Health Inflation Is Hiding in the American Paycheck

The most important inflation line in a lot of American households may not be groceries or rent. It may be health insurance, because that cost often shows up where people notice it last: in slower wage growth, skinnier benefit design, and a larger share of the bill shifted quietly onto employees.

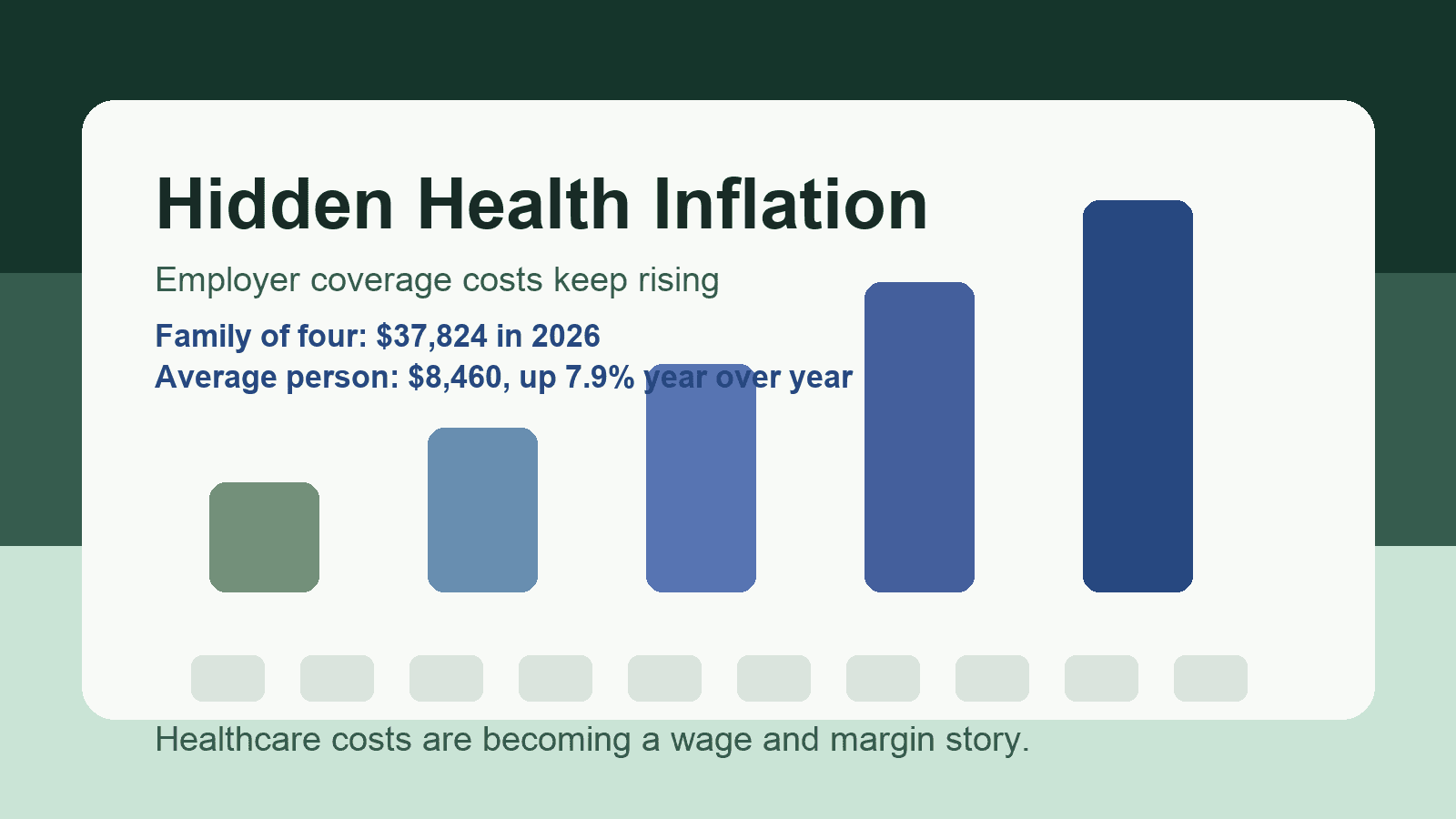

That is why this week's 2026 Milliman Medical Index matters more than it may look at first glance. Milliman estimates that healthcare for a typical family of four covered by an employer-sponsored plan will cost $37,824 in 2026. For the average person, the figure is $8,460, up 7.9% from 2025. Milliman says that is the largest increase in more than a decade if you set aside the distortion from the pandemic years.

