The Health-Care Bill Is Becoming a Paycheck Story

The sharpest cost surprise in the U.S. economy right now may not be at the gas pump or in the Treasury market. It may be sitting inside employer health plans.

That is why this week’s new Milliman Medical Index landed as more than a healthcare statistic. It looked like a wage story, a corporate margin story, and a consumer spending story at the same time.

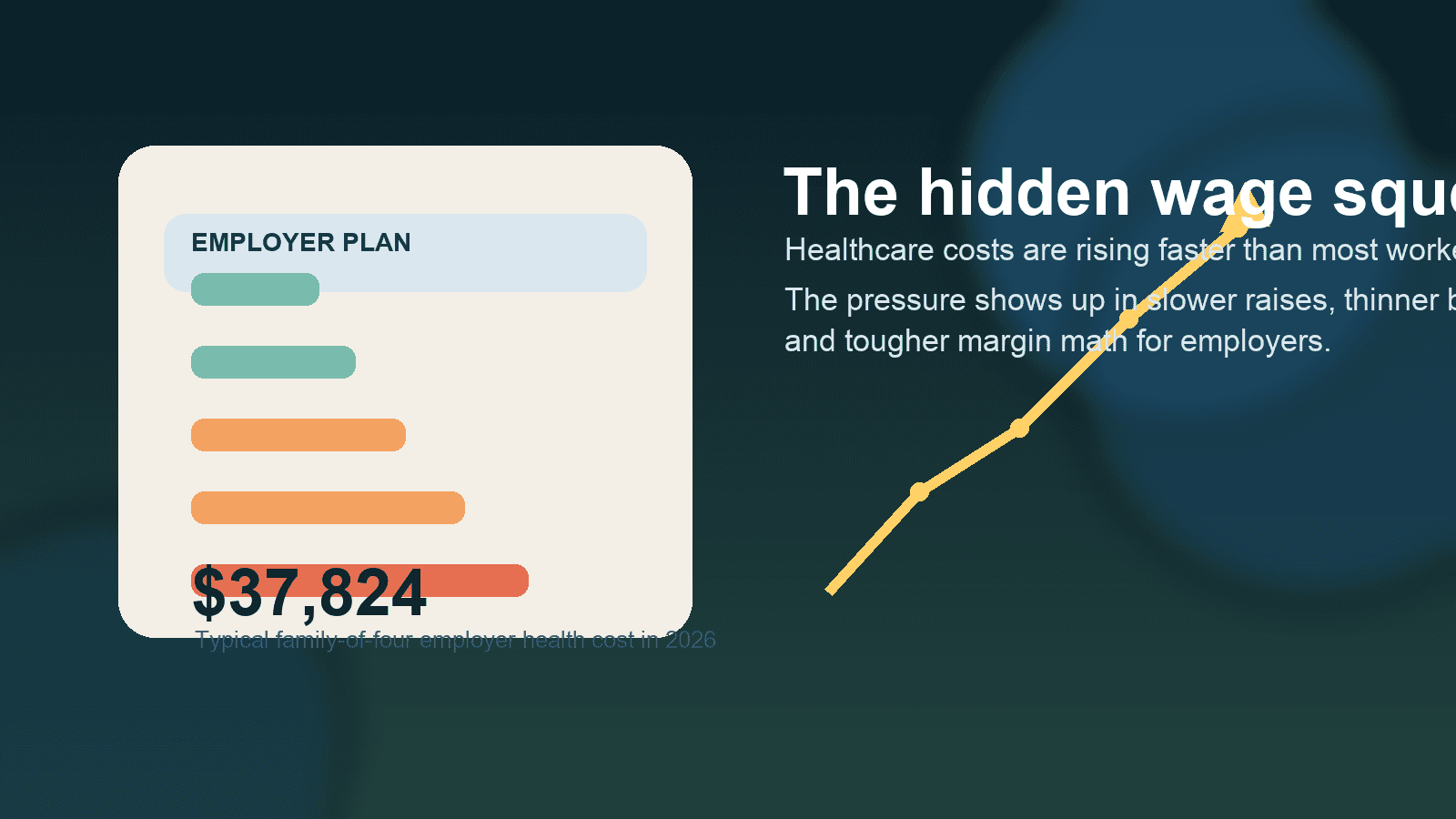

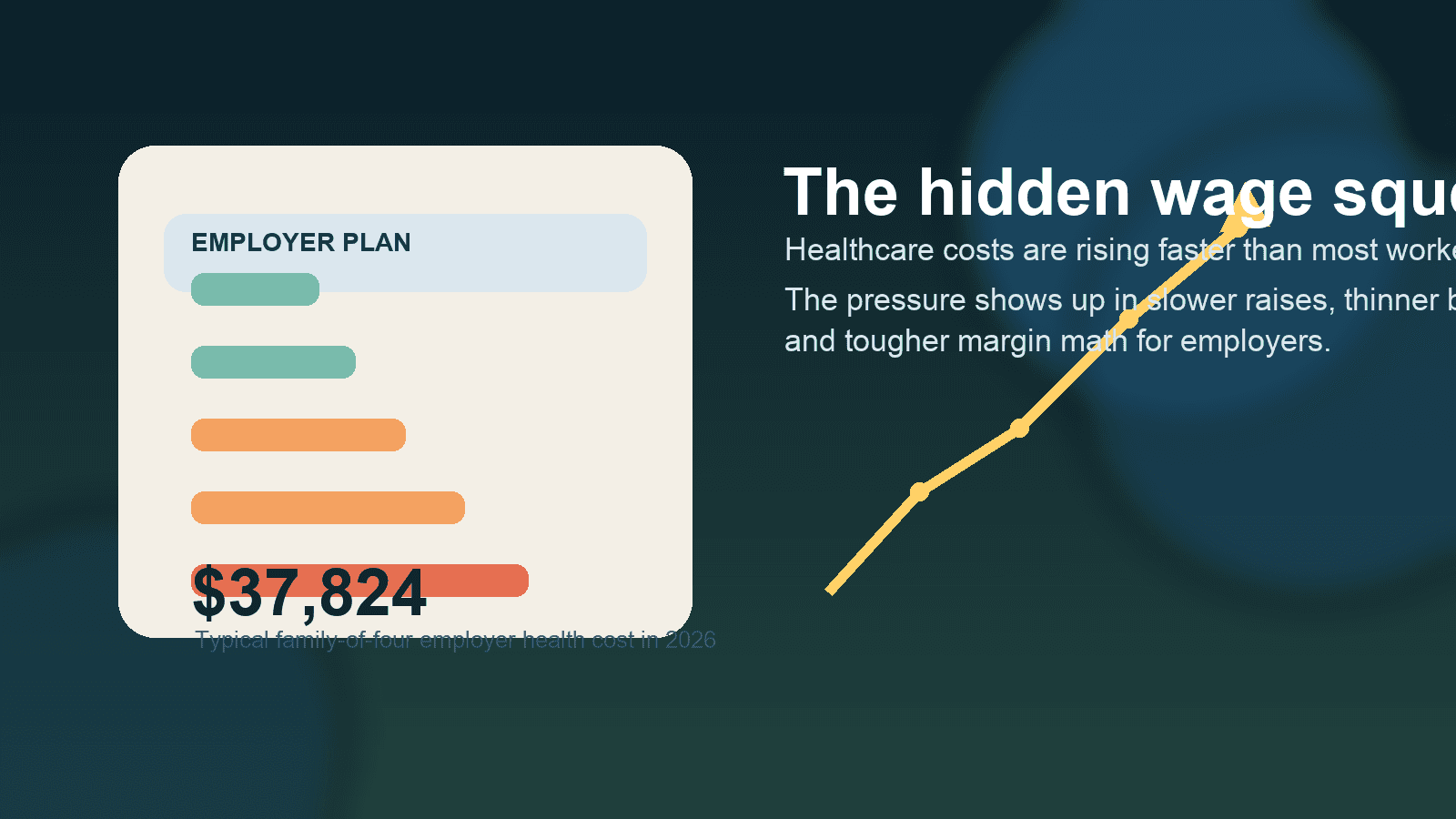

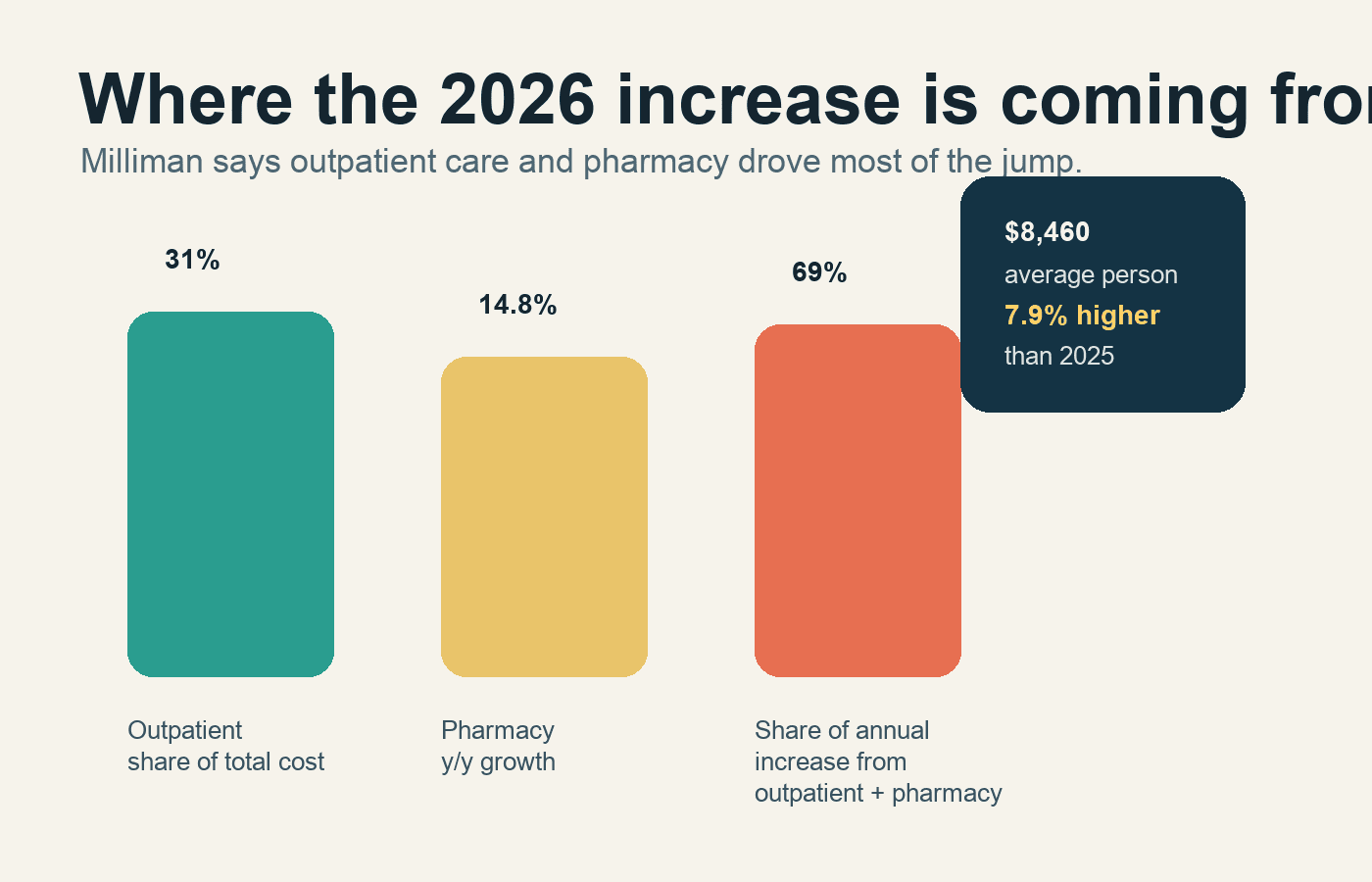

Milliman said the annual cost of healthcare for a typical American family of four covered by an employer plan reached $37,824 in 2026. For the average person, the cost reached $8,460. The average-person figure rose 7.9% from 2025, which Milliman said was the biggest increase in more than a decade if you set aside the pandemic distortions. That is a big number on its own. It matters even more because most workers do not experience it as one obvious bill.

They experience it as slower wage growth, narrower benefit choices, higher deductibles, tighter provider networks, and more anxiety about actually using the coverage they technically have.

