The Housing Market Is Becoming Builder-Financed

The U.S. housing market is starting to look less like a normal resale market and more like a builder-financed market. That distinction matters. Mortgage rates just climbed to 6.51%, the highest level in nearly nine months, yet pending existing-home sales still rose 1.4% in April from March and 3.2% from a year earlier. At the same time, the Mortgage Bankers Association said applications for mortgages to buy new homes fell 2.4% year over year in April.

Those numbers look contradictory only if you assume housing is competing on price alone. It is not. The real product now is financing, and large builders are better positioned than ordinary sellers to manufacture it.

That is the part casual readers tend to miss. High rates are not freezing every corner of housing equally. They are shifting power toward companies that can use incentives, captive mortgage arms, and balance-sheet flexibility to turn an unaffordable monthly payment into a barely acceptable one. The market is not clearing through lower prices. It is clearing through engineered affordability.

D.R. Horton said in April that affordability constraints and cautious consumer sentiment still weighed on new-home demand, but it also said it expects sales incentives to remain elevated through fiscal 2026. That is more important than it sounds. Horton is not just selling houses. It also provides mortgage financing, title services, and insurance, and its financial-services segment generated $192.8 million in quarterly revenue with a 26.8% pre-tax margin. In other words, one of the country’s biggest builders is not merely reacting to tough financing conditions. It is monetizing them.

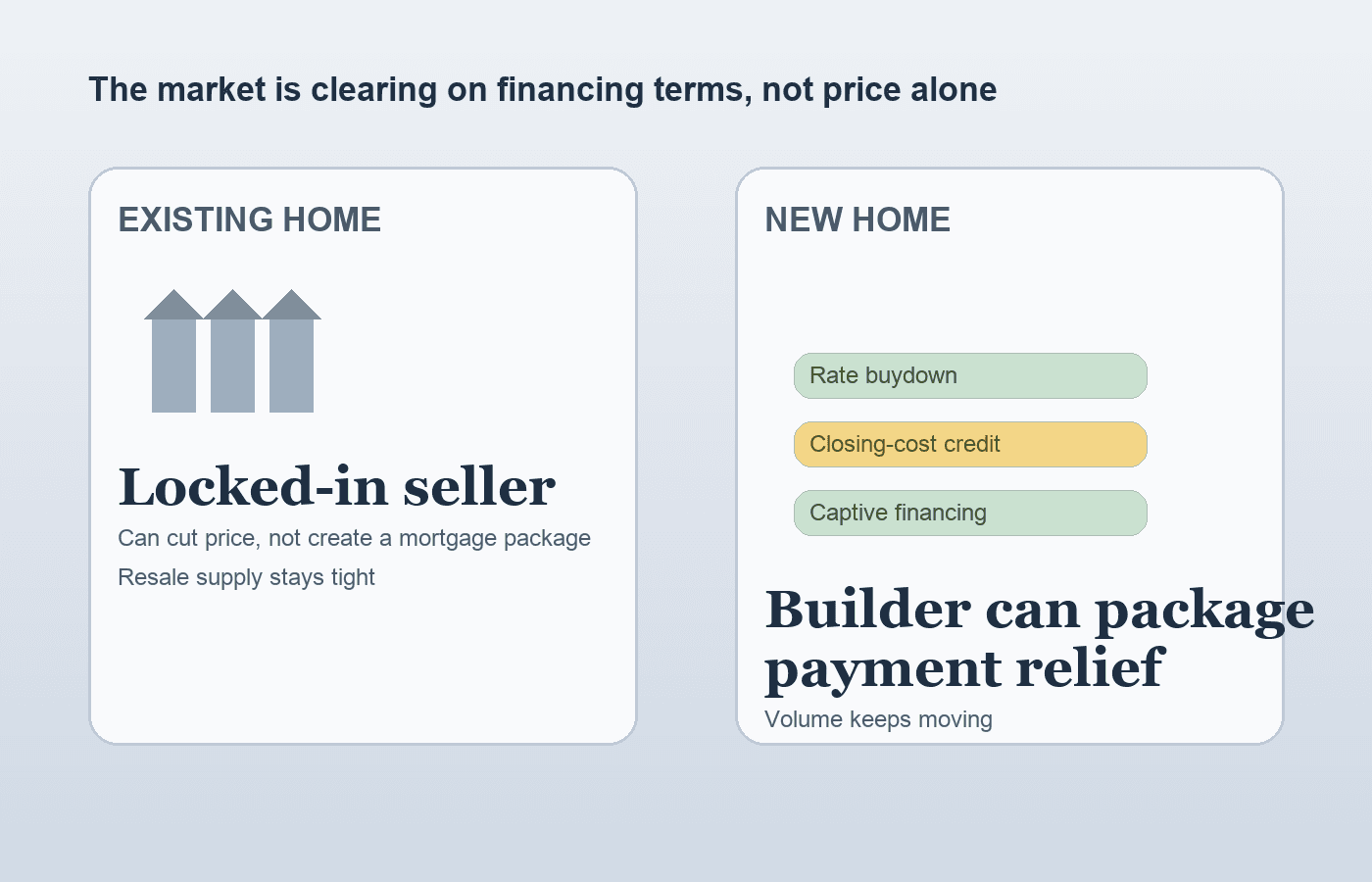

That helps explain why housing data can feel strangely resilient even when buyers still say homes are unaffordable. Existing homeowners are trapped by the so-called lock-in effect: many have mortgages far below current rates and do not want to give them up, which keeps resale supply structurally tight. Builders face the opposite problem. They need to move inventory, preserve volume, and keep land pipelines active. So instead of waiting for the Federal Reserve or the bond market to rescue affordability, they offer rate buydowns, closing-cost help, and financing packages that individual sellers cannot match.

The result is a market that is increasingly bifurcated. New homes can stay in motion because large builders are effectively subsidizing the transaction. Existing homes remain stickier because the owner of a single house cannot replicate that financing package without simply cutting price. For buyers, that means the sticker price is no longer the whole negotiation. The monthly payment structure matters more than the headline value of the home.

For investors, that makes housing data easier to misread. A small improvement in sales activity does not necessarily mean affordability is improving in a broad, durable way. It can simply mean builders are spending more aggressively to keep units moving. That supports volume and market share, but it also means the industry is absorbing part of the rate shock internally through incentives and financing support instead of waiting for the Fed to deliver relief.

There is also a business consequence beyond housing itself. If builders increasingly control the financing lever, they gain share not just from resale listings but from parts of the mortgage and brokerage ecosystem that used to sit outside the homebuilder profit pool. The more the housing market depends on engineered affordability, the more value shifts toward companies that can bundle land, construction, lending, title, and incentives into one offer.

That is why the housing story now matters as a market-structure story, not just a macro story. Rising rates are supposed to cool housing demand. Instead, they are reorganizing who gets to serve that demand. The winners are not necessarily the sellers with the best homes. They are the operators with the best financing machine.