AI Infrastructure Is Becoming a Yield Product

The market still talks about the AI boom as if it were mainly a technology race between chipmakers and cloud platforms. The money is starting to say something else.

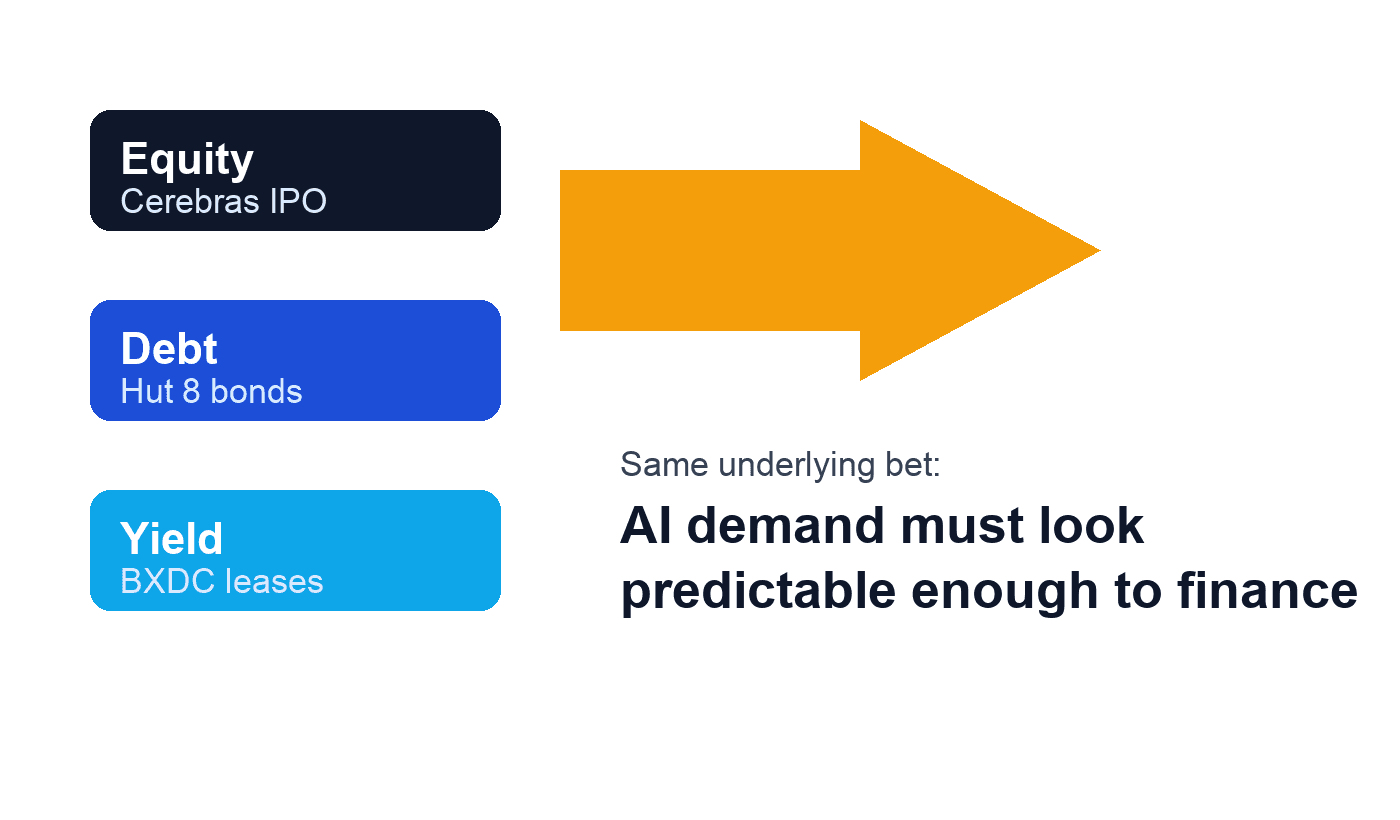

Over the last two weeks, the financing around AI infrastructure has become its own story. Cerebras said on May 15 that it closed a $6.38 billion initial public offering. Two days earlier, Blackstone Digital Infrastructure Trust priced an IPO of 87.5 million shares at $20 apiece, with proceeds targeted at stabilized data centers leased to investment-grade hyperscale tenants. And Hut 8 said on May 6 that it raised $3.25 billion of investment-grade senior secured notes to finance its River Bend AI data center project at roughly 95% loan-to-cost.

That is the shift casual readers are missing. AI is no longer just being valued like a growth theme. It is being packaged like an income product. Once Wall Street starts underwriting data centers, inference companies, and power-linked contracts as assets that can carry IPO equity, long-dated bonds, and rent-like cash-flow assumptions, the AI trade stops being only about who has the best model or fastest chip. It becomes about who can manufacture durable cash flows that financiers trust.

This matters because finance changes behavior. Venture money can tolerate ambiguity. Public equity can tolerate stories for a while. Project debt cannot. If more of the AI buildout gets funded through structures that depend on predictable utilization, credit metrics, and long-term counterparties, then the winning business models become narrower than the current AI hype suggests.

Blackstone’s pitch makes that explicit. The company says BXDC is aimed at newly constructed, income-generating, stabilized data center properties leased to investment-grade hyperscale tenants on long-term contracts. That is not a venture-style bet on optionality. It is a real-estate and yield thesis wrapped around AI demand. The asset only works if the tenant quality is elite, the contract term is long, and the cash flows look boring enough to underwrite.

Hut 8 tells the same story from the debt side. The company called its $3.25 billion note deal the first single-sponsor data center project to reach the investment-grade construction bond market, and said it did so on a non-dilutive, non-recourse basis. In plain English, AI infrastructure is being financed less like speculative capacity and more like a power plant, toll road, or aircraft lease. That lowers the equity burden, but it also raises the penalty for getting demand wrong.

Cerebras adds the public-market version of the same shift. Its IPO is a reminder that investors are now being asked to fund not just the established winners selling chips into the AI boom, but newer infrastructure names trying to become permanent fixtures in the stack. That broadens the investable surface area. It also means more of the boom gets judged by capital-markets discipline rather than pure technological excitement.

This is why Bloomberg’s May 19 report on rising AI data-center borrowing deserves more attention than another debate about whether AI spending is too high. Citing a Bank of America survey, Bloomberg reported that 34% of global fund managers saw AI hyperscaler capital spending as the most likely source of a future systemic credit event, double the share from April. The warning is not that AI demand disappears tomorrow. It is that once the buildout gets deeply financed, mistakes do not stay inside equity valuations. They move into credit, collateral, refinancing, and tenant concentration.

The optimistic version of this trend is clear. More financing vehicles can accelerate supply, bring in non-tech investors, and make AI infrastructure look more like a mature asset class. The harder version is that Wall Street may end up rewarding the most financeable AI businesses, not necessarily the most imaginative ones. If your customers are weak, your usage is volatile, or your economics depend on heroic assumptions about future pricing, the market may stop calling that innovation and start calling it bad collateral.

That is why the next phase of the AI trade may feel less like software and more like infrastructure finance. The important question is no longer just who can build the smartest model. It is who can turn AI demand into cash flows sturdy enough for bankers, bond buyers, and yield-hungry investors to treat as almost utility-like. When that happens, the boom gets bigger, but it also gets more fragile in a very different way.