That number should land as a finance story, not just a benefits story. Employer-sponsored insurance still covers a huge share of working Americans, which means medical inflation does not stay inside the healthcare sector. It leaks into labor costs, margins, hiring plans, and the real buying power of compensation packages. When employers absorb more of the bill, wage growth has less room to run. When they push more of it back onto workers, take-home economics get worse even if headline pay looks fine.

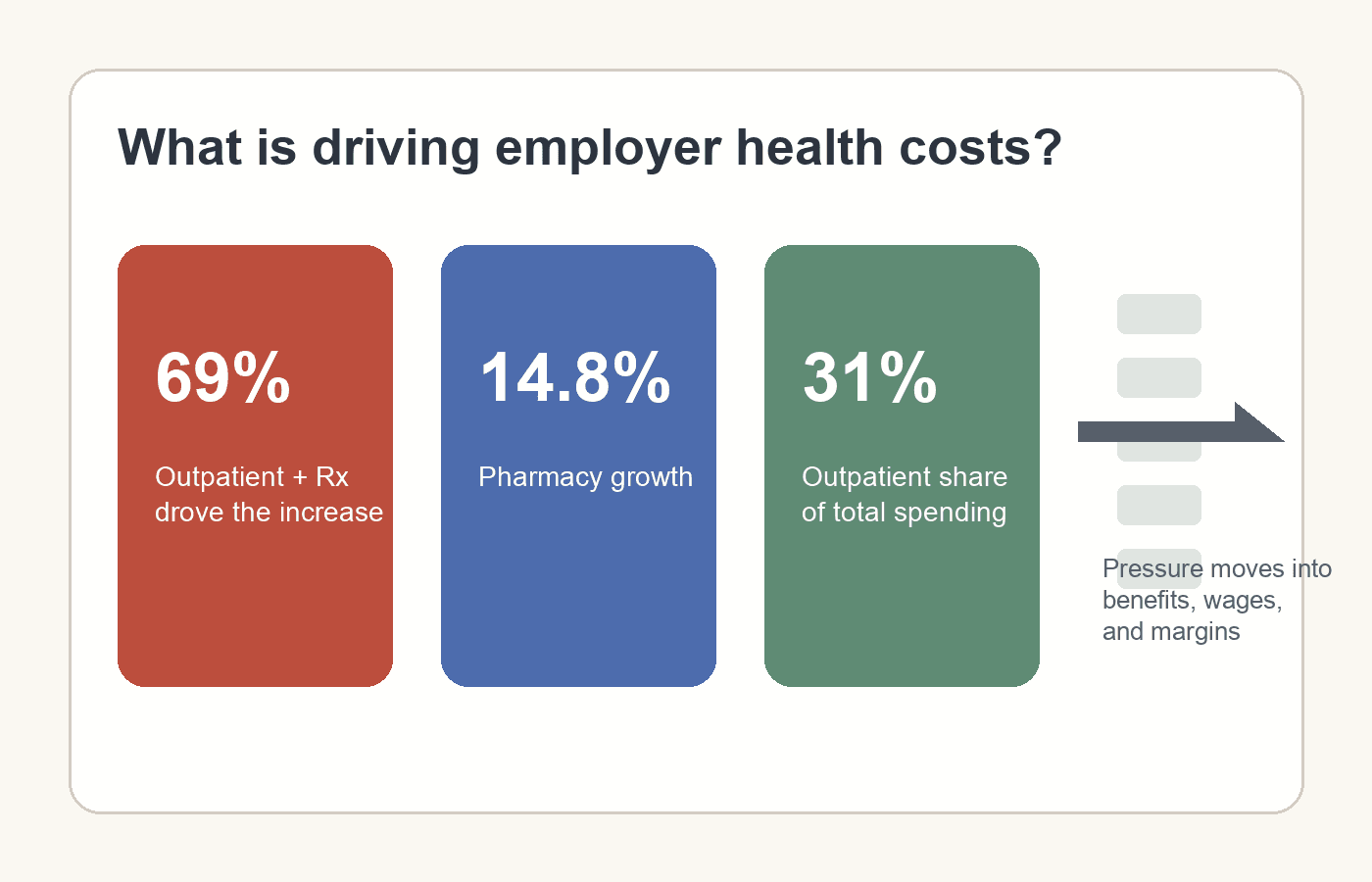

The detail inside the report is what makes the trend feel stubborn rather than temporary. Milliman says outpatient facility care and pharmacy services drove 69% of the increase this year. Pharmacy was the fastest-growing cost component, up 14.8% year over year, with GLP-1 drugs now a meaningful and growing part of employer pharmacy spend. Outpatient care now represents roughly 31% of total spending for the average person in the index. That mix matters because it suggests employers are not dealing with a one-off claims spike. They are dealing with a broader cost structure that is becoming more expensive across multiple categories at once.

Investors should read that alongside what large insurers have been saying this earnings season. CVS Health raised its 2026 forecast earlier this month after improving medical cost controls in Aetna, but even there management said costs remain above historical levels. Reuters reported that CVS's Aetna medical loss ratio came in at 84.6% for the quarter, better than expected, yet the company still said the federal government's 2.48% average increase in 2027 Medicare Advantage payment rates does not fully match its cost outlook. UnitedHealth struck a similar tone in April. It beat expectations, posted an 83.9% medical cost ratio, and said Medicare Advantage utilization in 2026 should look similar to 2025, but it also said the 2027 government rate increase remains too low.

Put differently, the industry is not talking like inflation in care delivery is fading. The better-managed companies are talking like they are getting better at navigating it.

