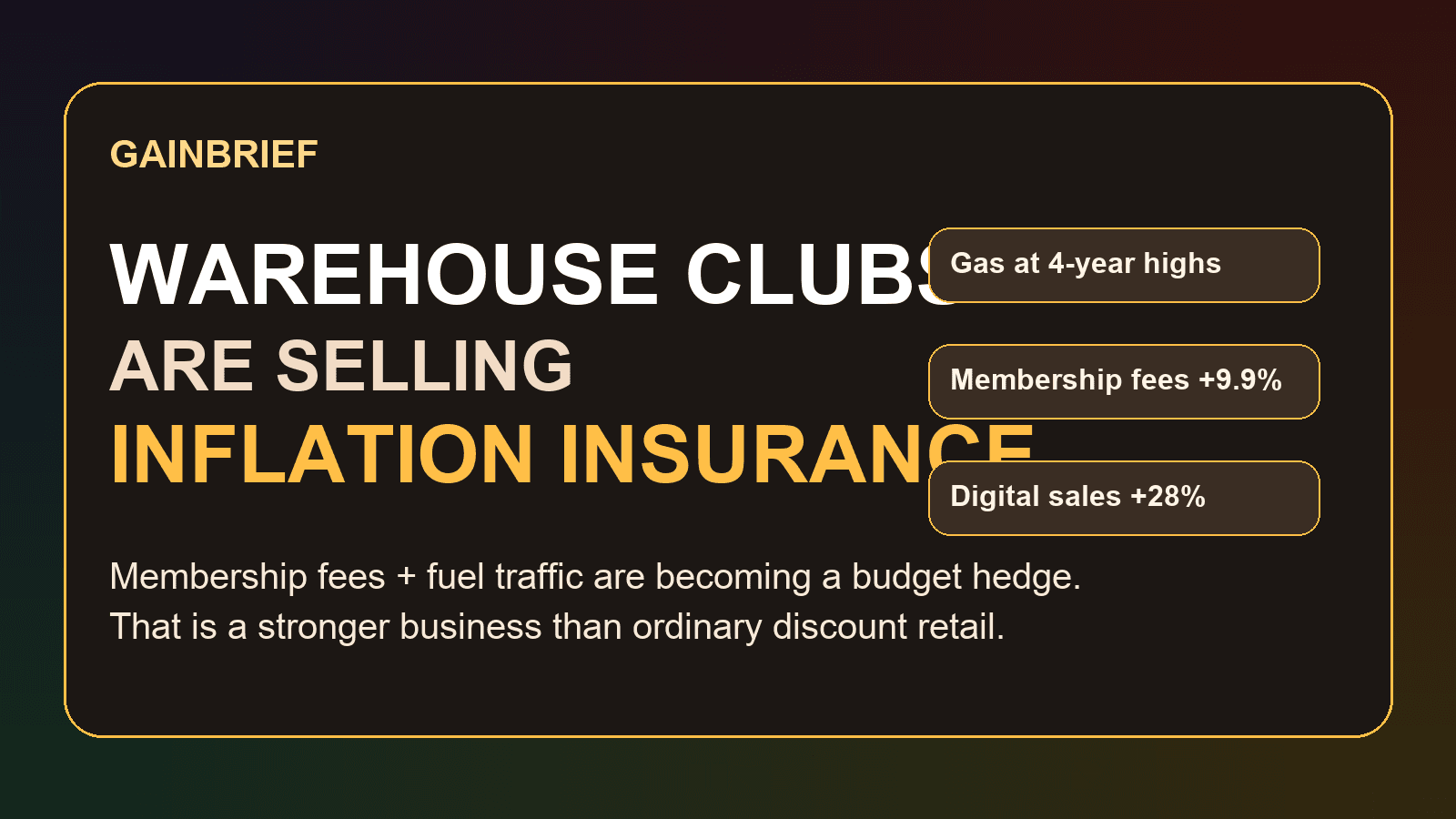

Warehouse Clubs Are Selling Inflation Insurance

BJ's Wholesale Club reported a strong quarter on Thursday, but the most interesting number was not the 6.3% comparable-sales gain. It was the shape of that growth. Excluding gasoline, comparable sales rose just 1.5%. Membership-fee income, meanwhile, jumped 9.9% to $132.4 million, and digitally enabled comparable sales climbed 28%.

