Wall Street Is Trading AI. The Fed Still Has to Trade Gasoline.

The strangest market signal on May 22 was not that consumer sentiment hit a record low. It was that stocks barely cared.

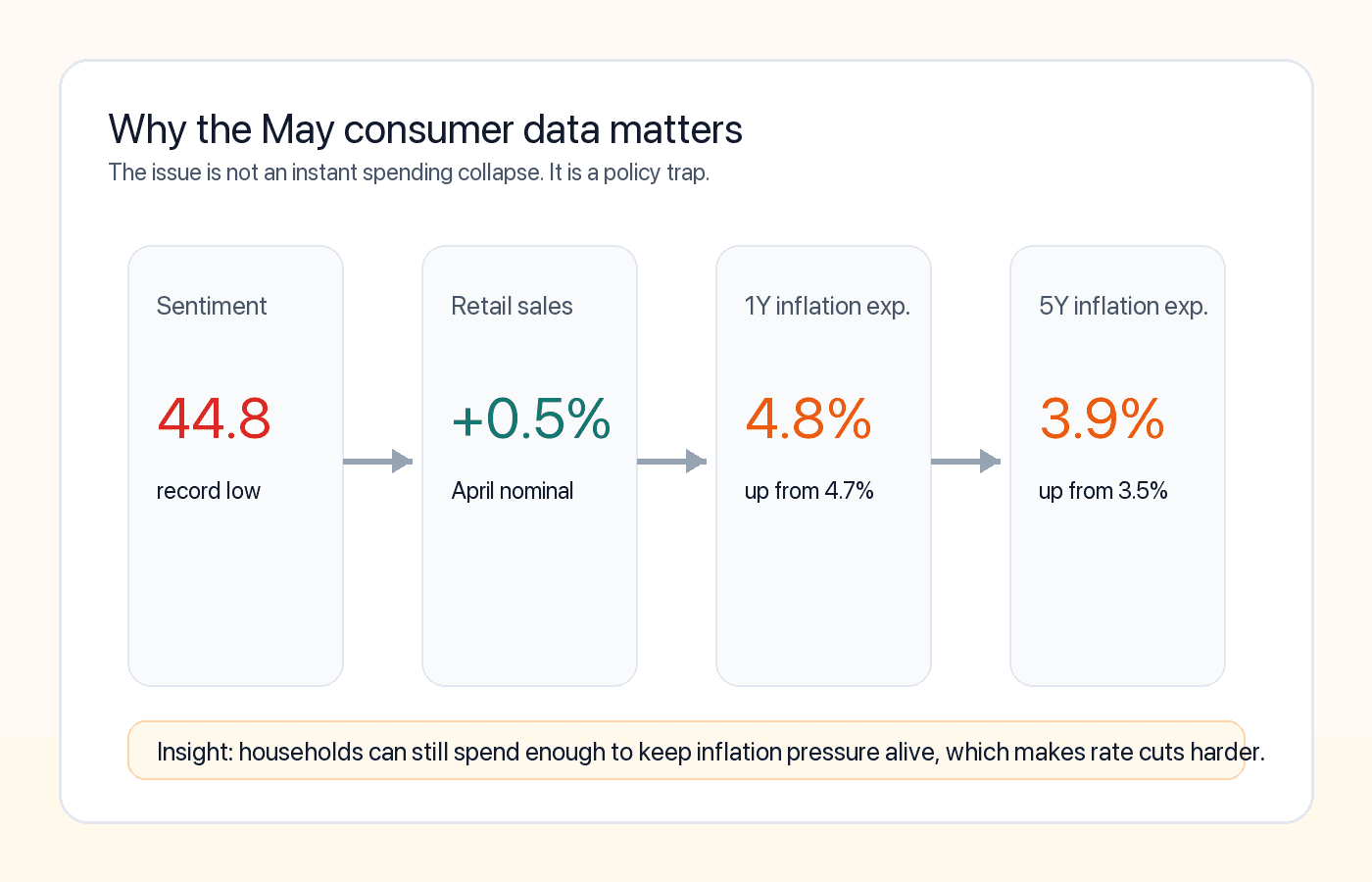

The University of Michigan’s final May reading fell to 44.8, the weakest on record, while major indexes kept pushing higher. At first glance, that looks like one more example of markets ignoring Main Street. But the bigger point is more important than that: Wall Street can afford to ignore a miserable consumer for a while. The Federal Reserve cannot.

That is the piece casual readers are missing. The real risk in this data is not that Americans suddenly stopped spending yesterday. It is that inflation psychology is getting worse again before demand has clearly broken. That is an awkward combination for anyone still assuming the next move from the Fed will be a clean, easy rate cut.

The hard data still looks resilient on the surface. U.S. retail sales rose 0.5% in April, following a 1.6% increase in March. Electronics and online sales held up well. Restaurant spending also stayed positive. But once you strip away the headline, the picture gets less comforting. Gas station receipts jumped again, helped by higher fuel prices, and real core retail sales growth was barely positive. In other words, households are still spending, but more of that spending is being absorbed by energy and other essentials.

That helps explain why sentiment is collapsing faster than the spending numbers. Consumers are not responding to some abstract economist’s model. They are responding to what it feels like when gas, food, and other basics take a larger share of the paycheck. Michigan’s survey said 57% of consumers spontaneously mentioned high prices eroding their finances, up from 50% a month earlier. Lower-income households and people without college degrees saw especially sharp declines.

The more important detail was not the headline sentiment number. It was inflation expectations. One-year expectations rose to 4.8% in May from 4.7% in April. Five-year expectations jumped to 3.9% from 3.5%, well above the range consumers were showing through most of 2024. That matters because the Fed can live with an oil shock more easily than it can live with a public that starts believing higher inflation will spread and stick.

This is why the market’s calm reaction may be misleading rather than reassuring. Investors are looking at an index increasingly driven by giant companies tied to AI infrastructure, cloud spending, and semiconductors. Those businesses do not need a strong middle-class shopping trip every weekend to keep earnings momentum alive. A consumer sentiment collapse can coexist with record highs in the Dow or S&P for longer than many people expect.

But monetary policy works on a different scoreboard. If households feel poorer, expect higher inflation, and keep spending just enough to prevent a clear slowdown, the Fed gets trapped. It cannot cut aggressively because inflation expectations are moving the wrong way. It also does not get the kind of clean demand destruction that would quickly cool prices. That is how you end up with a consumer that feels recessionary even while official spending data still says expansion.

There is a business consequence here too. Companies selling to price-sensitive households may run into a margin squeeze before they run into a volume collapse. Consumers often do not stop buying all at once. They trade down, postpone discretionary purchases, or lean harder on promotions. That is bad news for apparel, furniture, and other categories already showing weaker momentum. It is also a warning that the next stage of the consumer slowdown may show up in mix and profitability before it shows up in headline sales.

So the May sentiment report should not be read as a simple bearish signal or dismissed as another soft survey. It is better read as evidence that the inflation problem is moving from prices into expectations and from there into policy. Wall Street is still trading AI and capex. The Fed still has to trade gasoline, groceries, and rent.

That gap can stay open for a while. It just should not be mistaken for stability.