I write about markets, business, investing, and the small signals behind big financial moves.

Why Equities Stay Expensive Without a Diplomatic Win: A Risk-Adjusted Playbook for the June Data Week

TL;DR: In June’s market environment, unresolved geopolitical headlines can stay in the news without forcing an immediate equity repricing when earnings quality, liquidity, and policy expectations remain supportive. The critical constraint is not one big diplomatic event, but the next cluster of economic releases and how confidently executives can forecast cash flow across that sequence. For finance teams and investors, the edge is operational: classify risk into signal, noise, and timing, then convert each bucket into execution rules on sizing, liquidity buffers, and review intervals. That discipline protects capital whether markets continue climbing or suddenly reprice on data shocks. Why record levels can coexist with unresolved Iran risk The first headline in your source set is not a contradiction of history; it is a recurring market pattern. Equities can stay elevated without an Iran resolution when macro investors believe core earnings and discount-rate variables are stable enough in the near term. This does not mean geopolitics is ignored. It means markets are currently assigning lower near-term probability to a severe global spillover and higher probability to a contained pathway. One practical implication: if price action stays constructive, it is often because portfolios are anchored to balance sheets and rate-path expectations, not headlines themselves. You can think of it as two clocks running together: headline clock: geopolitical headlines, policy rhetoric, and negotiation optics; pricing clock: inflation prints, payrolls, guidance revisions, and corporate cash-flow sensitivity. When the pricing clock dominates, prices can ignore headline volatility, especially if positioning is already discounted. At the operational level, the J.P. Morgan piece, the headline question is more about why valuations can rema

Why Equities Hold Their Highs: The Data-First Setup Behind “No Iran Resolution” Volatility

TL;DR: Weekly market behavior is being decided by the next domestic data windows more than by a single geopolitical headline. Records in equities can coexist with unresolved diplomacy because investors are still calibrating inflation, growth, and central-bank expectations through concrete indicators, not diplomatic headlines. The practical edge is to run a conditional framework: map each key data scenario to position size and hedges, then act only when triggers appear. In that model, uncertainty from the Iran story is managed as a volatility input, not the master narrative. Why the headline paradox is not really a paradox The pair of themes is clear: traders are watching a week of economic releases while noting that stocks hold up even without an Iran resolution. The contradiction dissolves once you separate narrative weight from pricing weight. A missing agreement is painful in politics and sentiment, but in markets, what moves positioning is the probability-adjusted path of earnings, margins, rates, and liquidity. So the market can remain structurally resilient while still reacting sharply to specific negative shocks. Price can be stable while anxiety rises “No peace” headlines often create a headline risk premium, but that premium is frequently temporary unless it changes expected cash flow or financing conditions. As long as earnings pipelines stay intact and the risk-free curve remains understandable, equity exposure can stay constructive. In plain English: geopolitics sets the mood; data sets the trend. This week’s macro calendar beats diplomacy as a trading variable The financial calendar acts as a de facto switchboard. One soft jobs print can reprice rate expectations faster than a month of diplomatic updates; one stronger inflation read can force a repricing of discount rates regardless of the conflict narrative. That is why the market-watch framing in the provided headlines effectively points to one discipline: scan the calendar, then react to probabilities. What to watch in the upcomin

Why Markets Ignore a Frozen Iran Timeline: Valuation Discipline, Liquidity, and the June Data Gate

TL;DR: Stock indexes can remain near record levels despite unresolved Iran diplomacy when investors believe earnings resilience and policy predictability currently outweigh headline risk. This week’s tests are less about headlines and more about the U.S. data calendar, where inflation, labor, and earnings quality can quickly confirm or destroy the current risk-on discount. In short: geopolitics still matters, but right now it is a secondary discount factor, while macro and cash-flow realism is setting the valuation floor. Why geopolitical deadlock does not automatically cap upside Markets are not predicting peace; they are pricing probabilities. The headline that stocks are at record levels even without an Iran resolution is itself a signal: participants are betting that supply shocks, demand management, and corporate cash generation are manageable in the near term. In practical terms, this is a “known-unknown” setup. Iran headlines are uncertain and headline-friendly, but earnings season, labor costs, and refinancing conditions are periodic and measurable. Traders prefer uncertainty that can be refreshed each quarter or week over narrative risk that drifts with every diplomatic cycle. The market is trading a conditional thesis, not a declaration A conditional thesis has a trigger set. If the economic data supports a controlled-growth environment and liquidity conditions hold, prices can stay elevated even while politicians argue. If data breaks to a stronger inflation or weaker jobs scenario, the same market can reprice instantly. The key is that this process is incremental: a lot of risk gets pre-priced, but repricing only accelerates when a hard signal arrives. What is keeping the floor in place right now The second ingredient in the paradox is positioning. In periods where cash and liquidity are stable, risk assets can decouple from episodic geopolitical stress. For finance and business readers, this matters because portfolio behavior becomes more about balance-sheet sensitivity than political he

Volatility by Other Means: Why Stocks Keep Rising While Trade Headlines Stay Unresolved

TL;DR: Two finance headlines point to the same lesson: in uncertain weeks, market direction is decided less by one political event and more by how investors translate multiple weakly moving signals into positioning. While attention is fixed on Iran headlines and weekly economic releases, the market’s higher-order signal is that investors are rewarding businesses with resilient cash generation and boards that can defend margins under mixed macro conditions. If you are managing capital this week, treat geopolitics as a volatility tax, not a thesis driver; focus on data interpretation, balance-sheet resilience, and liquidity rules instead of chasing every headline. The Signal Is Moving from Geopolitics to Process The first headline frame is a list of this week’s U.S. macro events, while the second asks why stocks hold record territory without a geopolitical settlement. That pairing is the thesis: the conflict headline is now a background variable, not a primary valuation anchor. That does not mean risk has gone away. It means the market has become selective about what risk deserves capital. ) Why unresolved headlines still permit upside Headline risk usually works when a narrative is binary: either a policy break occurs or the path of least resistance continues unchanged. But a week without resolution tends to be interpreted as “status quo, no shock yet.” In that setting, investors often revert to what they can model: Operating leverage from stronger digital demand Ability to protect gross margins in softer-demand pockets Liquidity and refinancing durability for corporates The finance-week lens then shifts from event outcome to execution quality. What the record highs story is really saying The claim that equities can hold highs without Iran progress, as captured in the second headline, signals at least one of two things: either the risk is well-distributed across portfolios, or investors are alread