That distinction matters for markets. If insurers can stabilize margins through pricing, benefit redesign, narrower networks, coding discipline, and tighter utilization management, some healthcare stocks may look less fragile than they did last year. But that does not mean the underlying problem is solved for employers or workers. It may simply mean the pressure is being redistributed more efficiently through the system.

This is where the story becomes more personal than many market notes allow. A family does not experience "medical trend" as an abstract ratio. It experiences it through higher payroll deductions, a bigger deductible, stricter formularies, fewer plan choices, or a surprise bill after outpatient treatment that used to feel routine. Employers experience the same trend as a tax on compensation. The economy experiences it as a drag on discretionary spending. Every dollar that goes toward holding a health plan together is a dollar that does not go to wages, hiring, or other consumption.

There is also a policy angle hiding in plain sight. If Medicare Advantage reimbursement is still lagging cost growth, insurers will keep adjusting benefits and market footprints. If employer plans keep getting hit by outpatient and drug spending, pressure for tougher hospital pricing scrutiny, more transparency, and a more aggressive stance on pharmacy economics will keep building. None of that is especially new. What feels new is the speed. A 7.9% annual increase for the average person is not a background nuisance. It is large enough to shape boardroom decisions.

For Gainbrief readers, the takeaway is simple. Healthcare inflation is not only a hospital or insurer issue. It is an underappreciated labor-market and consumer-spending issue. The companies most exposed are not just health insurers, pharmacy benefit managers, and hospital systems. They are also employers with thin margins, labor-intensive business models, and limited pricing power.

That is why this report deserves more attention than it will probably get. The market spends a lot of time on visible inflation and very little on the kind hidden inside benefits. But hidden does not mean small. If the cost of covering a typical family is approaching $38,000 a year, then one of the biggest pressures on the American middle class is still arriving through the payroll system. Investors looking for the next clean inflation downtrend should keep that in mind. Healthcare may be where the old inflation story is still alive and well.