The AI Trade's Next Bottleneck Isn't the GPU. It's Power Delivery.

The AI trade still looks healthy if you only watch Nvidia’s top line. The company just reported $81.6 billion in quarterly revenue, with data center revenue at $75.2 billion, and added another $80 billion to its buyback authorization. That is not what a demand slowdown looks like.

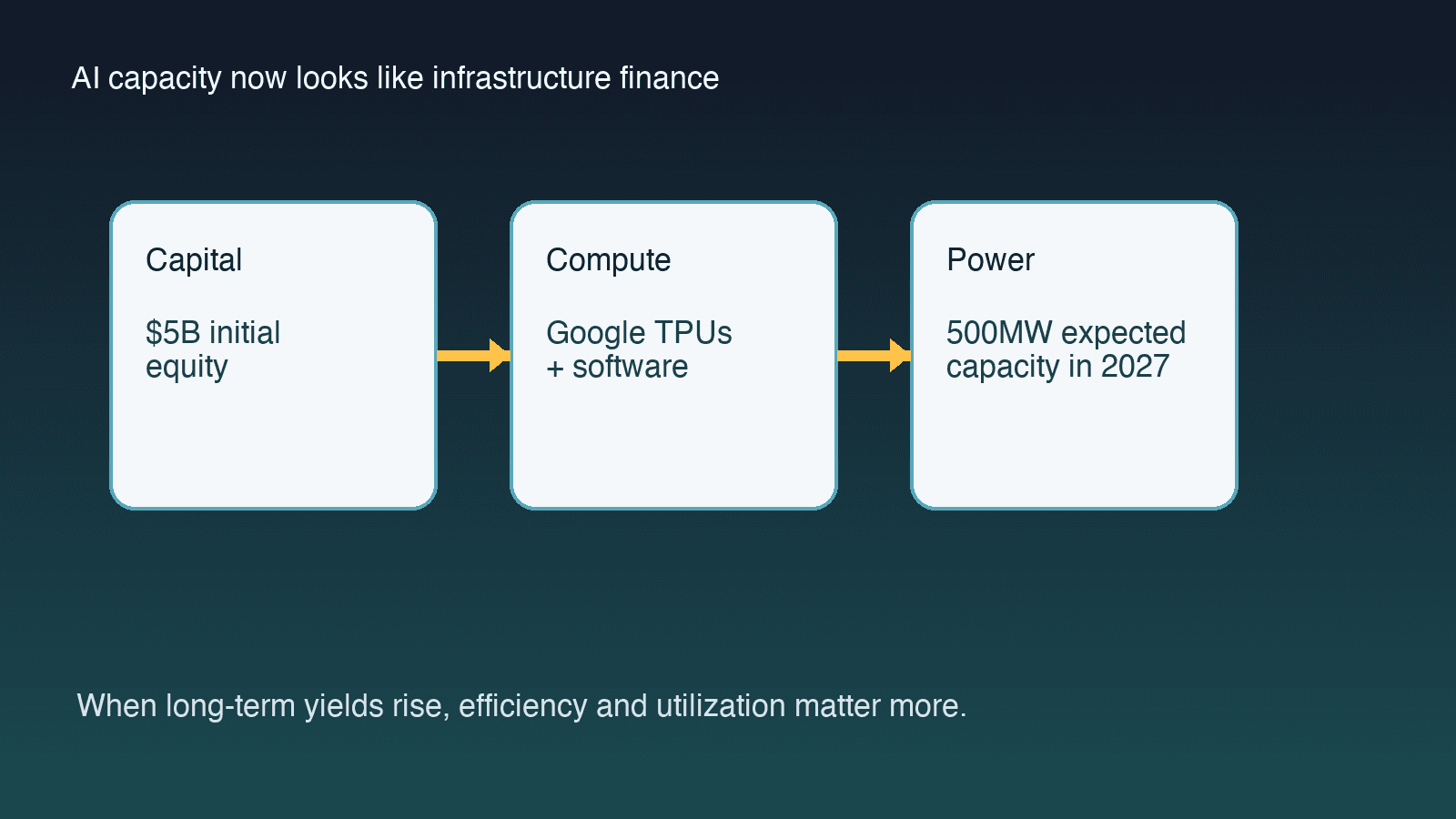

But the more interesting signal this week came from two less flashy announcements. Google said Blackstone is making an initial $5 billion equity commitment to a new TPU cloud venture that is expected to bring 500 megawatts of capacity online in 2027. A day earlier, Analog Devices agreed to buy Empower Semiconductor for $1.5 billion in cash to deepen its position in high-density power delivery for AI systems.

