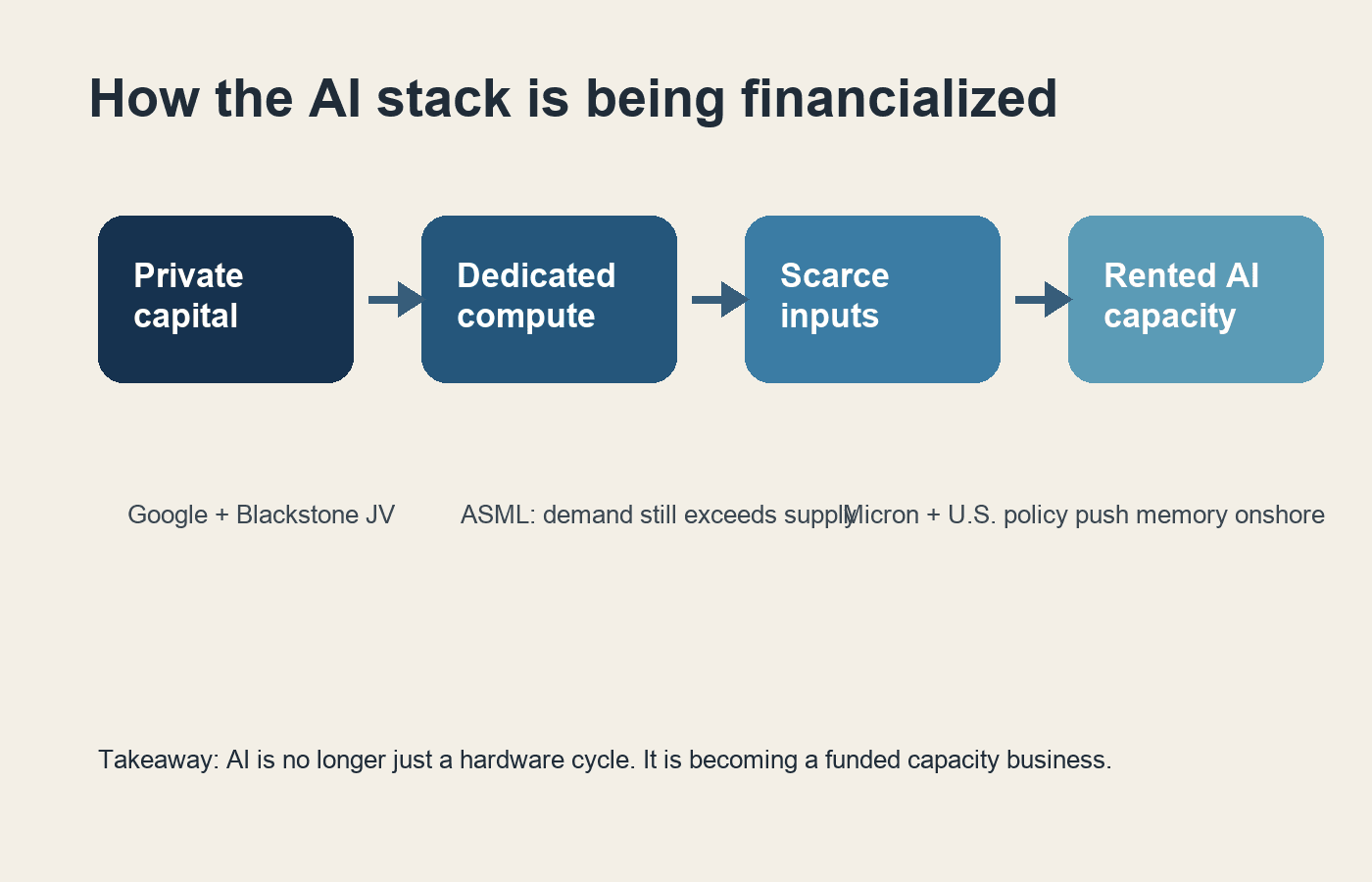

The clearest signal came from Google and Blackstone. Their new joint venture will offer Google’s TPUs through a separate compute-as-a-service company, backed by Blackstone’s initial $5 billion equity commitment and aimed at bringing 500 megawatts of capacity online in 2027. That matters because it moves AI compute one step away from the normal cloud model, where hyperscalers spend the capital and customers rent usage, and one step closer to an infrastructure model, where outside capital underwrites long-lived capacity and sells access into a market that is starting to resemble a utility.

That is the part casual readers are missing. The important shift is not just that demand for AI hardware remains strong. It is that the financing structure is changing. Once private capital is willing to fund dedicated AI capacity before all the end customers are even visible, compute stops looking like a tech feature and starts looking like an asset class.

The rest of this week’s semiconductor news fits that interpretation. ASML said AI-related infrastructure investment is still pushing chip demand ahead of supply and lifted its 2026 sales outlook to as much as 40 billion euros. Micron, meanwhile, said it has started manufacturing 1-alpha DRAM in Virginia, calling it the most advanced memory made in the United States, while U.S. trade officials used the event to argue for carefully timed semiconductor protection during a reshoring phase. Put those together and the market message is straightforward: capacity is scarce enough, and strategically important enough, that both financial engineering and industrial policy are moving closer to the center of the AI trade.

That has a few consequences for investors. First, the winners may broaden beyond the obvious GPU names. If AI capacity is being financed like infrastructure, then the beneficiaries include memory makers, equipment suppliers, networking vendors, data-center landlords, power developers, and private-capital firms that can fund multiyear buildouts. Second, margins may migrate. In a normal software cycle, value tends to concentrate in applications. In this cycle, scarcity is still deeper in the stack, so the businesses that own constrained inputs or can bankroll them may keep bargaining power longer than many software bulls expect.

There is also a competitive implication for big tech. Google is not just trying to sell more cloud. It is effectively creating another route to market for its TPUs by pairing them with outside balance-sheet capacity. That lowers the burden on Google to own every dollar of infrastructure itself and gives customers another procurement path. If that model works, more AI leaders will try to separate the economics of building compute from the economics of selling software on top of it.

It also changes how risk is distributed. In the older model, a cloud provider absorbed more of the demand risk on its own balance sheet. In the newer one, private capital, landlords, lenders, and utility-linked infrastructure partners can take part of that risk in exchange for long-duration returns. That is exactly how an industry starts to institutionalize.

This is why the AI boom should not be read only through quarterly chip guidance. The story is maturing into a capital-markets story about who funds the next layer of scarce capacity, who controls access, and who gets paid like an infrastructure owner rather than a cyclical hardware vendor. The deeper takeaway is that AI compute is starting to be financed the way America finances other bottleneck industries. When that happens, the boom usually lasts longer, spreads wider, and becomes harder to dislodge than headline skeptics expect.