No Peace Deal, Still Green Tape: A Data-First Playbook for the Risk Window

TL;DR: Markets can stay near record highs even without a clean geopolitical breakthrough because prices often reflect a risk-management bargain: participants assume stability unless fresh data forces a repricing. In the coming week, the key edge is not prediction of a headline event but disciplined calendar trading—filtering signals from inflation, labor, and growth read-through while respecting positioning already built into the tape. If data surprises are mild, the path of least resistance remains trend-consistent gains; if surprises become violent, the same market can switch quickly from patience to de-risking. Why record levels can coexist with unresolved geopolitical risk The headline tension is intuitive: no Iran resolution should not automatically equal immediate market stress. One reason is that investors can keep the status quo in a “known-uncertain” bucket as long as risk controls are preserved in real time. That bucket narrows only when one side loses access to liquidity support, or when the range of outcomes becomes too wide for carry trades and valuation multiples to absorb. J.P. Morgan’s framing around record highs without political resolution points to this same state of pricing discipline rather than complacency source. What that means for positioning Liquidity is not just cash or credit volume; it includes implied tolerance for overnight headlines. As long as participants are not forced to run from risk, rallies can continue despite unresolved conflict. The signal to watch is whether portfolios are still adding duration risk, cyclical beta, and select small-cap quality names—or quietly trimming under the surface. The hidden variable: narrative durability A narrative is durable when it explains price behavior across several data points. If the same narrative (“geopolitics is noisy but contained”) survives a ru

When Data Beats Drama: Why Markets Hold Records Without a Geopolitical Truce

TL;DR: This week's market tension is a contrast game between scheduled economics and unsolved geopolitics: macro data sets the trend line while headlines inject volatility around the edges. Even without a Middle East resolution, equities can stay elevated if labor, inflation, and growth signals remain constructive for profit expectations. The practical message is simple: track data reliability and reaction quality, not one headline; then treat geopolitical noise as a volatility tax that changes position sizing, not your base thesis. The two headlines point to a recurring market pattern: price leaders can look irrational to outsiders, yet remain highly rational in context. The first headline signals that traders are staring at the next wave of macro prints, while the second says policy and earnings can keep pushing valuations if the risk premium does not rise faster than earnings surprise quality. The market is separating signal from story The macro calendar is now the central variable When traders worry about the same theme for many days, they eventually price uncertainty into a spread and move on to concrete inputs. A weekly list of major releases may sound routine, but routine is exactly what drives compounding gains in broad indices: every missed disaster and every resilient hard number becomes incremental confidence. This is why a full schedule of labor, inflation, and growth prints often matters more than one-off political speeches. It gives participants a process a

Hope Trades and Underpriced Rates: Why the Iran Headline Rally May Be Risk Repricing, Not a New Bottom

TL;DR: Markets are reacting to two separate but linked narratives: a political opening with Iran that could reduce near-term energy friction, and a market view that may still be underpricing how much the Fed keeps policy restrictive. The immediate rally is likely a hope trade, but durable returns usually require proof in energy inventories, wage momentum, and inflation data—not just headlines. In this piece, I separate sentiment from policy signal so investors can treat today’s move as a risk-shift setup, not a blind chase of a one-day rebound. Headline risk impulse: what the market is pricing right now The two headlines point to a familiar financial pattern: geopolitically induced optimism can push broad risk assets higher even when valuation math is unchanged. The finance headlines indicate that US shares rose as expectations grew that a U.S.-Iran arrangement might reduce energy-market uncertainty, and that markets may still be discounting a softer Fed path than currently implied by one set of expectations from asset pricing models. This matters because investors often confuse direction with durability. A political headline can improve sentiment quickly; it can also be reversed quickly if details fail to materialize. The first task is therefore to distinguish narrative-driven repricing from fundamental repricing. Hope can price better before reality does A headline suggesting reduced geopolitical friction lowers the perceived risk of sudden oil supply shocks, so equity investors may compress risk premia and bid up cyclicals and financials. That is exactly what the “market climbs” angle reflects. Better optics in one asset class often masks another Even if energy markets look calmer, that does not automatically mean inflation expectations, credit spreads, or funding conditions are improving at the same pace. This is why [markets rallying on conflict de-risking headlines](https://news.google.com/rss/articles/CBMiugFBVV95cUxNTGExUWx1WGZaNmtxTXJLZ1pNMmZ2dUg0dmJLTExtX1NXZURmZS1lNEQ2ZXIzdmxVZTdQdmtERU1PcnNXVU5YUGtXbWhPY3NjREtUYXhfUnN6aDRPNGhvWmFEbnlNWlNTcjdDUU5zMkxSaFZqVXdYZWhvUU1XNDZqcTNoZXp1Vk1sM3E4Q2NDWXgwcE1CdHo0RVdNMk5fUE00NVRIZ193NG03T3BUR0M

Markets Without a Deal: Trading a Geopolitical Void with Calendar-First Discipline