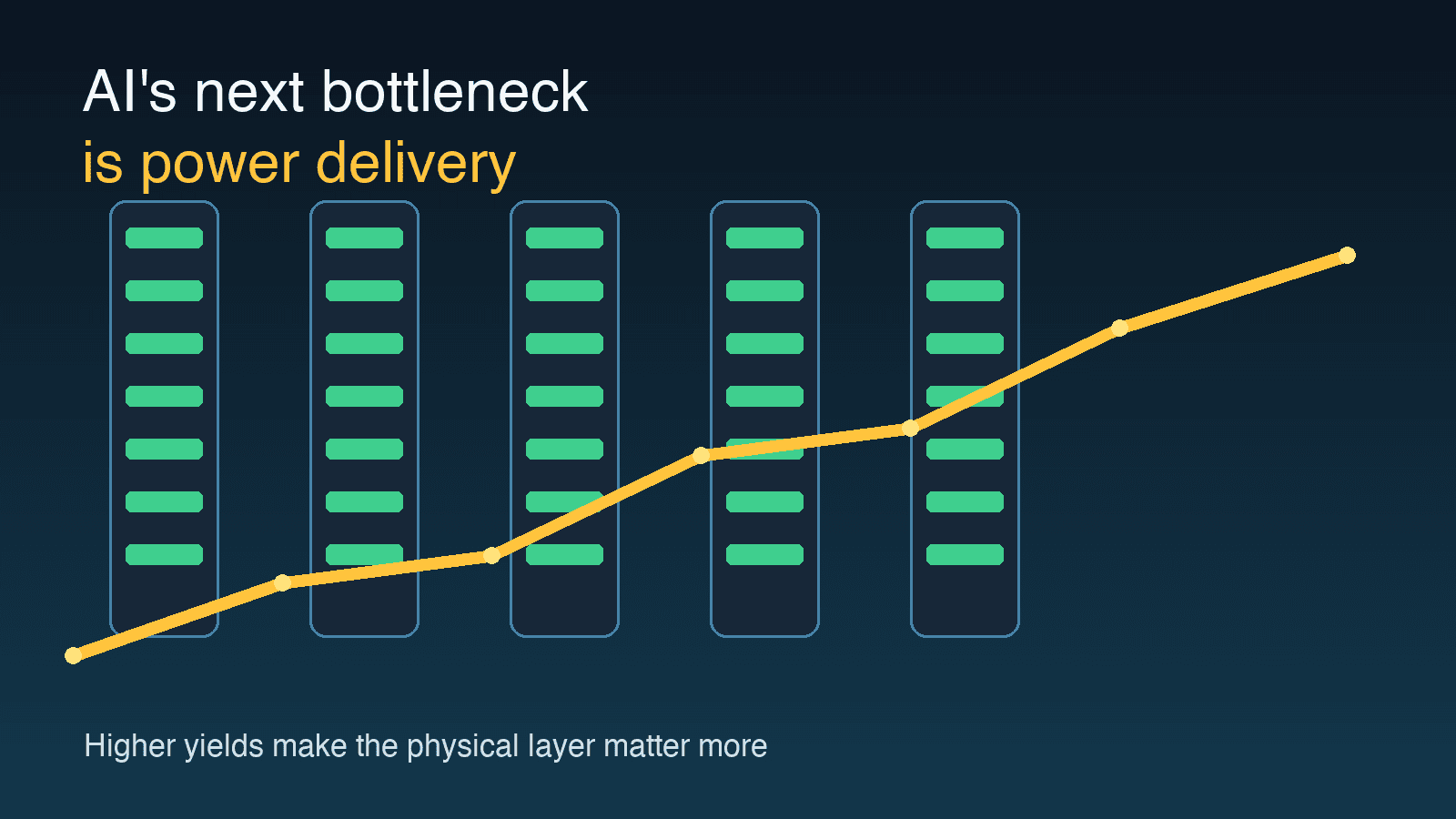

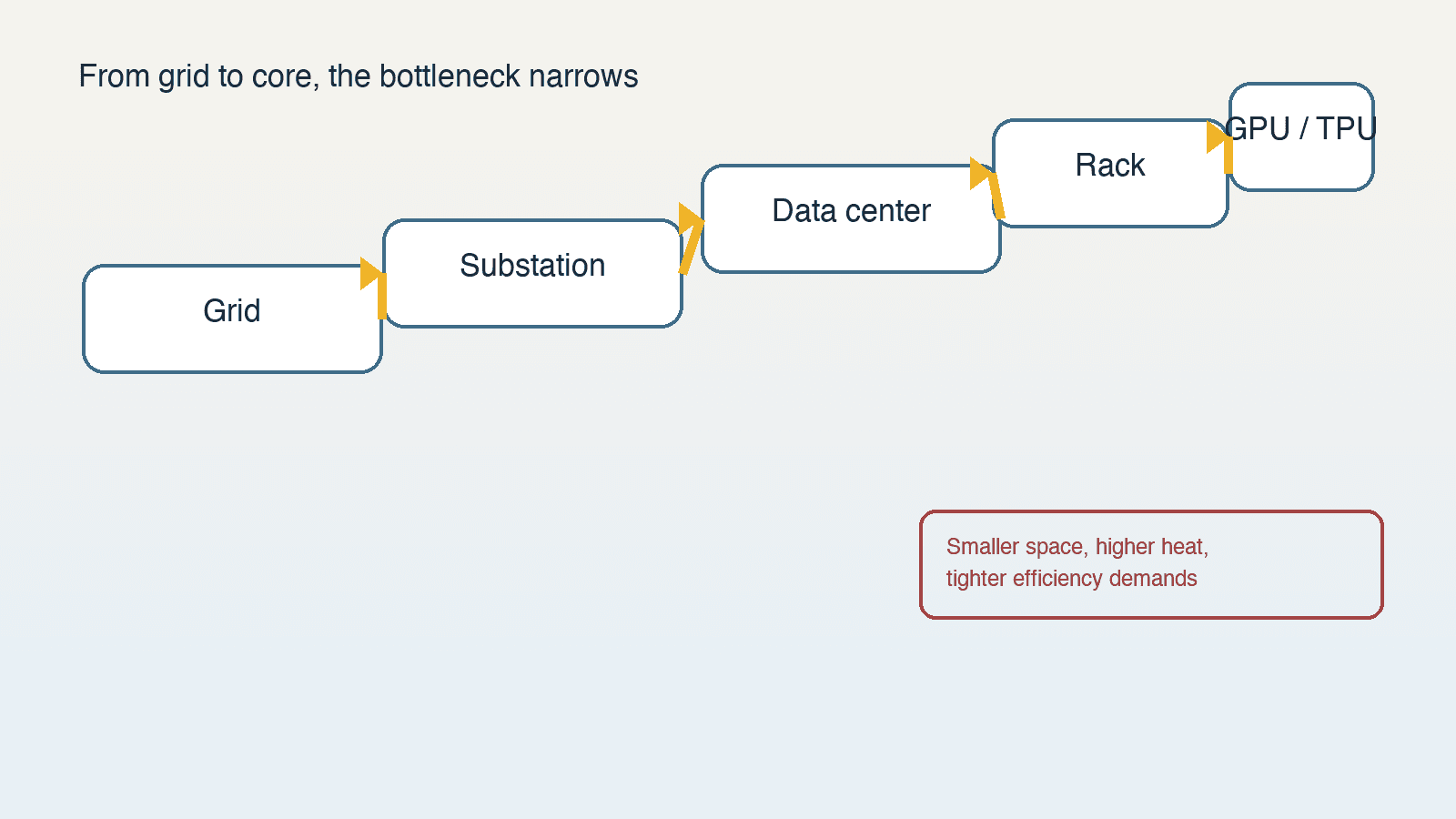

Those headlines point to the same conclusion: the next constraint on the AI buildout is no longer just access to GPUs. It is the ability to deliver power efficiently, close to the processor, at a scale that still earns an acceptable return.

That matters because the market has started to price the AI boom as a long-duration infrastructure story, not just a chip cycle. Reuters reported on May 22 that the 10-year Treasury yield hit its highest level since January 2025 this week, while the 30-year yield touched its highest level since 2007. When yields move like that, the cost of financing data centers, transmission upgrades, cooling systems and power equipment moves with them.

So investors now have two things to hold in their head at once. First, AI demand is still real. Nvidia’s numbers make that hard to dispute, and Google’s TPU cloud partnership with Blackstone says large buyers are still lining up capital for compute. Second, demand alone does not settle the return math. If power is scarce and capital gets more expensive, the winners inside AI infrastructure will not all be the same as the winners from the first GPU shortage.