The Market’s Real Calendar: Why Stocks Can Stay High Without a Diplomatic Clue

TL;DR: This setup feels stable until it is not, and that is exactly why investors should expect short-term indecision to persist. The two candidate headlines point to a core market truth: when diplomacy on Iran remains unresolved, stock performance is still mostly set by the next wave of economic data and its implication for profits, inflation expectations, and financing costs. For finance teams, the edge is to treat unresolved headlines as background noise and design a scenario framework that survives both stronger-than-expected data and data misses, rather than react to every cable or tweet. Why markets can rally when geopolitics stalls Headline risk versus price-setting risk The J.P. Morgan headline explicitly says stocks can sit at record highs even without Iran resolution. That does not mean markets are unaware of geopolitical risk; it means markets may judge that uncertainty is being gradually priced and compensated through valuation, hedging, and positioning choices. In practice, that usually produces a sideways-to-up tape: headlines bump intraday volatility, but cash-flow assumptions, liquidity conditions, and macro signals decide whether the trend holds. From a business-finance viewpoint, the distinction matters: headline risk is a volatility tax, while repeated economic surprises are a directional tax on equity beta and credit spreads. If investors feel uncertain but not panicked, they may tolerate risk while keeping optionality via tighter risk limits rather than full de-risking. What this week’s economic signals are likely to dominate The June 15-19 data window as the next decision point The other headline centers on what to watch in economic data for June 15-19. That calendar framing is the right lens: not the geopolitics narrative itself, but the timing and quality of releases. As a practical filter, focus on upcoming inflation and labor trend signals and whether they alter expectations for earnings growth, input c

Why This Week’s Data Calendar and AI IPO Narrative Should Drive Your Next Finance Decisions Together

TL;DR: The next weeks for finance professionals are best treated as one joint decision problem, not two separate storylines. A weekly economic data window still determines what borrowing, spending, and hiring can sustain, while the AI mega-cap narrative is changing how households allocate risk across savings, spending, and career plans. If you connect these signals, you can move from headline-chasing to a structured playbook: adjust duration exposure to confidence risk, reduce single-theme concentration, and separate valuation risk from income risk. In short, treat macro data as the throttle and AI wealth effects as the steering wheel, especially as liquidity, talent, and innovation spending remain highly linked. 1) Start from the macro floor, then layer narrative The first headline points to a familiar but still underused discipline: weekly economic data sequencing. Market narratives can shift fast, but credit and cashflow are still ultimately constrained by policy, inflation expectations, and employment strength. In practical terms, the data calendar is not a static list; it is the environment that prices risk for the next 6–12 weeks. Investors often overfit to one strong data release and ignore the surrounding distribution of outcomes. A more durable process is to map each incoming release to three balance-sheet consequences: liquidity cost, demand durability, and refinancing timing. That mapping helps explain why the same data point can push equities and credit in opposite directions in different sessions. For finance teams, the key is not only “good vs bad” data, but whether each update confirms or contradicts the existing earnings curve. See Kiplinger’s data-watch framing for this week not as a news feed, but as a scenario map for your capital assumptions. 2) Where macro logic can still be systematized The old risk signals that still matter Inflation, labor momentum, and credit conditions still shape business margins and valuatio

From AI Hype to Balance-Sheet Reality: Why This Week’s Inflation Data Could Reset the Risk Curve

TL;DR: AI hype does not burst in one dramatic moment—it deflates where liquidity, hiring, and valuation discipline diverge. This week’s macro calendar matters because wage and inflation prints can change discount rates faster than corporate AI slide decks can, while equity positioning can trap even good firms in expensive sectors until proof of durable profits arrives. Treat the AI story as a stress test, not a prophecy: map which businesses turn AI narrative into recurring cash before the window closes. Why this AI cycle feels structurally different from the last narrative boom The AI conversation is no longer about “is AI real?” but “how long can capital fund it while rates, inflation expectations, and margin discipline remain supportive?” The first headline invites a scenario approach to a potential AI reset, while the second is effectively a checklist for the weekly signals that move markets from belief to math. This is a useful pairing: sentiment sets the price, but macro data sets the durability. ![AI, hiring, and macro feedback loop] The distinction matters. In prior waves, markets often extrapolated a single productivity story across broad sectors. Now, investors appear to price firms on two layered criteria: visible AI adoption and balance-sheet resilience under less favorable financing conditions. A company can still have excellent products and still lose valuation if investors conclude that every AI dollar spent now must be raised at higher cost, with slower pricing power than expected. The key lesson from the “AI bubble” framing is not fatalism. It is a warning against flattening all AI businesses into one sector trade. AI is becoming a cross-sector multiplier, but it is not a free one: it carries wage, compute, and hiring costs, plus policy risk. If inflation data or labor signals move against assumptions, the cost of these assumptions rises immediately. What this week’s macro prints can and cannot tell you The economic-data-focused headline is about practical surveillance: jobs, inflatio

From Private Rocket Bets to Public Balance-Sheet Risk: Why AI IPO Momentum Changes How Families Should Think About Money

TL;DR: AI is no longer a distant “innovation story” and becoming a household finance question. The SpaceX IPO framing suggests ordinary portfolios may now move with AI sentiment through pensions, payroll-linked ownership, and credit conditions, while the “bubble pop” framing warns that the downside is not one stock collapsing but a cross-asset re-pricing of liquidity and trust. The right response is not passive fear and not blind optimism; it is disciplined concentration reduction, stronger liquidity buffers, and explicit stress-testing of cash-flow plans. Why this headline signal is different from normal tech-cycle talk The two candidate angles point to different tempos of risk. One points to a future where a major AI-linked company’s public market presence broadens who feels exposed; the other asks what happens if speculative expectations unwind abruptly. Combined, they imply a shift: AI is becoming a macro variable in household finance, not just a sector theme. From elite-growth narrative to balance-sheet reality In past cycles, many households were indirectly exposed to AI through broad market index exposure. The post-IPO lens implies deeper exposure for ordinary investors because AI profits and valuation narratives are increasingly connected to wage and wealth channels. Workers receive compensation from AI-heavy firms, institutions rebalance retirement contributions through AI-heavy holdings, and banks price credit against sector cyclicality and revenue quality. That means the question is less “Should I own AI stocks?” and more “How much of my household resilience is unintentionally tied to AI multiple expansion?” This framing is visible in the SpaceX-linked AI discussion, but the practical implication is broader than any single company. How an AI bubble unwind can differ from a standard

AI’s Next Shockwave: Why the Real Risk Is Concentrated Winners, Not Just Big Valuations

