Health Insurers Are Healing. Employers Aren't.

The market has spent this month looking for proof that health insurers are finally getting control of medical costs. It may be finding that proof. But that does not mean American healthcare inflation is cooling down. It may just mean the pain is moving.

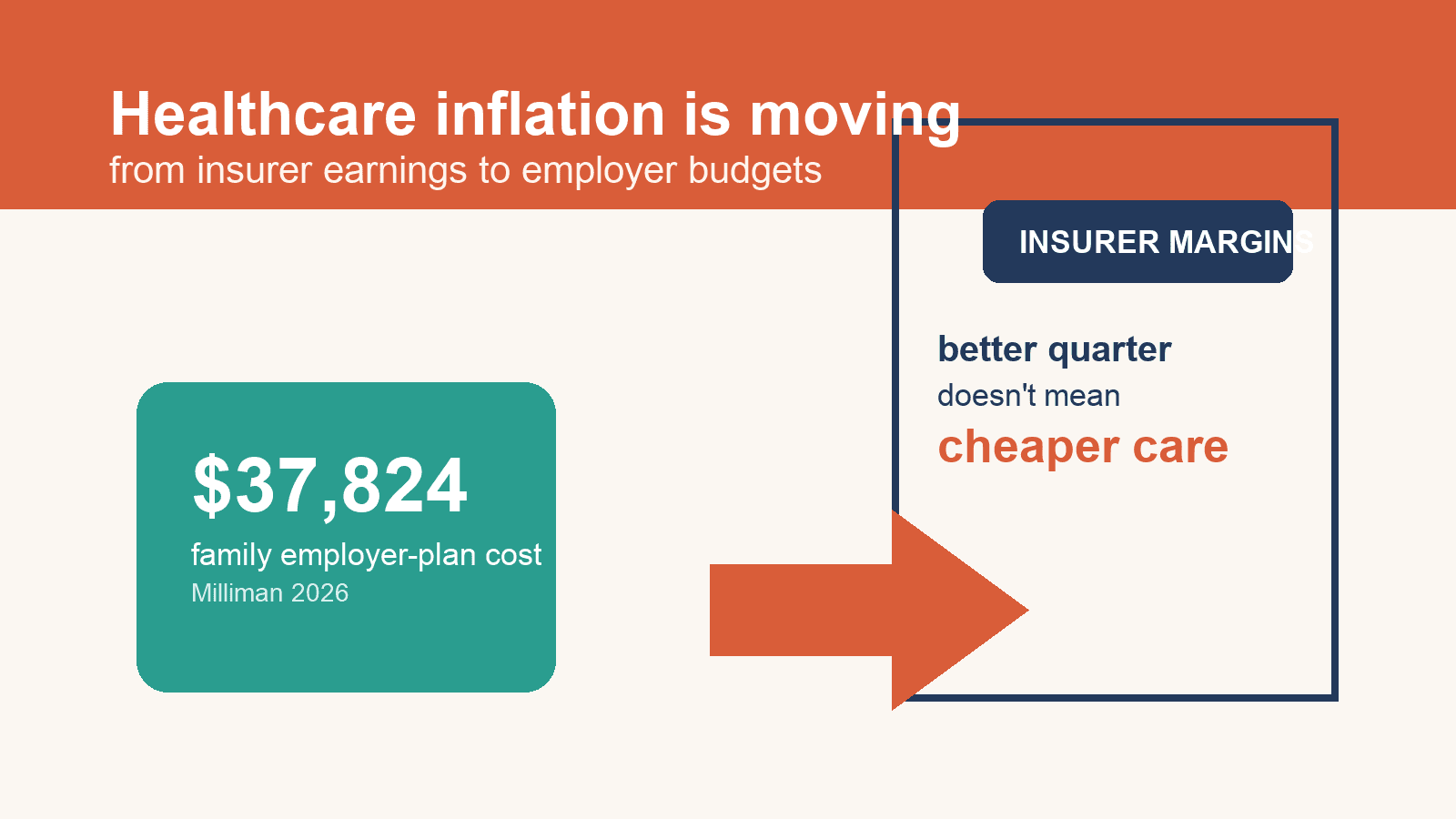

That is why the latest mix of data matters more than the headline stock reaction. Milliman said this week that healthcare for a typical family of four covered by an employer plan will cost $37,824 in 2026. For the average person, the figure is $8,460, up 7.9% from 2025. Milliman says that is the biggest increase in more than a decade if you strip out the pandemic distortions.

Here is the part casual readers are missing: insurers can look healthier at the exact moment employers and workers feel less healthy financially. Those are not contradictory facts. They are the same system redistributing pressure.

Reuters reported last week that first-quarter results from large insurers pointed to more stable medical costs after years of pressure. CVS raised its 2026 forecast after improving cost controls. Other major managed-care companies also beat expectations, and analysts said medical trends might finally be decelerating. That is good news for healthcare stocks that spent the last few years trading like every earnings season carried a claims surprise.

