AI's Next Bottleneck Is Power Delivery

The most interesting development in the AI trade this week is not another chatbot launch or another giant GPU order. It is the growing evidence that power delivery itself is becoming a real bottleneck, and that changes how investors should think about where AI money goes next.

On May 19, Analog Devices said it would acquire Empower Semiconductor for about $1.5 billion in cash. That is not a headline most generalist investors would normally stop for. But the logic behind it is worth stopping for. Analog Devices framed the deal around a specific constraint in AI systems: not just how many watts a data center can draw, but how efficiently power can be delivered closer to the processor as compute density keeps rising. Empower builds integrated voltage regulation technology meant to shorten that path and improve efficiency at the point where the chip actually needs power.

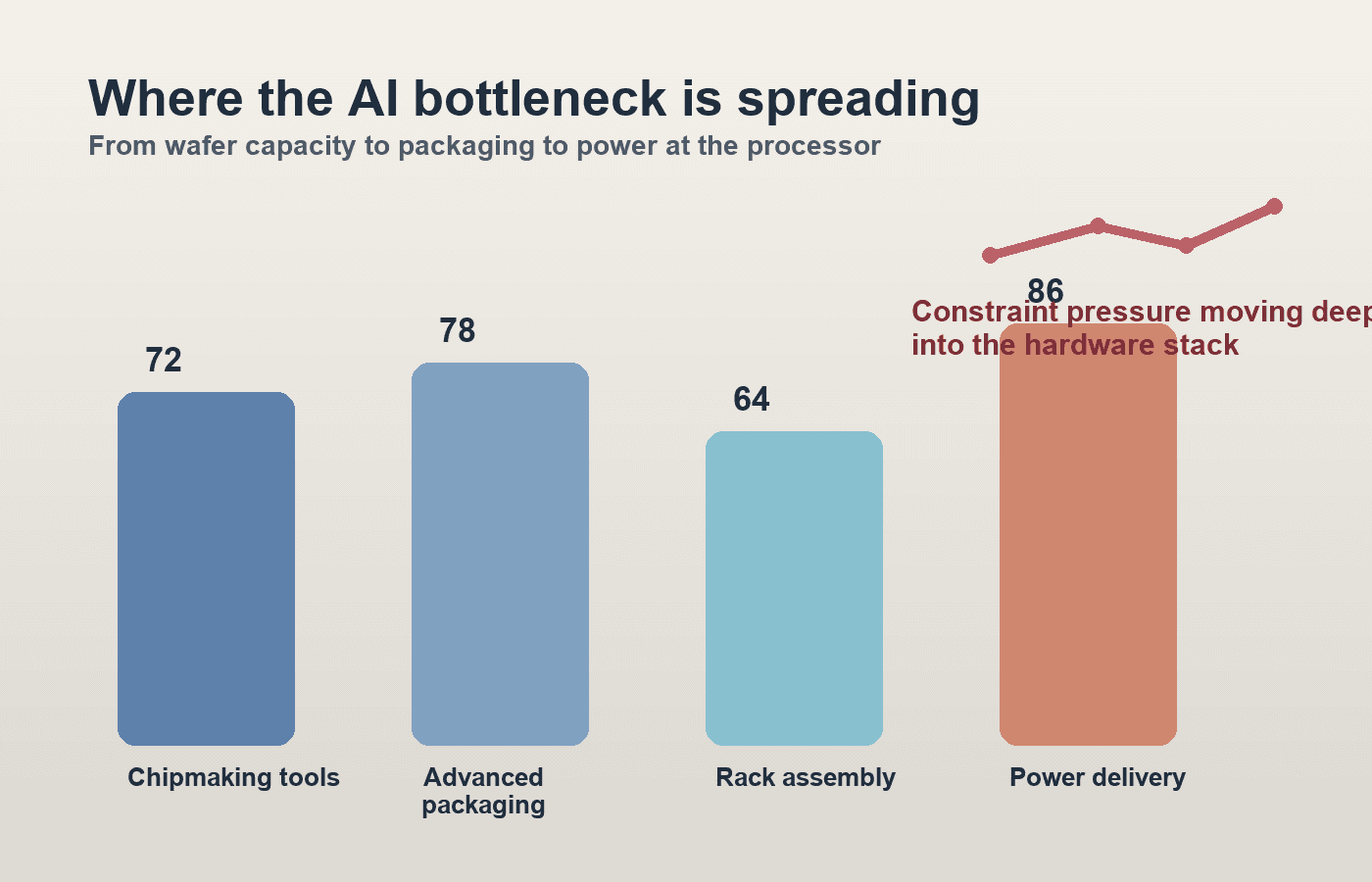

This is a meaningful shift in the AI narrative. For the last two years, the market has mostly treated AI infrastructure as a race for the biggest visible pieces: GPUs, high-bandwidth memory, cloud leases, and data-center capacity. Those still matter. But once every major platform is trying to pack more performance into each rack, the bottlenecks migrate. They move into advanced packaging, interconnects, cooling, and power conversion. In other words, the next dollars do not only go to headline chip designers. They also go to the companies that make dense computing physically workable.

That broader point showed up again on May 20, when ASML CEO Christophe Fouquet told Reuters that the global semiconductor market would remain tight for the foreseeable future, with demand from AI, satellites, and robots outrunning what the industry can produce. He said the market would likely face sporadic bottlenecks across the supply chain. The point is not just that demand is strong. It is that the constraint set is widening. If the front end of chip manufacturing is stretched, and the back end of packaging and power delivery is also tightening, then the economics of AI infrastructure stop looking like a one-company story.

AMD's moves this week reinforce that reading. On May 21, the company announced more than $10 billion of investment across Taiwan's ecosystem to expand strategic partnerships and scale advanced packaging manufacturing for next-generation AI infrastructure. On May 22 in Taipei, CEO Lisa Su said AMD was asking partners to ramp up production because AI demand had been stronger than expected, and said the CPU market was tight. That matters because AMD is not talking only about accelerator demand anymore. It is talking about a system-level buildout that includes CPUs, packaging, substrates, manufacturing, and rack-scale assembly.