TL;DR: The central issue is not whether AI is a bubble that will pop, or an engine that will only grow; it is that financial outcomes are becoming increasingly concentrated in a smaller set of firms and balance-sheet outcomes. The two headlines signal a market where household finances, payroll plans, and venture strategies are now exposed to the same concentration risk: a few AI-linked names can reprice risk for everyone. The edge for investors and business finance teams is to separate narrative strength from cash-flow durability, then run scenarios that survive lower multiples, higher rates, and slower adoptions. The useful lens: from “AI bubble” fear to concentration stress People often frame AI in binary terms: euphoric optimism versus imminent collapse. But both “AI bubble” headlines that question, and from the SpaceX IPO framing in the second piece that AI success narratives are now tied to highly visible public platforms. Bubble language is market shorthand The phrase bubble usually acts as a compression device for three different concerns: aggressive valuation, fragile financing conditions, and uneven distribution of gains. It often works as a cautionary signal, not a precise timing model. That framing can help, but it may also hide the actual mechanism that damages real-world portfolios: not every AI stock is equally exposed to every AI use case. Concentration is the hidden transmission channel When AI spending, talent flows, and procurement contracts flow disproportionately through a few firms, correlations rise. A single macro disappointment, regulation change, or margin

Beyond the Hype, Into the Balance Sheet: AI’s Bubble Debate and the New Risk Map for U.S. Investors

TL;DR: The central question is not whether AI is ‘real’—it clearly is, and fast—it is whether markets can keep pricing AI as endless growth without matching it with resilient cash flow and financing depth. The two headlines together imply a transition point: one asks how painful a bubble unwind could be, the other suggests AI may become a structural feature of U.S. financial life after a major IPO. For investors, the winning move is not to avoid AI, but to separate durable AI infrastructure economics from over-levered narrative bets and design portfolios for both a demand expansion path and a sentiment-downside path. The Debate Is Happening at the Right Time The first signal is obvious from the headlines alone: people are no longer asking “Should we own AI?” but “How does finance survive the period between hype and normalization?” This matters because public markets usually punish firms that looked visionary at the top and cash-fragile at the first contraction. The AI Bubble Question Is a Cash-Flow Question When the term bubble appears, investors often treat it as a morality tale of bad ideas. The practical version is narrower: did we assume too much future spending, too quickly, without the balance-sheet proof that survives slower quarters? A post-scenario where AI multiples compress is not a failure of AI progress. It is a failure of forecasting discipline. Why Timing the Debate Matters The AI fragility headline is useful because it highlights tail risk, not base expectation. In market terms, what matters is whether downside shocks are absorbable at the margin of debt, payroll, and budget policy. From Speculation to Structural Exposure After a Big IPO The second headline frames a tougher shift: AI could move from a stock-selection meme into household-level financial structure. A lar

If the AI Bubble Breathes Out, How Mega-IPO Liquidity and Public-Wallet Risk Could Reprice Everything

TL;DR: The finance question is no longer whether AI can grow, but whether public markets keep paying for growth before it is reliably backed by cash flow. Two headlines hint at the same stress point: a potential AI bubble unwind and a giant AI-linked public listing wave. If sentiment flips, the next weak point is often liquidity, not technology. That would hit growth budgeting, risk premium assumptions, and household portfolios faster than most investors expect. The right response is not to abandon AI, but to demand tighter evidence of pricing power, unit economics, and financing resilience before accepting headline-driven momentum bets. Market Setup: Two Signals, Same Stress Test The first signal is broad: market participants ask what an AI “bubble pop” would look like when valuations outrun earnings for too long. The second is specific: a high-profile, capital-intensive company goes public and anchors broader AI risk appetite. These are not separate stories. A mega-IPO can act like a thermostat for the whole ecosystem. If the listing succeeds cleanly with strong execution confidence, investors infer a liquidity backstop for adjacent firms; if it disappoints or raises funding concerns, the entire risk-on narrative is repriced quickly. Investors usually realize this only after risk repricing has already started. The key distinction is between innovation risk and funding risk. Innovation risk is real but slower-moving. Funding risk is immediate and can be amplified by public expectations, interest-rate sensitivity, and index-linked mandate flows. Why AI Valuation Psychology Can Snap Faster Than Revenue Models The central danger in this cycle is not the return of recession concerns or tech skepticism, but the speed at which valuation narratives can detach from business models and then reattach on the downside. The Market Reflex: “Proof After the Price” In euphoric periods, many investors treat strategic optionality as equivalent to guaranteed growth. Once price rises, disclosure quality and conversion metrics are often read as backward confirmation. In an unwind, the same disclosure is re-read as proof gaps. That is why a single miss on unit

If the AI Bubble Breathes Out, How Mega-IPO Liquidity and Public-Wallet Risk Could Reprice Everything

TL;DR: The finance question is no longer whether AI can grow, but whether public markets keep paying for growth before it is reliably backed by cash flow. Two headlines hint at the same stress point: a potential AI bubble unwind and a giant AI-linked public listing wave. If sentiment flips, the next weak point is often liquidity, not technology. That would hit growth budgeting, risk premium assumptions, and household portfolios faster than most investors expect. The right response is not to abandon AI, but to demand tighter evidence of pricing power, unit economics, and financing resilience before accepting headline-driven momentum bets. Market Setup: Two Signals, Same Stress Test The first signal is broad: market participants ask what an AI “bubble pop” would look like when valuations outrun earnings for too long. The second is specific: a high-profile, capital-intensive company goes public and anchors broader AI risk appetite. These are not separate stories. A mega-IPO can act like a thermostat for the whole ecosystem. If the listing succeeds cleanly with strong execution confidence, investors infer a liquidity backstop for adjacent firms; if it disappoints or raises funding concerns, the entire risk-on narrative is repriced quickly. Investors usually realize this only after risk repricing has already started. The key distinction is between innovation risk and funding risk. Innovation risk is real but slower-moving. Funding risk is immediate and can be amplified by public expectations, interest-rate sensitivity, and index-linked mandate flows. Why AI Valuation Psychology Can Snap Faster Than Revenue Models The central danger in this cycle is not the return of recession concerns or tech skepticism, but the speed at which valuation narratives can detach from business models and then reattach on the downside. The Market Reflex: “Proof After the Price” In euphoric periods, many investors treat strategic optionality as equivalent to guaranteed growth. Once price rises, disclosure quality and conversion metrics are often read as backward confirmation. In an unwind, the same disclosure is re-read as proof gaps. That is why a single miss on unit

AI as the Risk Offset: Why Equities Stay Elevated While Geopolitics Sit Unresolved

