The AI Trade Has Reached the Utility Bill

The AI trade just bought itself a utility problem.

This week NextEra Energy agreed to acquire Dominion Energy in an all-stock deal valued at about $67 billion. On the surface, that looks like a standard scale merger in a defensive sector. It is not. It is one of the clearest signs yet that the AI boom is moving out of the data center and into the power grid, where the economics are slower, more political, and much harder to ignore on a monthly bill.

The headline reason is simple. America suddenly needs a lot more electricity, and not because households are buying more refrigerators. The U.S. Energy Information Administration said in January that power demand is set for its strongest four-year growth stretch since 2000, driven largely by large computing facilities. That changes the way investors should look at AI. The first phase of the trade was about chips, cloud contracts, and model releases. The next phase looks more like substations, transmission lines, gas generation, batteries, and regulated rate cases.

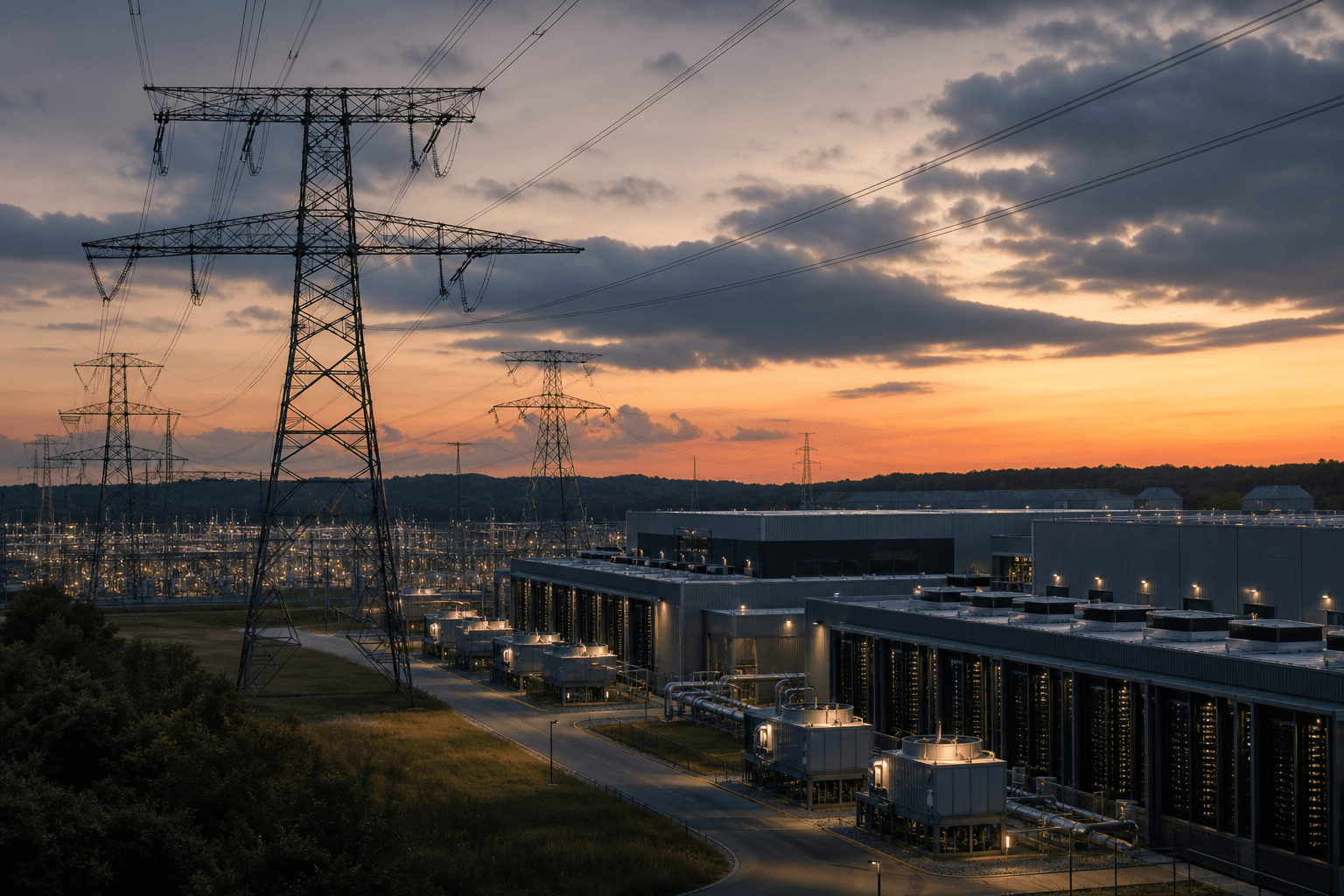

That is why the NextEra-Dominion tie-up matters beyond utility investors. In their announcement, the companies said the combined business would serve about 10 million customer accounts, own 110 gigawatts of generation, and carry more than 130 gigawatts of large-load opportunities in its pipeline. That is not normal merger language. It is AI-era language. Utilities are starting to describe their future in terms that sound more like hyperscaler capex decks than sleepy dividend presentations.

Dominion is especially important in this story because Virginia has become the physical heart of the U.S. data-center economy. S&P Global noted this week that Dominion Energy Virginia has about 51 gigawatts of data-center capacity in various stages of authorization and contracting, including 10.4 gigawatts already under electric service agreements. You do not need every one of those projects to arrive on time for the point to land. Even a partial buildout implies massive demand for generation and grid investment.

The harder part is what this means for everyone else. The independent market monitor for PJM, the largest U.S. power market, said last week that its recent capacity auctions were not competitive primarily because of forecast demand from data centers. It also said total wholesale power costs in the first quarter rose 75.5% from a year earlier. Not all of that increase drops directly onto consumer bills, and weather and fuel costs still matter. But the direction is hard to miss: large new loads are colliding with a grid that was not built for this pace of demand.

That is where the politics begin. The merger pitch from NextEra and Dominion leans heavily on scale. Management says a bigger platform will buy equipment more efficiently, finance projects more cheaply, and spread costs better across a larger base. The companies are even offering $2.25 billion in bill credits over two years for Dominion customers in Virginia, North Carolina, and South Carolina. That is a meaningful concession, but it also reads like an early admission that affordability will be the central regulatory fight.