The market already had clues this was coming. In AMD's May 5 first-quarter results, data-center revenue reached $5.8 billion, up 57% from a year earlier, and the company said second-quarter revenue should be about $11.2 billion at the midpoint. Analog Devices reported record fiscal second-quarter revenue of $3.62 billion on May 20 and said it saw record bookings across its industrial, automotive, and communications B2B markets. Those are not isolated data points. They suggest the AI buildout is feeding demand through multiple layers of the hardware stack, including companies that sit well below the glamorous software narrative.

There is an investing lesson here. When a technology boom matures, the best opportunities often move one layer down, into the chokepoints. Railroads mattered during industrial expansion. Power equipment mattered during electrification. In the AI cycle, some of the next chokepoints look increasingly physical and unglamorous: power-management chips, advanced packaging capacity, networking gear, thermal systems, and the manufacturers that can actually assemble high-density compute at scale.

That does not mean the GPU leaders stop winning. It means the market has to get more precise. If AI demand stays this strong, the question is no longer just who designs the fastest chip. The question is who can help customers turn expensive silicon into deployed, reliable, energy-efficient systems. That is a different question, and it opens room for a broader set of beneficiaries.

It also introduces a layer of risk that equity narratives sometimes skip past. As systems become more power-dense, the chance of delays, cost overruns, or margin compression rises in the supporting layers of the stack. If advanced packaging remains constrained, some compute deployments get pushed out. If power conversion and cooling do not scale smoothly, total cost of ownership goes up. If every major AI buyer is trying to secure the same supply chain at once, pricing power spreads beyond the obvious names. Investors chasing AI purely through the biggest brands may miss that the value pool is widening and getting more operationally complex.

For U.S. readers, the practical takeaway is straightforward. The AI trade is no longer only about model leaders and GPU shipments. It is becoming a story about whether the entire hardware chain can carry more compute, more efficiently, and on time. This week's Analog Devices deal looks small beside the trillion-dollar market caps elsewhere in semis. But strategically it says something important: the next bottleneck may be less about inventing more intelligence and more about delivering enough clean, dense power to let existing intelligence run.

That is the kind of change markets often notice late. By the time a bottleneck becomes obvious in quarterly numbers, the enabling suppliers are usually no longer cheap. This week was a reminder that the AI buildout is moving deeper into the plumbing. Investors should follow it there.