TL;DR: Markets can stay near all-time highs without diplomatic breakthroughs because investors are increasingly treating unresolved geopolitical risk as a hedged variable, not a deterministic reset. The two signals in your source queue point to the same setup: AI-related growth expectations keep anchoring forward valuations, while risk management tools absorb headline volatility faster than they did in prior cycles. For finance and business readers, the key move is to separate signal from noise—track how AI productivity, margins, and financing conditions evolve, then stress-test your own cash-flow and capital plans for volatility, not certainty. The setup: markets are rewarding cash-flow durability over headline certainty The two headlines you provided sit at the center of the current tension. J.P. Morgan notes that stocks can remain elevated without an Iran resolution. Morgan Stanley reports AI momentum continuing to support global markets. The market response has shifted from one where every headline reset expectations to one where headline risk is often priced into a pre-set volatility budget. That does not mean risk is gone; it means markets are deciding that risk has a price, and that price is currently acceptable against longer-duration earnings themes. What is being repriced At a practical level, investors are re-evaluating how much a geopolitical flare-up should affect discount rates versus projected earnings in the next few quarters. When AI-driven demand is broadening margins, valuation support can come from a different engine than macro certainty. This creates a paradox: headlines are po

When Narratives Decouple From Headlines: AI Liquidity Is Outlasting Geopolitical Deadlines

TL;DR: Two current headlines point to the same market logic from opposite angles: AI momentum is being priced as a durable earnings and spending theme, while unresolved geopolitical risk is increasingly treated as a manageable noise factor rather than a regime shift. That does not mean markets are reckless; it means investors are assigning a higher near-term weight to AI-driven earnings visibility than to headlines whose outcomes are uncertain in timing and magnitude. For investors, the implication is clear: differentiate between stories that change cash-flow probabilities and stories that change sentiment volatility. The tape is being driven by cash-flow narratives, not headlines The first headline frames a broad claim: AI momentum is still propping up global markets. The second asks why stocks remain near records even without a specific geopolitical resolution. Put together, they highlight a portfolio-level shift in market framing. AI as a valuation anchor Most valuation debates are no longer just top-down (rates, inflation, geopolitics); they are increasingly mixed with micro signals: software stack upgrades, infrastructure spend, and productivity narratives that can be refreshed every quarter. When investors believe a theme can repeatedly convert into billable output and scale, they are willing to tolerate a wider range of outside noise. Geopolitics as a delayed variable A non-resolution headline naturally invites fear of risk-off episodes. But unresolved issues become market shocks only when they cross a threshold: either they threaten physical supply chains, financial plumbing, or policy pathways enough to change earnings trajectories. Until then, they are absorbed as volatility tax rather than a fundamental reset, and equity risk appetite can stay intact. Why investors may tolerate “no news” headlines without de-rating A market at high valuation still can hold when the alternative to current risk allocation is worse than remaining exposed. The role of optionality in AI spending AI-cap

AI as the Market’s New Floor: Why Risk Assets Hold Their Ground While Geopolitics Remains Unresolved

TL;DR: In a market where unresolved geopolitics often trigger headlines but not necessarily broad de-risking, valuation discipline is increasingly being replaced by AI-linked earnings expectations as the immediate anchor. The key question is no longer only whether conflict risk rises or falls, but whether AI deployment can actually convert into durable margins, cash flow quality, and balance-sheet resilience. A practical way to read this tape is to treat AI as a forward earnings filter: upside persists when execution improves faster than cost, and risk returns the moment AI spending outpaces monetization. Why Markets Stay Composed While Geopolitics Remain Murky Headlines versus cash flow assumptions The first headline to watch is not a peace announcement; it is earnings commentary. If stocks are lifting to new records despite unresolved uncertainty, it means investors are deciding that uncertainty is not yet a binding constraint on expected cash flows. The J.P. Morgan headline on record highs without an Iran resolution suggests a strong setup: narrative stability is being substituted by model stability. The market is effectively applying a discounted-cash-flow stress test to the geopolitical variable. If a conflict scenario is costly but still bounded, and if companies continue to report expanding AI-related revenue, the equity board often gives patience. That does not mean blind calm; it means selective calm. Why AI Has Become the New Market Floor as a shorthand for the machine-learning demand channel A second strong signal in the day’s coverage is the framing that AI momentum supports global markets. This matters because AI is no longer a vague theme headline; it is increasi

When Four Sparks Hit at Once: Why Yesterday’s 953-Point Dow Drop Is a Volatility Reset, Not Just a Geopolitical Headline

TL;DR: The Dow’s 953-point drop, an Iran-related security escalation, mixed technology-company commentary, and the ECB’s policy signal arriving in the same broad window point to a market regime where headline-level uncertainty is translating into demand for optionality, not directional conviction. Traders are not choosing between growth and inflation yet; they are pricing the probability that these risks overlap. For investors, the practical question is not whether to be bullish or bearish today, but how to protect capital while waiting for a cleaner signal from policy tone, oil transmission channels, and corporate commentary that can sustain earnings expectations. The Day in One Frame The market opened from an uncommon macro-composite: a broad U.S. equity selloff, a geopolitical flashpoint, and an ECB-session narrative. In that environment, the 953-point Dow pullback matters less as a precise directional forecast and more as a stress read: portfolio managers are reallocating liquidity toward cash-like positions because event uncertainty crossed a threshold. The same day’s news mix also included Oracle coverage and ECB discussion in a single risk basket, a pattern that often creates whipsaw behavior in futures, FX, and credit simultaneously. ) Why 953 Points Is a Signal Beyond the Index Level A move of this scale is usually less about “one bad thing” and more about “several incomplete things.” When the tape sees conflict risk rise while macro readouts are not fully confirmed, each participant has to estimate second-order effects: inflation persistence, currency effects, supply chain insurance costs, and corporate capex confidence. The Meaning of Overlapping News With a geopolitical headline tied to U.S.-Iran tension, investors often treat

Financial Muscle as the New Market Edge: Why Liquidity Is Replacing Hype in 2026 Capital Rationing

