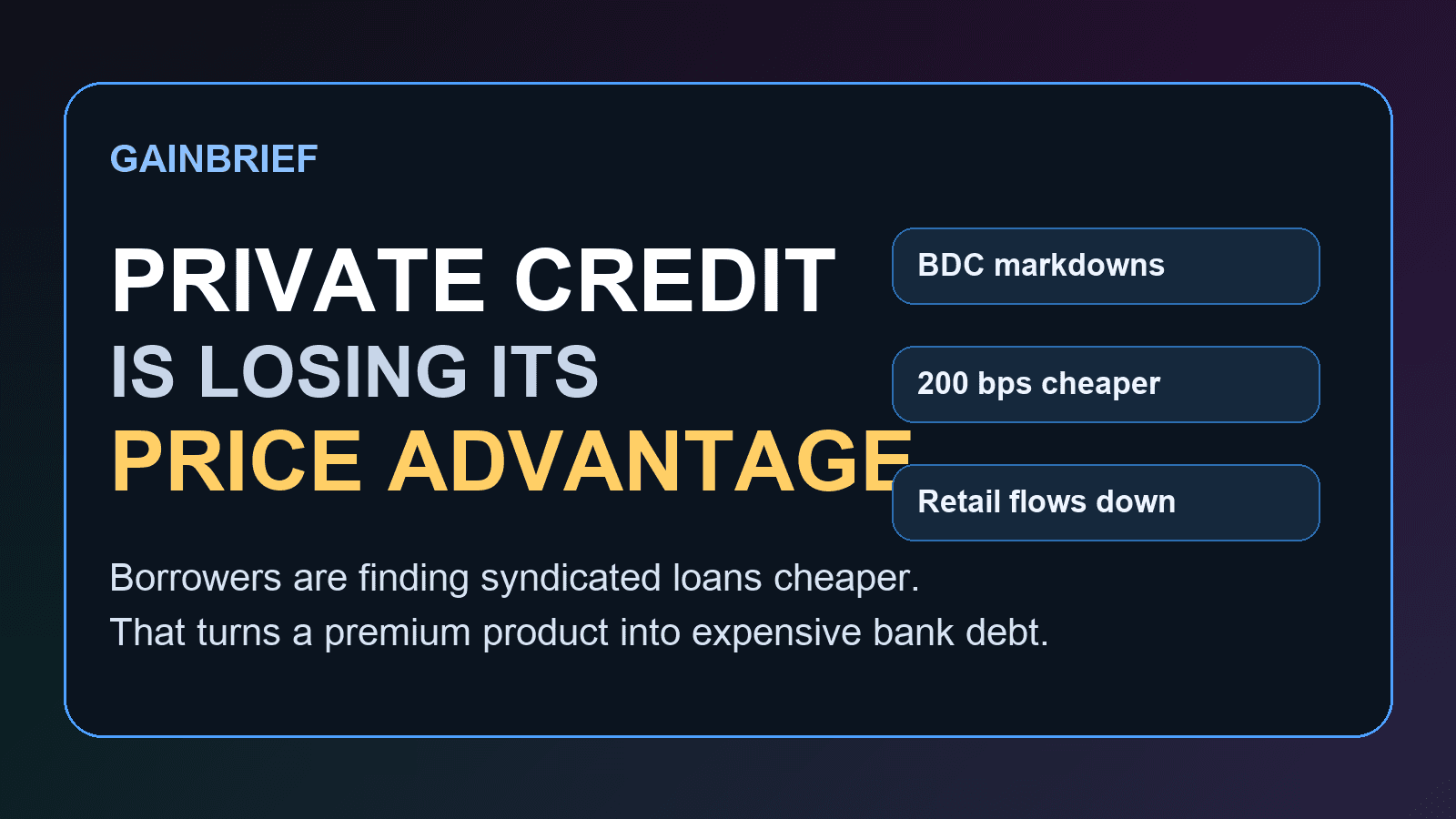

Private Credit Is Losing Its Price Advantage

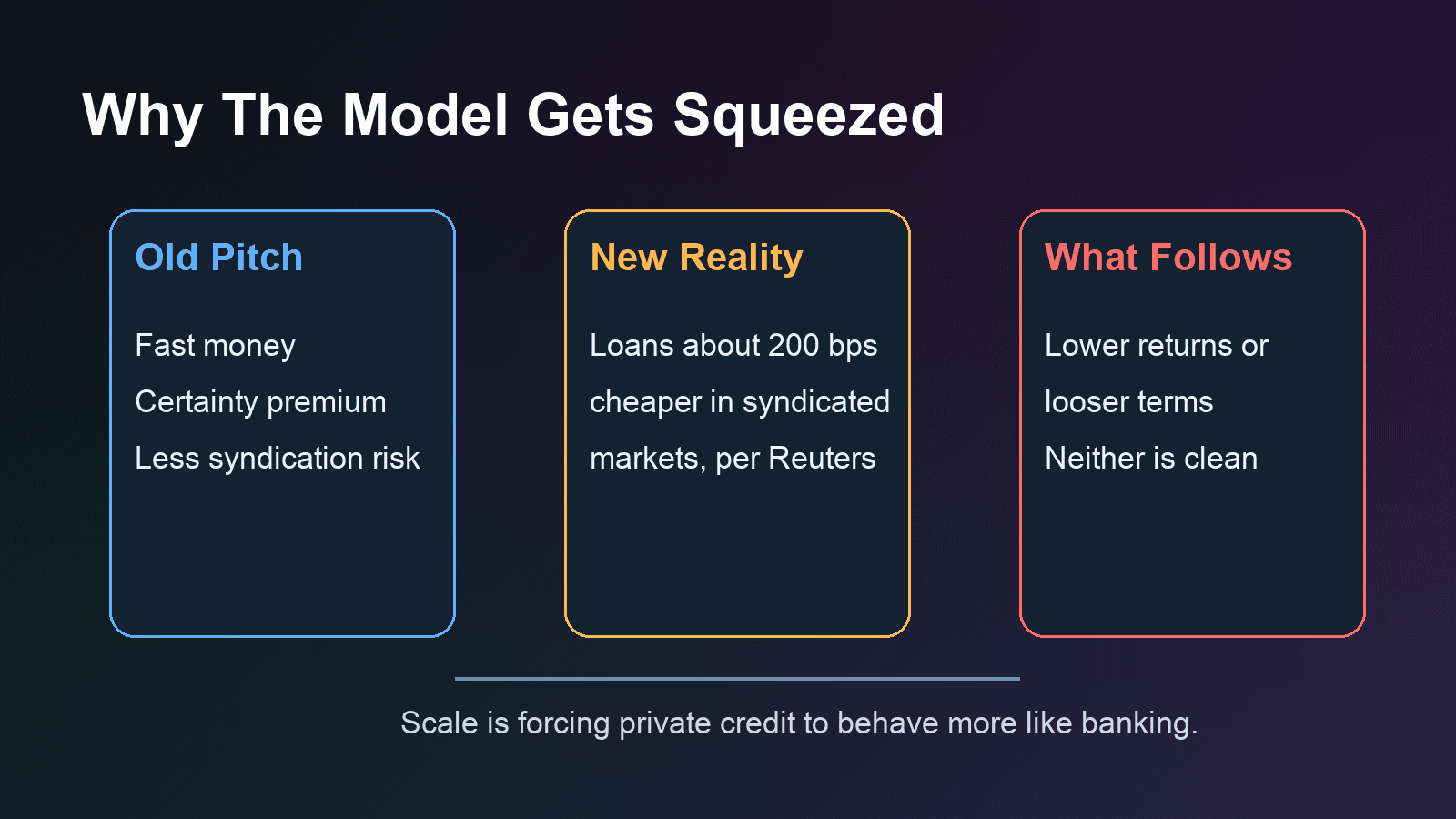

Private credit has spent years marketing itself as a better version of bank lending: faster decisions, tighter execution, fewer syndication headaches, and more certainty for private equity sponsors. That story worked when money was cheap and borrowers were willing to pay up for speed.

This month, the more important signal is that the price advantage has started to run in reverse. Reuters reported on May 4 that some U.S. borrowers are moving back toward bank-led syndicated loans because risky loans there are about 200 basis points cheaper than direct lending. Around the same time, Reuters reported that private credit funds have begun marking down their loan books, while fundraising from wealthy individuals into non-traded BDCs fell 45% in the first quarter from a year earlier.

What casual readers are missing is that this is not just a stress story. It is a business-model story. Private credit was supposed to win by offering certainty at a premium. Once that premium gets too high, and once investors start questioning marks, the product stops looking like a superior form of lending and starts looking like expensive bank debt with less liquidity.

The Federal Reserve's May 2026 Financial Stability Report shows how big this has become. Private credit loans account for about $1.4 trillion, or roughly 10% of U.S. nonfinancial corporate debt and about one-third of below-investment-grade debt excluding bank loans. That scale matters because the sector is no longer a niche workaround for a handful of mid-market deals. It has become a real source of financing power.