Investors should take that seriously. AI infrastructure still has a popular narrative problem: markets tend to treat demand as unquestionably good and supply as somebody else's engineering detail. In power, supply is never just an engineering detail. It runs through public utility commissions, local opposition, environmental permitting, fuel procurement, balance-sheet capacity, and the simple fact that power plants and transmission lines take time. A utility cannot scale the way a software platform scales.

That mismatch may become one of the most underappreciated constraints in the AI buildout. If the grid becomes the bottleneck, then some of the biggest economic gains from AI get delayed, repriced, or redirected. Data-center operators may have to pay more for dedicated generation. Utilities may push for special large-load tariffs so new industrial users bear more of the cost. Regulators may insist that residential customers be protected before any merger synergies are allowed to count as a public benefit. In plain English, AI is entering the part of the economy where growth gets negotiated.

For markets, that creates a wider opportunity set than the usual semiconductor leaderboard. The obvious beneficiaries include utilities with credible growth territories, transmission developers, gas and nuclear suppliers, power-equipment makers, and companies that can finance generation quickly. But there is also a real risk layer. If customers keep seeing electricity bills rise while data centers multiply, utilities may face a backlash that limits how fast they can pass through costs or win approval for new infrastructure.

This is why I think the NextEra-Dominion deal deserves to be read as a warning as much as a bullish signal. It is bullish because it confirms that AI demand is strong enough to reshape the largest regulated parts of the economy. But it is also a warning because once AI demand shows up in household utility politics, the trade stops being purely about innovation and starts becoming about who pays.

That is a different market. It rewards scale, patience, and regulatory skill more than flashy product cycles. It also pulls the center of gravity away from Silicon Valley and toward state capitals, grid operators, and utility commissions. The AI story is still expanding. It is just expanding into a part of America where every growth plan eventually meets a ratepayer.

For U.S. readers, the takeaway is straightforward. If you want to understand the next leg of the AI economy, do not only watch Nvidia, cloud capex, or model benchmarks. Watch utilities, wholesale power markets, and the political fight over electric bills. The smartest way to read this merger is not that utilities are joining the AI trade late. It is that the AI trade has finally reached the real economy, and the real economy sends an invoice.