TL;DR: Valuation debates are rotating from "story quality" to survival quality. The latest finance headlines frame a clear inflection: markets are rewarding firms that can fund operations through stress, finance growth without repeated capital raises, and avoid being forced into reactive decisions when the macro shifts. For investors, the winning question is no longer just who is winning market share this quarter, but who still owns strategic optionality after a liquidity squeeze. In this regime, pessimism about crowded themes can be productive if it forces more realistic scenario testing and less story-based valuation drift. The Narrative That Won't Outrun Liquidity The new spread between durable and fragile firms The first headline explicitly frames the current reset as a change from a technology-first lens to financial strength. That is a profound shift because it changes what “quality” means. A company can still innovate; it just must show how that innovation survives working-capital stress, funding dry-ups, and slower spending cycles. A firm with weaker cash conversion but a bold roadmap is no longer automatically a premium name. Instead, investors are asking: can this business defend execution quality when top-line noise appears? This is also a portfolio-level lesson, not a single-stock one. In an environment where macro data, rates, and sentiment can reprice risk quickly, the market discounts fragile structures faster. Liquidity is now embedded in valuation as a form of optionality, not a defensive footnote. From Hype to Optionality Why cash is a strategic option, not just a safeguard The second headline asks what pessimists may miss, and the hidden answer is that risk aversion can hide value in well-capitalized players before the crowd catches up. A company with stable operating cash and conservative refinancing assumptions can wait longer, invest incrementally, and buy market share when weaker peers are forced into dilution or cutbacks. That is how optionality is created in real time. The practical point: strong balance sheet positions are not purely passive protection. They permit strategic speed. [This is visible in recent market com

The May Jobs Report Kept the Fed in a Narrow Lane

TL;DR: The May jobs report gave investors the wrong kind of strength. The U.S. economy added 172,000 jobs, unemployment held at 4.3%, and wages kept rising, but the hiring was concentrated in leisure, local government, and health care while financial activities lost jobs. That mix makes Federal Reserve rate cuts harder to justify and tells investors this is not a broad white-collar boom. It is a narrow labor market that still keeps policy tight. #What The May Jobs Report Actually Said The clean headline from the Bureau of Labor Statistics' May employment report was strong enough to move markets: 172,000 jobs added, unemployment unchanged at 4.3%, and average hourly earnings up 0.3% in the month and 3.4% over the year. That sounds simple. It is not. The jobs were not spread evenly across the economy. Leisure and hospitality added 70,000 jobs, local government added 55,000, health care added 35,000, and social assistance added 12,000. Financial activities lost 22,000 jobs and are down 107,000 from a recent May 2025 peak. The point is not that the labor market is secretly weak. The point is sharper: the parts still hiring are not necessarily the parts that make investors comfortable paying rich multiples for rate-sensitive assets. #Why This Is A Rate-Cut Problem Markets wanted a labor report soft enough to keep the Fed's easing option alive. They got the opposite. Reuters reported that stocks, bonds, and gold sold off after the strong jobs print, with interest-rate futures showing a higher chance of Fed tightening by December and the Nasdaq falling sharply as investors backed away from rate-sensitive technology shares (via Investing.com). That reaction makes sense. A labor market can be uneven and still be too firm for rate cuts. The Fed does not need perfect breadth to stay tight The Fed's problem is not whether every industry is hiring. The problem is whether employment and wages are soft enough to offset inflation risk. May did not give policymakers that cover.

Palantir's NHS Review Exposes Public-Sector AI Renewal Risk

TL;DR: Britain is reviewing Palantir's GBP330 million NHS Federated Data Platform contract before an early-2027 break point, according to Reuters. The important business point is not whether one UK contract disappears tomorrow. It is that public-sector AI software revenue carries a renewal risk that ordinary SaaS math tends to smooth over: the buyer can decide the workflow works and still decide the vendor is politically, operationally, or procurement-wise too expensive to keep. #What Palantir's NHS Review Actually Tests Palantir has been priced by public markets as a company that can turn government and commercial AI demand into very high-margin software revenue. The NHS review tests a less glamorous part of that story: whether a public buyer keeps renewing after the platform becomes useful. That distinction matters. A private company can dislike vendor lock-in and still renew because the migration cost is annoying. A public health system has to defend the renewal in front of ministers, auditors, clinicians, unions, privacy groups, rival suppliers, and taxpayers. That is not normal churn risk. It is a standing committee hearing embedded inside the sales cycle. #Why A Break Clause Is A Financial Event The UK Parliament answer from April 16, 2026 said the NHS Federated Data Platform contract runs for seven years, ending in 2030, with break clauses at three years, two years, and one year. Reuters reported that Technology Secretary Liz Kendall said the current health secretary is reviewing the contract before the government decides whether to extend it beyond the initial term in early 2027. Investors often talk about software contracts as if duration equals security. In public-sector AI, duration is only the outer frame. The real asset is the right to survive the next renewal test. The workflow can work and still be commercially fragile That is the uncomfortable part for Palantir bulls. The government does not have to prove the plat

WhiteHawk's IPO Says Public Markets Want Gas Cash Flow Without The Drill Bit

TL;DR: WhiteHawk Minerals priced an upsized IPO of 7.7 million shares at $26, raising about $200 million before the greenshoe. The interesting part is not another energy listing. It is that public markets are showing renewed appetite for gas exposure that looks more like a toll road than a drilling program. Most energy equity pitches still ask investors to believe two things at once: commodity prices will cooperate, and management will spend capital with unusual discipline. WhiteHawk is selling a different proposition. Own the minerals, let somebody else drill, and collect a slice of the production stream. That distinction matters more than it sounds. In a market still crowded with AI-capex stories, rate debates, and quarter-to-quarter earnings noise, WhiteHawk is really a financing story about what kind of cash flow Wall Street wants to underwrite. The IPO Is Really A Vote For Capital-Light Energy Exposure WhiteHawk says its portfolio spans about 3.4 million gross DSU acres concentrated in the Appalachian and Haynesville basins. In its amended prospectus, the company says that footprint gives it exposure to more than 10,900 producing wells and that mineral and royalty interests generated about 99% of 2025 royalty revenue. That is the core of the pitch. WhiteHawk is not asking public investors to fund rigs, frac crews, and operating blowups. It is asking them to buy a claim on acreage and production economics while third-party operators carry most of the execution burden. This is why the upsize matters. The original deal was marketed at 6.925 million shares. It priced as a 7.7 million share offering instead. That does not prove the stock is cheap. It does suggest institutional buyers were willing to fund a structure that strips o