That is the part of the health-cost story I think markets still underprice.

Investors spend a lot of time debating consumer resilience. Can households keep spending? Can employers keep hiring? Can margins hold if rates stay higher for longer? Employer health inflation cuts through all three questions at once because it acts like a quiet tax on compensation.

If a family plan is now pushing toward $38,000 in total annual cost, the issue is no longer just whether the employee’s payroll deduction went up. The issue is what the employer is not doing with that money instead. Less room for raises. Less room for bonus pools. Less room for richer benefit design. Less room for aggressive hiring in labor-intensive businesses.

That is why I read the Milliman release as finance news, not niche health-policy news.

The drivers matter. Milliman said outpatient facility care now makes up roughly 31% of employer-sponsored healthcare spending, making it the biggest single category. Pharmacy was the fastest-growing component, rising 14.8% year over year for the average person. Milliman also said outpatient care and pharmacy together accounted for 69% of the annual increase.

That should sound familiar to anyone watching public markets. Outpatient settings have become a bigger revenue engine across the healthcare system. GLP-1 drugs keep pulling more dollars into pharmacy spend. Provider consolidation keeps weakening the buyer’s leverage. The result is that employers, even very large self-insured ones, are often negotiating from a structurally weak position.

KFF’s employer survey already showed where this was heading. In 2025, the average annual premium for family coverage hit $26,993, with workers contributing $6,850 toward that total. The new Milliman number is not directly comparable because it includes the broader cost of care, not just premiums. But together they tell the same story: the visible premium pain was already high, and the invisible cost base behind it kept getting worse.

That is the hidden squeeze.

For workers, healthcare inflation does not always feel like inflation because so much of it is filtered through employers. The money disappears before it shows up in take-home pay. That makes it politically quieter than rent or groceries, but not economically smaller. In some cases it may be more important, because it directly competes with wages.

For companies, especially outside big tech, this is a harder problem than it looks. Employers can push more cost onto workers, but only up to a point before retention gets worse. They can narrow networks, but that tends to create employee blowback. They can push high-deductible designs, but that often just changes when people seek care, not the underlying system prices. They can carve out pharmacy strategies, but drug trend is still drug trend.

This is where the New England Journal of Medicine perspective from earlier in May was useful. Its argument was that self-insured employers are a sleeping giant in health-care affordability. That framing feels right to me. Big employers have scale, claims data, and purchasing power on paper. In practice, they are still fragmented buyers dealing with a healthcare system that is better at monetizing complexity than reducing it.

That gap matters for investors because it pushes this story beyond insurance stocks.

If employer health costs keep compounding this way, the effects show up in more places than UnitedHealth, CVS, Humana, or hospital operators. They show up in wage negotiations, labor cost assumptions, benefits consulting, pharmacy benefit management, and consumer discretionary demand. They also show up in the earnings quality of companies that look healthy until you notice how much of their compensation growth is being eaten by healthcare.

I think that is why this topic deserves more attention right now. The U.S. market has spent the last year obsessing over AI capex, tariffs, rates, and the consumer. Fair enough. But employer healthcare costs are one of the clearest examples of an economic pressure that is both large and easy to miss.

It is easy to miss because the burden is dispersed. No single worker sees the full employer contribution. No single quarterly report calls it out cleanly unless medical trend really blows up. No single inflation print captures the labor-market consequences. But the drag is real.

The near-term question is whether employers become more aggressive buyers or continue acting like price takers. Milliman pointed to GLP-1s, changes in how pharmacy costs flow to plan sponsors, and AI-assisted billing as important forces to watch. None of those look like one-quarter issues. They look structural.

My read is that 2026 may be the year more executives stop treating health benefits as a background HR expense and start treating them as a capital-allocation problem. If healthcare claims inflation keeps outrunning comfort, then benefits strategy becomes part of margin strategy. And if benefits strategy becomes part of margin strategy, this stops being a healthcare-side story and becomes a mainstream business story.

For U.S. readers, the practical takeaway is simple. When you hear that the labor market is holding up, or that wage growth looks decent, or that the consumer has more room than expected, it is worth asking what part of that picture is being quietly offset by employer health costs.

This week’s Milliman data suggests the answer is: more than most people think.