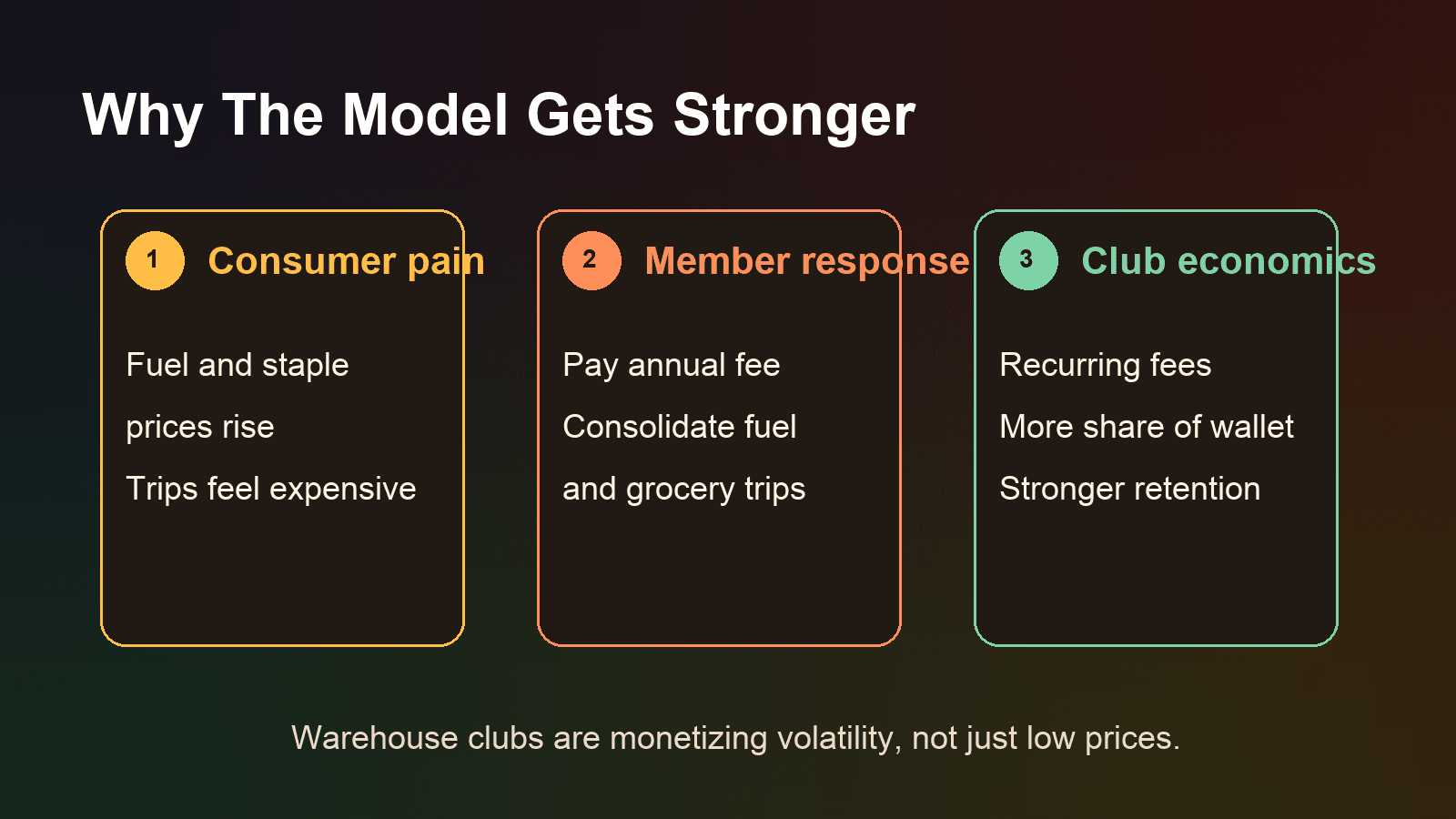

That combination matters because it suggests warehouse clubs are no longer just winning on cheap groceries. They are winning on a more powerful promise: helping households manage volatility in the two parts of the budget that feel least optional, food and fuel.

That is the part casual readers may be missing. Warehouse clubs are quietly becoming a form of inflation insurance. Consumers pay an upfront membership fee, then use that access to defend themselves against repeated hits at the pump and in staple categories. When gas prices spike and budgets get tighter, the model can actually become more attractive, not less.

The timing helps explain why. AAA said Memorial Day weekend gas prices were the highest in four years, with the national average for regular above $4.50 a gallon. Foot-traffic data summarized by NACS from Placer.ai showed visits to BJ's Gas, Costco Gas and Sam's Club Fuel accelerated earlier this spring as fuel prices climbed. In other words, the pain point that hurts much of retail can become a traffic engine for warehouse clubs.

BJ's quarter fits that pattern almost perfectly. The company added six gas stations, kept investing in price, and still grew gross profit to more than $1 billion. Merchandise margin slipped slightly, which is what you would expect when a retailer leans into value in a stressed environment. But the membership stream is what gives the model room to keep doing that. If fee income rises while members consolidate more trips around fuel and essentials, the retailer is not just selling goods. It is monetizing household habit.

That makes warehouse clubs structurally different from ordinary retailers trying to chase the same value-conscious customer. A traditional chain has to win the basket one transaction at a time. A club retailer gets paid before the basket even starts. Once a household has already paid to belong, the incentive shifts toward sending more spending through that ecosystem to justify the fee. Add gasoline, curbside pickup, delivery, and higher-tier memberships, and the relationship starts looking less like bargain hunting and more like a prepaid budget strategy.

This is why the warehouse-club story should probably trade less like a routine consumer-discretionary narrative and more like a subscription model attached to necessities. The real moat is not simply lower prices on bulk items. It is the ability to turn economic anxiety into retention. Households may cut apparel, furniture, or impulse purchases. They are much less likely to experiment with the place that helps lower a weekly grocery bill and a refill at the pump.

There is also a second-order effect on digital. When management says digital sales are growing quickly, that should not be read as a generic e-commerce win. It means clubs are making the membership more useful across more moments: stock-up trips, fill-in orders, same-day needs, and gas-linked visits. Digital is not replacing the club model. It is thickening it.

That does not mean the business is recession-proof. Fuel margins can swing, grocery competition stays brutal, and consumers can eventually balk at fee increases. But the broader lesson from BJ's is that inflation pressure is reshaping retail winners. In a high-cost economy, the strongest consumer model may be the one that feels least like shopping and most like protection.

Warehouse clubs are selling that protection in plain sight. Investors who keep reading them as simple low-price merchants may be underestimating why the model keeps compounding.