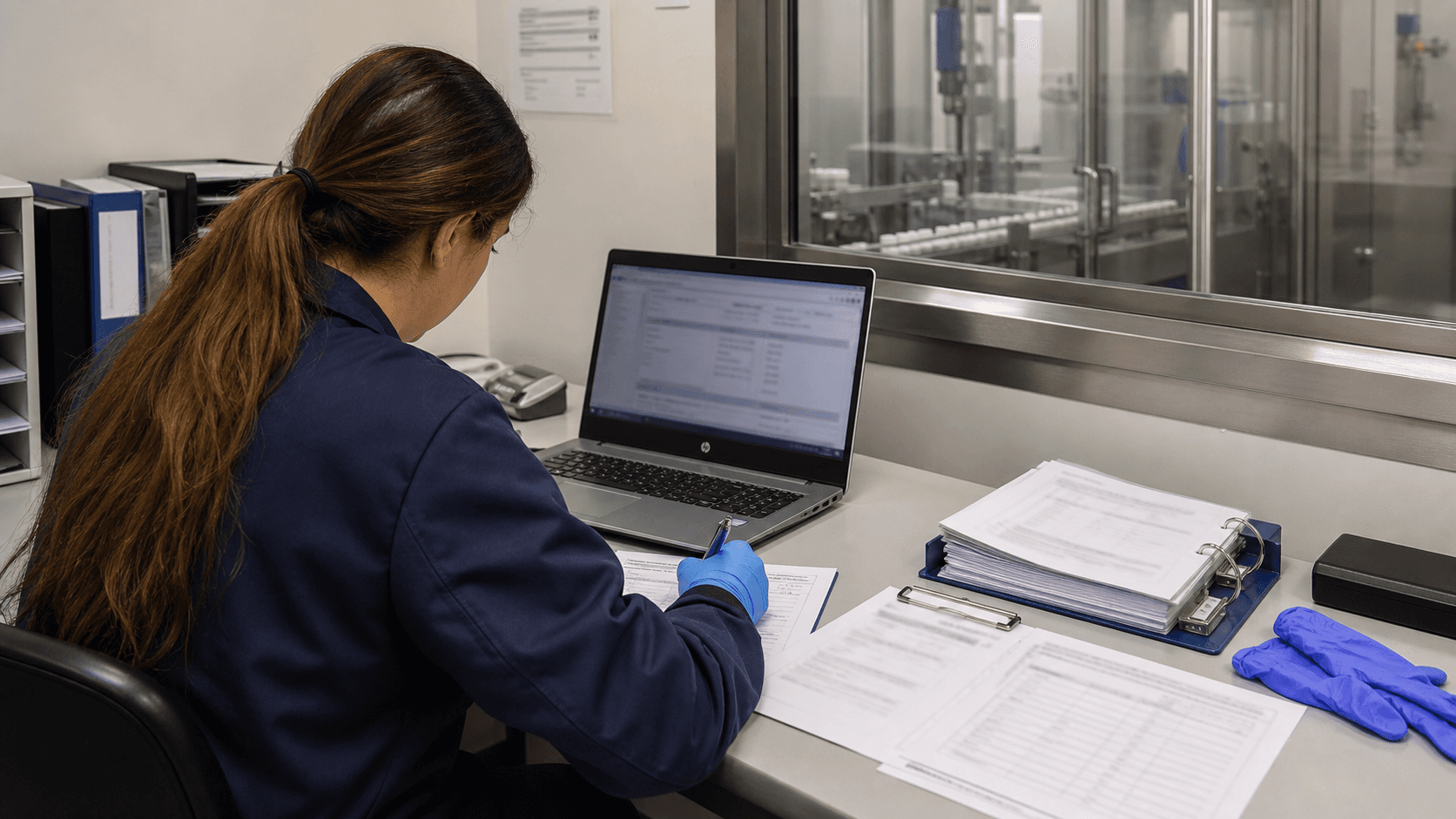

Thoma Bravo's Kneat Deal Prices Life-Sciences Validation Workflows

TL;DR: Thoma Bravo agreed to buy Kneat for about C$650 million, and the interesting part is not the take-private premium. It is the kind of software being priced: digital validation and quality-process automation for life-sciences companies. In regulated pharma and medtech, workflow software can become sticky because replacing it means revalidating evidence, approvals, audit trails, and trust. #What Thoma Bravo Is Really Buying In Kneat Thoma Bravo's all-cash deal for Kneat values the company at roughly C$650 million, with shareholders set to receive C$6.50 a share if the transaction clears approvals. That is the headline. The better business question is why a private-equity software buyer wants a company built around validation records, quality workflows, and life-sciences compliance. Kneat is not selling a prettier spreadsheet. It is selling a system of record for work that regulated manufacturers cannot casually improvise. Why validation software is not ordinary SaaS In a normal software budget, a department can replace a tool because a cheaper vendor appears, a contract expires, or a CFO wants consolidation. In a regulated life-sciences plant, the decision is messier. The software touches evidence that a process, system, cleaning method, package line, or equipment setup was tested, approved, and controlled. That makes the switching cost procedural, not just technical. #Why The Validation Desk Has Pricing Power Picture a quality-assurance worker at a desk beside a cleanroom window. There is a laptop, a stack of validation forms, a binder, gloves, and a production line behind the glass. The job is not glamorous. It is also not optional. When a drugmaker or medtech company moves from paper-heavy validation to digital workflows, the buyer is trying to reduce manual handoffs, missing signatures, duplicate records, and audit scramble. Kneat says its platform is used by 8 of the world's top 10 life-sciences companies, which tells you where

Realtor.com's May Housing Report Turns Price Cuts Into Payment Math

TL;DR: Realtor.com’s May 2026 housing data shows a market where list prices are finally bending, but mortgage rates still keep the monthly payment in charge. The business implication is simple: housing is no longer sold mainly through scarcity. Brokers, builders, lenders, and sellers now have to sell payment math, concessions, and timing. That shift changes where pricing power sits in the housing transaction. #What Realtor.com’s May Housing Report Actually Says The clean headline from Realtor.com’s May 2026 report is that the national median list price fell 2.4% from a year earlier, the steepest annual decline in its data going back to 2017. That sounds like relief. It is not quite relief. The median list price was still $429,500 in May, and Realtor.com said inventory remained 11.6% below typical 2017-2019 levels. Sellers are adjusting, but the market is not suddenly cheap. The more interesting detail is behavioral. Pending sales have now grown year over year for six straight months, a streak Realtor.com said had not happened since early 2021. Buyers are not gone. They are waiting for sellers to admit the payment has changed. #Why The Monthly Payment Now Runs The Sale Mortgage rates are the quiet boss in this story. Freddie Mac said the 30-year fixed-rate mortgage averaged 6.48% for the week of June 4, 2026, down from the prior week but still high enough to make a small price cut feel smaller than sellers want it to feel. At a kitchen table, that difference is not theoretical. A buyer does not experience a 2.4% lower list price as a market statistic. The buyer sees a preapproval letter, a tax estimate, an insurance line, and a monthly payment that still starts with the wrong number. That is why this is a business story, not just a housing story. The transaction is being repriced around cash flow. Why a cheaper listing can still feel expensive A seller may think a $15,000 price cut is generous. A buyer may see only a modest monthly-payment improvement once taxes, insurance, and mortgage rates are