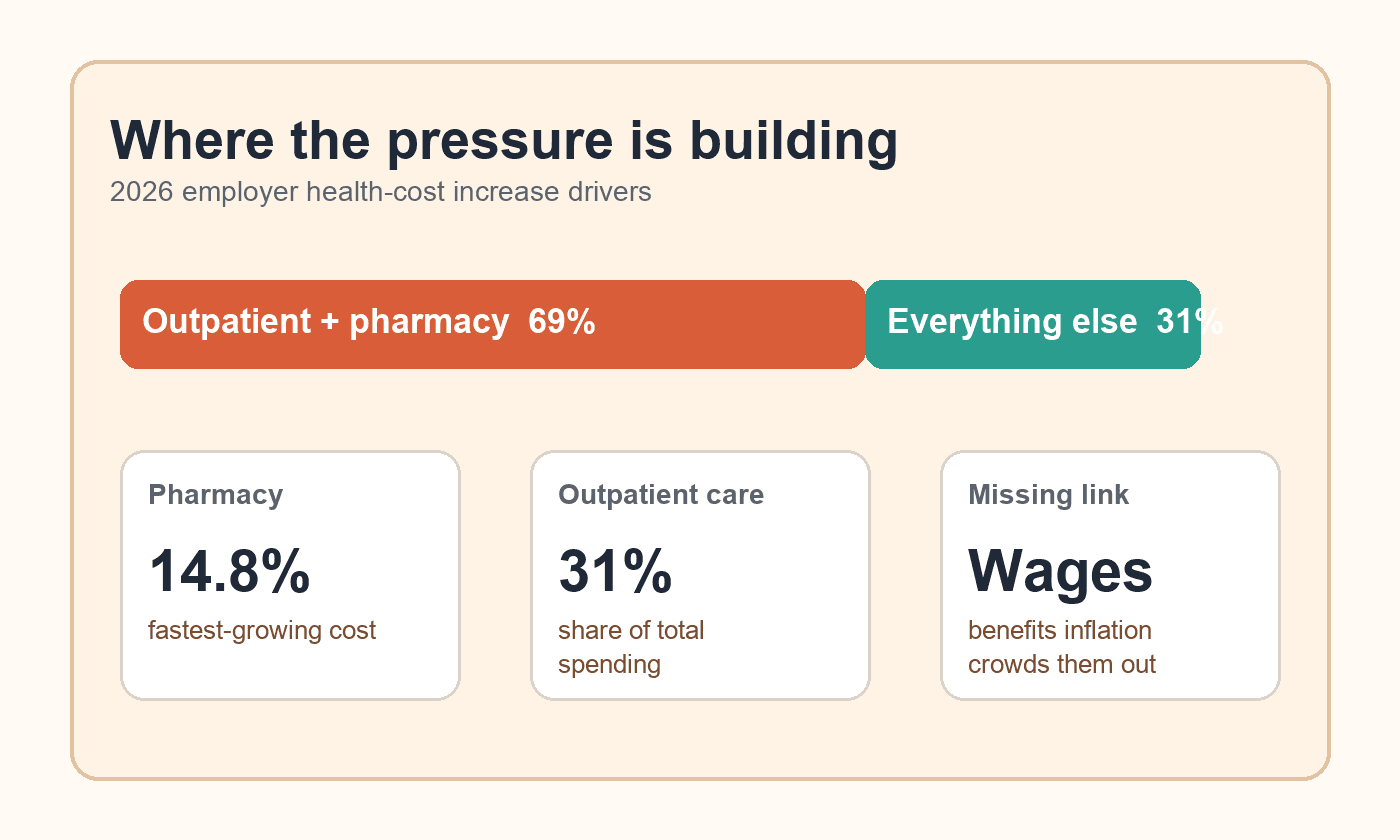

But Milliman’s report shows why that relief should not be confused with affordability. Outpatient facility care and pharmacy services drove 69% of this year’s increase in employer health costs. Pharmacy was the fastest-growing component, up 14.8% year over year for the average person. Outpatient care now represents roughly 31% of total employer-sponsored healthcare spending.

That mix matters. It says the inflation is not just coming from one bad flu season or one insurer losing control of a Medicare book. It is coming from a broader cost structure that is still marching higher through drugs, outpatient settings, and billing complexity. If insurers are stabilizing margins, they are doing it by managing the flow better, not by making the underlying river smaller.

That has a real business consequence. Employer health insurance is one of the least visible lines in the cost structure of the U.S. middle class. Workers do not experience most of it as a single sticker price. They feel it through slower raises, higher payroll deductions, skinnier plan design, tougher formularies, or a deductible that quietly resets the family budget. Employers feel it as a tax on compensation. Every extra dollar needed to hold a health plan together is a dollar that cannot go to wages, hiring, or margin protection.

This is why I think the bigger market takeaway sits outside the insurers themselves. If medical-cost pressure is shifting away from managed-care earnings volatility and into employer benefit budgets, then the next earnings strain may show up in labor-intensive sectors with limited pricing power. Restaurants, retailers, logistics operators, manufacturers, and local service businesses do not need a recession to feel weaker. They just need benefits inflation to keep outrunning productivity.

There is also a policy tell here. CMS finalized a 2.48% average increase in Medicare Advantage payments for 2027 in April, while saying it wants better payment accuracy and tighter coding discipline. That may help taxpayers, but it also means insurers still have reason to keep redesigning benefits and managing utilization tightly. So even if Wall Street stops fearing an insurer margin collapse, households should not assume the coverage experience gets easier.

My read is simple: healthcare inflation has become less of a pure insurer story and more of a labor-market story. The companies recovering first may be the ones best able to pass, route, or manage the cost. The people left holding the least visible part of the bill are employers and employees.

That is why the recent insurer rebound and the Milliman data belong in the same frame. One tells you the system is adapting. The other tells you the system is not getting cheaper. For investors, that is a meaningful distinction. Margin recovery inside managed care can coexist with a broader affordability squeeze across the real economy.