Analog Devices is worth watching for exactly that reason. In announcing the Empower deal, ADI described power density and thermal limits as a critical bottleneck for AI system scale. The company is not buying another broad AI story. It is buying a specific layer of the stack: integrated voltage regulation and silicon capacitor technology that pushes power conversion closer to the processor. That is a practical bet that system architecture is shifting toward whatever reduces loss, heat and footprint inside increasingly dense compute racks.

ADI’s own results help explain why this matters now. The company reported second-quarter revenue of $3.62 billion on May 20 and guided for roughly $3.9 billion in third-quarter revenue at the midpoint. That is not Nvidia-style growth, but it does show improving demand across industrial and communications markets at the same moment hyperscalers are redesigning AI infrastructure around power efficiency. In plain English: the boring parts of the semiconductor chain are getting less boring.

Google’s side of the story matters just as much. Its Blackstone joint venture is a reminder that AI capacity is increasingly being packaged like energy or telecom infrastructure. Google will supply TPUs, software and services; Blackstone is effectively helping underwrite the physical capacity needed to bring that compute to market. That is a more capital-intensive model than the old software-era assumption that demand could be met mostly by renting generic cloud hardware.

This is where the rates backdrop becomes more than macro noise. If long-end yields stay high, the market may keep rewarding companies with immediate AI revenue while becoming more selective about everyone else in the buildout. That probably means a higher bar for speculative data center projects, more attention to utilization rates, and more value placed on hardware that lowers total power consumption rather than simply raising peak performance.

It also means the AI trade may broaden in a more complicated way than many investors expected. Yes, the obvious beneficiaries are still the companies selling the compute. But there is a second ring of beneficiaries forming around power management, electrical equipment, cooling, grid services and financing structures that can absorb multi-year build cycles. If you believe AI spending remains durable, those may be the places where the next round of upside is less crowded.

The simple version is this: the AI boom is maturing from a chip story into a systems story. Systems require land, power, thermal design, financing and patience. Nvidia’s latest quarter shows the demand side is intact. Google and Blackstone show the capital side is adapting. ADI’s Empower deal shows the engineering bottleneck is moving closer to the socket.

That does not kill the AI trade. It makes it more real. And once a trade becomes more real, it usually becomes less about the headline winner and more about the hidden constraints that everyone underestimated at the start.