AMD's Taiwan Bet Shows the AI Trade Is Moving Below the GPU Surface

The AI trade still gets reduced to one question: how many GPUs can the market absorb? AMD's latest move suggests that is no longer the right frame. This week the company said it will invest more than $10 billion across Taiwan's AI ecosystem, then followed that up by saying CPU demand has been stronger than expected and that supply will rise quarter by quarter through 2026. That matters because it shifts the conversation from chip launches to industrial capacity.

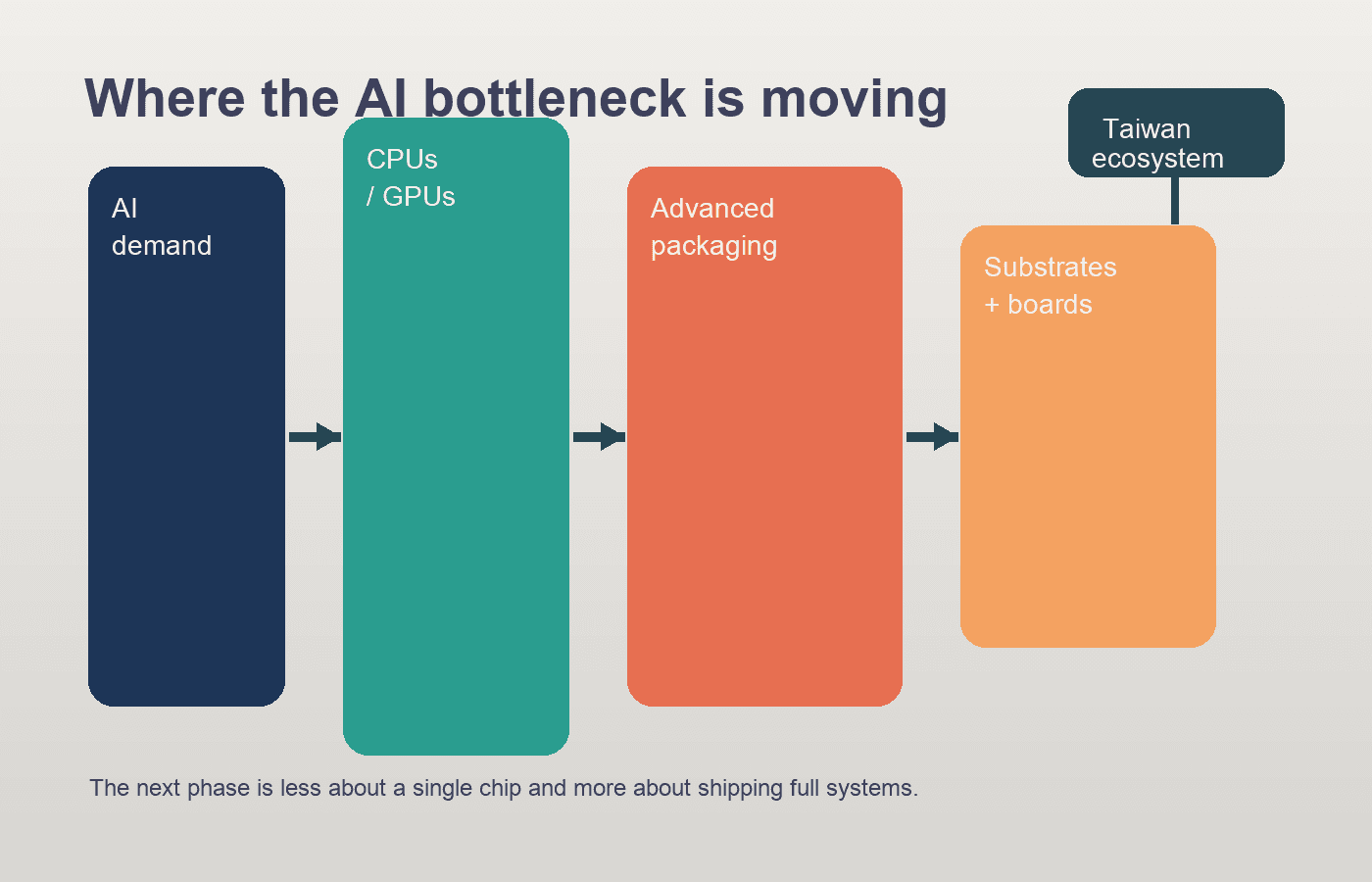

For U.S. investors, the point is not simply that AMD is spending aggressively. It is where the money is going. The company said the investment will target advanced packaging, substrates, and manufacturing for rack-scale systems. In plain English, AMD is putting capital behind the parts of the supply chain that have become the real chokepoints in AI infrastructure. The old version of the AI boom was mostly about who had the best accelerator. The current version is about who can actually assemble complete systems at volume and on time.

That distinction helps explain why this announcement is more interesting than a standard capacity headline. Advanced AI servers are no longer a single-chip story. They are built from increasingly complex collections of compute dies, memory, networking, substrates, thermal systems, and packaging technologies that need to work together inside power-hungry racks. AMD's statement named a long list of Taiwanese partners, from packaging and substrate specialists to server builders. The message was clear: if you want to compete in AI infrastructure now, you need an ecosystem, not just a product roadmap.

Lisa Su added an important second layer on Friday when she said CPU demand is running hotter than the industry expected a year ago. That sounds almost odd after two years in which AI headlines trained everyone to think GPUs were the only scarce asset that mattered. But inference is changing the mix. Once companies move from training frontier models to deploying AI products broadly, they need a lot more than elite accelerators. They need general-purpose compute, orchestration, data movement, and cheaper system-level scaling. Agentic AI only reinforces that. A world full of AI agents does not just consume bursts of training capacity; it leans continuously on the plumbing around the model.