Arch Capital's $2 Billion Bond Deal Puts Insurance Pricing On The Liability Desk

TL;DR: Arch Capital Group priced a $2 billion senior-note offering that is expected to close on June 9, 2026, with $600 million due in 2036 and $1.4 billion due in 2056. The obvious read is refinancing. The better read is insurance capital discipline: a specialty insurer is paying up for long-dated balance-sheet certainty while catastrophe risk, casualty inflation, mortgage credit, and rating-agency scrutiny keep making "capacity" more expensive to promise. #What Arch Capital Is Actually Buying With Long-Dated Debt At an insurance company, a bond deal is not just a treasury chore. It is part of the product. Arch said it priced $600 million of 5.250% senior notes due 2036 and $1.4 billion of 5.950% senior notes due 2056. The proceeds are meant to retire $500 million of 4.011% notes due 2026, fund tender offers for older notes due 2043 and 2046, and leave any remainder for general corporate purposes. That sounds plain. It is not. Arch is taking short-near-term refinancing risk and turning it into long-duration certainty. The coupon is higher, but the company gets a cleaner capital runway. For a reinsurer and specialty insurer, that runway matters because customers do not buy only policy language. They buy the confidence that the balance sheet will still be there when the bad year arrives. #Why The Coupon Is The Visible Cost, Not The Whole Cost The old 2026 notes carried a 4.011% coupon. The new 2036 and 2056 notes cost 5.250% and 5.950%. That spread is the easy headline. It is also the least interesting part. The real trade is flexibility versus cheapness Arch could wait, roll less debt, or keep more refinancing risk near the front of the curve. Instead, it is accepting a higher stated cost to reduce the chance that a rough insurance market, a catastrophe year, or a credit-market freeze forces capital decisions at the wrong time. The prospectus supplement says Arch expects about $1.97 billio

Johnson & Johnson's Firefly Bio Deal Puts Oncology Optionality On The Balance Sheet

TL;DR: Johnson & Johnson agreed on June 8, 2026, to buy Firefly Bio for $1 billion in cash, adding a preclinical degrader antibody conjugate platform aimed at KRAS-driven solid tumors. The deal matters because J&J is not buying near-term revenue. It is paying an oncology option premium: a way to keep pipeline breadth alive while patent pressure, clinical risk, and payer scrutiny make every future cancer franchise harder to defend. #What Johnson & Johnson Actually Bought Johnson & Johnson said it will acquire Firefly Bio for $1 billion in cash, with closing expected later in 2026 subject to regulatory approvals and customary conditions. The asset is not a marketed drug. Firefly Bio is advancing Firelink, a degrader antibody conjugate platform designed to deliver a protein degrader to tumor cells while avoiding healthy cells. J&J framed the platform around pan-KRAS and other hard-to-treat cancer drivers. That is why the transaction is more interesting than its size. A $1 billion all-cash deal is small inside J&J's balance sheet. It is large enough, though, to show how big pharma now buys uncertainty. The company is not filling a quarterly revenue hole. It is buying a new path through a target class where the science has improved, but the commercial proof is still far away. #Why KRAS Changes The Price Of Optionality KRAS has been a famous problem in oncology because it is common, difficult, and commercially tempting. The National Cancer Institute says more than 30% of all human cancers are driven by RAS-family mutations, including high shares of pancreatic and colorectal cancers. That makes the target valuable. It also makes it crowded. The platform is the wager, not one molecule The important phrase in the Firefly announcement is not only "KRAS." It is "platform." Big pharma likes platforms because they can justify a portfolio view: one acquisition may produce multiple shots on goal, multiple tu

Med-Metrix's $147 Million Vitalware Deal Prices The Hospital Billing Desk

TL;DR: Med-Metrix agreed to buy Health Catalyst's Vitalware business after Health Catalyst disclosed a $147 million base cash purchase price in a June 4 SEC filing. The deal matters because hospital revenue-cycle software is no longer just back-office tooling. In a world of denials, prior authorization friction, and stretched provider margins, cleaner coding and charge capture can look like recoverable cash. #What Med-Metrix Is Actually Buying Med-Metrix is buying Vitalware, Health Catalyst's mid-revenue-cycle business, and Health Catalyst's Form 8-K says the buyer agreed to pay a $147 million aggregate base purchase price, subject to customary adjustments. The buyer's release describes Vitalware as a revenue workflow and analytics software business that supports coding accuracy, charge capture, chargemaster management, compliance, and price transparency. Med-Metrix said the asset should strengthen its mid-revenue-cycle offering and help improve net revenue yield for clients. That phrase sounds dull. It is not. Net revenue yield is the difference between a hospital performing work and a hospital actually collecting the dollars it is allowed to collect. That is where a lot of healthcare economics hides. #Why The Billing Desk Is Becoming More Valuable Hospitals do not experience reimbursement pressure as a neat policy debate. They experience it as files, edits, denials, resubmissions, appeals, and aging receivables. The American Hospital Association's 2026 Costs of Caring report says hospitals spent $43 billion in 2025 trying to collect payments from insurers for care already delivered. It also says roughly 56% of hospital costs were tied to service lines where reimbursement fell short of the cost of care delivery. That is the background that makes Vita

OceanFirst's Flushing Deal Shows Regional Bank M&A Now Needs An Equity Backstop

TL;DR: OceanFirst closed its merger with Flushing Financial on June 1 and paired it with a $225 million Warburg Pincus investment. The important part is not that another regional bank got bigger. It is that a regional-bank merger now arrives with an outside equity escort, conservative credit marks, and an explicit plan to shrink commercial real estate concentration over time. That is a clue about the new merger math in banking: scale still matters, but clean capital matters more. #What OceanFirst Actually Bought You can picture the obvious part of this deal easily enough: a bigger regional bank, more branches, broader geography, more corporate talking points about reach and capabilities. OceanFirst said the completed combination creates an approximately $23 billion regional bank operating 71 retail branches across New Jersey, New York, Long Island, and Pennsylvania. Flushing shareholders received 0.85 OceanFirst shares for each Flushing share, and the merged board now includes ten legacy OceanFirst directors, six legacy Flushing directors, and one from Warburg. That is the surface. The deeper signal is that OceanFirst did not just buy Flushing. It brought in Warburg Pincus at the same closing table with a $225 million equity investment. If a straightforward scale story were enough, that extra capital would not be the part worth s