But scale changes the rules. As markets mature, borrowers become less impressed by branding and more sensitive to price. Reuters' May 15 review of 14 major BDCs found aggregate fair value falling to 98.55% of cost at the end of March, leaving portfolios marked about $1.2 billion below amortized cost. Another Reuters report, citing MSCI data, said more than a tenth of private-credit loans had been marked down by at least 50%. Those numbers do not mean the entire sector is in trouble. They do mean private lenders are losing the luxury of being judged mainly on narrative.

That is why the real threat is not a sudden collapse. It is compression. If banks can syndicate leveraged loans more cheaply, private lenders either accept lower returns or loosen terms to defend volume. Neither option is attractive. Lower returns hurt fundraising. Looser terms hurt future credit quality. Reuters also reported that first-quarter outflows from semi-liquid private credit vehicles slightly exceeded new inflows, the first time that has happened since those vehicles were created, according to the Fed's summary of the market.

There is a second-order effect for Wall Street. The winners from here may be less the firms that raised the most private credit and more the ones that can arbitrage between public and private markets. If syndicated desks regain pricing power while private funds face redemption pressure and valuation scrutiny, the advantage shifts back toward institutions that can warehouse risk, distribute paper, and choose the cheaper channel. In other words, the more private credit becomes mainstream, the more it starts to recreate the banking logic it claimed to escape.

That does not kill the asset class. Borrowers will still pay for speed, flexibility, and bespoke structures. Sponsors will still want certainty in volatile markets. But the easy era, when private credit could charge up for convenience and still be treated as a smoother, safer product than public credit, looks harder to defend.

The market is finally asking a basic question it should have asked sooner: if private credit is more expensive for borrowers and less liquid for investors, how long can managers keep selling the idea that the premium is proof of quality instead of proof of strain?