This is where the market may need to broaden its lens. If AMD is right, the winners in the next phase of AI spending may include the less glamorous layers of the stack: packaging vendors, substrate makers, board suppliers, thermal and power infrastructure players, and anyone with the manufacturing discipline to help move from prototype clusters to repeatable deployments. Reuters reported this week that ASML's chief executive expects the chip market to remain tight because AI, robotics, and related demand are still outpacing supply. AMD's news fits that same pattern. The bottleneck is not disappearing. It is spreading.

There is also a geographic angle U.S. readers should not ignore. Much of the AI world's physical buildout still runs through Taiwan. AMD highlighted Taiwan for both its ecosystem investment and the ramp of its "Venice" EPYC CPUs on TSMC's 2-nanometer process. Future production is also planned at TSMC's Arizona fab, which is strategically important, but the center of gravity remains offshore. That leaves U.S. hyperscalers and enterprise buyers exposed to the same concentration risk they have been talking about for years, even while they increase capex. It also means every new data-center boom narrative should be read alongside supply-chain resilience, export controls, and industrial policy.

None of this guarantees AMD suddenly closes the gap with Nvidia in investor mindshare. Nvidia still owns the clearest position in the market's imagination, and for good reason. But AMD may be carving out something more durable than a simple "number two GPU vendor" narrative. If AI infrastructure keeps evolving toward full-rack systems, mixed compute, and multi-year co-investment with suppliers, then the competitive map gets wider. Execution in packaging, CPU supply, and systems integration starts to matter more.

The deeper takeaway is that AI capex is maturing. Early in a boom, money chases the most visible bottleneck. Later, it starts filling in everything around it. AMD's Taiwan bet looks like a sign that we are moving into that second phase. For investors, that argues for a less theatrical but probably more useful question than "which model wins?" The better question may be: who controls the messy middle of turning AI demand into shipped hardware?

That is where this story feels timely. The market has spent months rewarding the headline beneficiaries of AI. What AMD is saying now is that the next stretch may belong to the companies that can secure land, buildings, packaging capacity, substrates, and dependable system assembly before everyone else does. In other words, the AI trade is becoming more industrial. That may be less exciting than another benchmark war, but it is usually where large, durable returns get decided.