Britain's Money Fund Rewrite Puts A Yield Tax On Cash

TL;DR: Britain's Financial Conduct Authority softened its most aggressive draft for money market fund reform on June 8, but the real message did not get looser. Money market funds still sit at the center of corporate cash management and as an alternative to bank deposits, and regulators are making them carry more resilience even if that means some yield has to be left on the table. #What the FCA changed in UK money market fund rules The headline out of London sounds modest. The FCA said it would no longer push the bluntest version of its earlier money market fund proposal, which had called for all UK funds to raise daily liquid assets to 15% and weekly liquid assets to 50% of assets. Instead, the regulator now plans to keep current minimum weekly liquid asset rules in place, while setting a strong supervisory expectation that stable-NAV money market funds hold 40% weekly liquid assets and variable-NAV funds hold 20% to meet a new resilience requirement. It also plans to keep current daily liquid asset minimums and move ahead with so-called delinking, plus tighter know-your-customer expectations around investor concentration and correlated withdrawals. That sounds like a climbdown only if you think the fight was about one ratio. It was not. The fight is about whether a product sold as cash management can keep offering attractive yield without carrying more idle liquidity inside the wrapper. Why the 40% and 20% weekly liquidity numbers matter The important number is not just the final level. It is the message that liquidity buffers are no longer a nice-to-have comfort feature when institutional cash starts moving at once. #Why this matters well beyond London Money market funds are not a side show. The UK government and FCA described them in May as widely used by [asset managers, insurers, pension funds, large corporates and local authorities](https://assets.publishing.service.gov.uk/media/6a059b2622977ebc82cb3f5d/TheGovernmentandFCAannounceplanstoreformUKMoneyMarketFundReg

FHLB Des Moines Turns VantageScore 4.0 Into Mortgage Funding Plumbing

TL;DR: The Federal Home Loan Bank of Des Moines said its more than 1,200 member institutions can now pledge eligible mortgage collateral using VantageScore 4.0, extending the credit-score shift that Fannie Mae and Freddie Mac began implementing in April 2026. The business implication is narrower and more interesting than a housing-access headline: credit-score competition is moving into bank funding plumbing, where collateral eligibility can shape which loans lenders are willing to hold, finance, and repeat. #What Changed At FHLB Des Moines FHLB Des Moines is not a flashy consumer brand. That is why this matters. The institution sits behind the mortgage market, lending to member banks and accepting eligible collateral across a district that includes Alaska, Hawaii, Iowa, Minnesota, Missouri, Oregon, Washington, and several other states and territories. When it says a member can submit mortgages evaluated with VantageScore 4.0, the change lands in the back office before it lands on a real estate app. The public headline is inclusion. VantageScore says its newer model can evaluate millions more borrowers, including people with thinner credit files. The business story is collateral. If a loan can be more easily pledged into a Federal Home Loan Bank funding channel, a lender has a cleaner path to balance-sheet liquidity. That does not make mortgage credit cheap. It does make the loan easier to fit into the machinery banks use after origination. #Why The Credit Score Fight Is Really A Funding Fight Most borrowers experience a credit score as a yes-or-no gate. Lenders experience it as a workflow variable. Can the loan be sold? Can it be pledged? Can it survive an audit? Can the credit team explain the file when rates move, delinquencies rise, or regulators ask why a risk bucket grew? That is the part casual readers miss. A scoring model does not need to change the whole mortgage market overnight to matter. It only needs to become acceptable inside enough secondary workflows that lenders stop

Cegid's Shine Deal Makes SMB Accounting A Credit-Market Bet

TL;DR: Cegid closed its acquisition of Shine on June 8, creating a European SMB finance platform that combines accounting, e-invoicing, payroll, business accounts, payments, tax, HR, and reporting. The overlooked point is not the AI label. It is that boring compliance workflows are becoming financed software assets, backed here by a new €1.1 billion debt facility, because the company that controls the small-business ledger can also control payments, data, retention, and distribution to accountants. #What Cegid Actually Bought With Shine Cegid said it completed the Shine acquisition, creating what it calls a fully integrated, cloud-native, AI-driven financial hub for SMBs and accounting professionals in Europe. That is a long way of saying something simpler: Cegid wants the small-business finance desk before a bank, payroll vendor, tax app, or accountant-only workflow gets there first. Shine brings more than 400,000 SMB customers. The combined group is expected to serve more than one million SMBs and 15,000 accountants across France, Germany, Spain, Portugal, Denmark, the Netherlands, and Belgium. Why the customer count matters less than the workflow A small business does not wake up wanting an AI financial copilot. It wakes up needing to send an invoice, pay an employee, check cash, file tax data, and avoid a compliance mistake. The company that sits inside those tasks sees the business before the lender sees it, before the payments provider sees it, and sometimes before the owner understands the cash pinch. That is the asset. #Why This Is A Credit-Market Story The deal was funded through Cegid's operating cash generation and a new €1.1 billion financing facility provided by direct credit funds, after prior underwriting by Citibank, J.P. Morgan, RBC Capital Markets, and UBS. That financing detail deserves

GoHealth Chapter 11 Puts Medicare Broker Economics On Trial

TL;DR: GoHealth filed a prepackaged Chapter 11 case on June 7, 2026, with lender and shareholder support, aiming to exit before the next Medicare annual enrollment season. The bigger business point is not simply that another public de-SPAC-era healthcare company broke. It is that Medicare brokerage economics are being forced to value renewal quality, carrier trust, and cash conversion over headline enrollment volume. #What GoHealth's Chapter 11 Actually Signals GoHealth said it voluntarily filed Chapter 11 petitions in Delaware to implement a prepackaged plan backed by 100% of its lenders, more than 60% of its Class A shareholders, and more than 99% of GoHealth Holdings holders. That support matters. This is not a supplier-lock-the-doors bankruptcy story. GoHealth says it plans to keep operating, pay ordinary-course obligations, protect carrier and customer relationships, and emerge before the 2026 annual enrollment period. The sharp read is simpler: the Medicare broker model is no longer being rewarded for producing a flood of applications. It is being judged on whether those applications renew, whether carriers still want the members, and whether commissions turn into cash quickly enough to support the capital structure. #Why The Medicare Broker Business Got More Ruthless Medicare enrollment looks like a marketing business from the outside. Buy leads, staff licensed agents, match seniors to plans, collect commissions. Inside the machine, the economics are more unforgiving. A submitted application is only valuable if the member stays, the plan partner likes the cohort, and the commission receivable is not quietly overstated by future churn. The balance sheet is downstream of the call center Picture a licensed agent in October with a retiree on one line, a plan comparison screen open, and a list of doctors