TL;DR: Equities near records while the Iran question remains unsettled are not necessarily ignoring geopolitics; they are often trading through it by treating the risk as a managed probability cost. That setup is stable only if cash flows and data-driven expectations stay coherent, but it becomes fragile the moment key economic prints differ from forecast. This week should be framed as a shift from headline narrative to calendar execution: track liquidity, monitor how each data print changes policy-path probabilities, and size exposure so a single surprise does not force a liquidity-driven unwind. Keep the focus on probabilities, not predictions. Why Markets Can Stay Elevated in the Absence of a Deal Risk Is Still Present, But It Is Being Priced Differently The headline message from JP Morgan suggests, equity markets can remain near records when investors believe the most probable downside scenarios are contained in the near term. This does not mean risk is absent; it means the market is assigning the unresolved issue a finite discount rate. Practically, risk is now split into two buckets: Scenario risk: whether the geopolitical environment worsens before the next major economic read. Discipline risk: whether investors stay forced-buy/sell and ignore their own risk budget when the narrative gets loud. The first is harder to eliminate, the second is avoidable. In other words, this is less about “are stocks irrational?” and more about “are investors respecting their own process?” From Story Risk to Execution Risk When markets get used to unresolved headlines, they stop waiting for one defining announcement and start caring about execution quality. The price action be

No Iran Deal, Strong Data: Why Stocks Can Still Grind Higher While Volatility Waits

TL;DR: Despite the unresolved Iran headlines, stocks can still hold up if this week’s data keeps supporting demand, margins, and financing resilience. The real edge is separating narrative risk from pricing risk. If geopolitics stays in headlines only, markets usually re-rate around rates, growth visibility, and liquidity, not slogans. If it starts moving those channels, you should shift quickly from conviction to protection. Treat the week as a two-track model: stay exposed where earnings quality is visible, and pre-hedge sectors with high geopolitical sensitivity. Why a Missing Deal Is Not Automatically a Market Breaking Point Narrative risk versus pricing risk The JPMorgan headline asks the key question directly: why are stocks still near records with no Iran resolution? That framing already implies something important: markets are not always backward to hard news, but they are very forward to price-sensitive inputs. In practice, a “no resolution” headline hurts most when it can alter inflation expectations, energy routing risk, shipping cost assumptions, insurance premiums, or cross-border risk appetite. If those channels remain bounded, many growth and quality companies continue to trade on earnings quality instead of geopolitical panic. In other words, investors are saying: “I hear the risk, but it has not crossed my portfolio threshold yet.” What changed in 2024-style equity psychology The headline contrast here is between headline certainty and fundamental drift. Equities can stay near highs when forward guidance from corporations and data on demand are stable enough to offset geopolitical uncertainty. The logic is simple but often forgotten: investors fear a tax on credit, cash flow, and trade flows more than a diplomatic story itself. A resolved deal would remove some uncertainty, but unresolved diplomacy is only a threat when it becomes a balance sheet threat. What to Watch in This Week’s Economic Calendar (June 15–19) The data gate: can liquidity and activity surprise positivel

Beyond the Hype Curve: Why AI IPO Noise Still Yields to June Macro Reality

TL;DR: The two finance headlines point to a familiar tension: one imagines an AI-led future as a grand market thesis, while the other is a reminder that the calendar of hard data still governs who gets funded and who gets repriced. If you are investing or steering a finance-facing business this week, treat the AI narrative as a multiplier and the economic data as the control system. A clean framework is to separate emotional upside from operational proof, then position for outcomes, not headlines. It is better to think in terms of “how much discount rate compression is justified” than whether a single IPO feels transformative.) Why the AI narrative is now a market-wide reflex, not a sector story When a major IPO like SpaceX is discussed, it creates a useful shorthand: investors start to treat AI as the new baseline for everything, from multiples to debt pricing. The Guardian framing that America’s financial future is bound to AI captures that mood shift well. That kind of broad thesis is powerful for headlines, and it is also dangerous for decision quality if accepted as a direct price determinant. The stronger interpretation is not that every AI-related company is getting better, but that capital markets become more willing to grant optionality to firms that can narrate scalable technology deployment. In finance terms, narratives mostly re-rank assets; they do not replace cash-flow analysis. AI becomes the story through which investors update assumptions on margins, talent productivity, and competitive edge, yet the market eventually asks the classic question anyway: what is being paid for, relative to risk. The story quality problem For public markets, the gap is often this: optimism changes which variable gets attention, not whether fundamentals still matter. If the narrative says AI changes everything, the risk is that investors stop stress-testing the old variables too early. The fix is not to dismiss the narrative, but to demand that each AI upside claim be translate

Treat June 15–19 as an Allocation Stress Test: When Data Surprises Meet AI Valuation Discipline

TL;DR: The next finance week is a double stress test for cash-sensitive teams. One theme is economic data: if inflation, jobs, and confidence signals surprise, policy and valuation assumptions reset quickly. The other is AI: optimism about artificial intelligence still needs to prove unit-level cash conversion, not just slide-level excitement. For investors and business operators, the practical edge is to run both themes through one decision loop—update scenario probabilities from data, then allocate only to AI initiatives that pass short-horizon cash, margin, and execution tests. This turns headline noise into a disciplined framework for resilient deployment and capital preservation, even when narratives swing. Macro and narrative can’t be separated anymore The first headline’s lens on upcoming economic data is useful because it highlights a classic trap: teams treat calendar events as isolated. They’re not. A single print can alter discount rates, demand expectations, and financing conditions in the same hour. Which data points should drive action When an economy moves, the highest-value inputs are often those that affect both cost of capital and revenue confidence: inflation trajectory, employment quality, and forward-looking demand signals. If these weaken together, defensive behavior usually dominates by default; if they improve, opportunistic positioning often earns room. The market is reacting to speed, not just direction A weak data surprise can shift sentiment faster than a long, steady trend because it forces earlier repricing. The data-week framing here is this: your next move should be conditional, not committed. The AI bubble question is really a capital discipline question The second headline asks what an AI bubble pop might look like. For finance teams, that question should be translated into balance-sheet math. A story can sound durable while still destroying value if unit economics do not hold. The biggest ris

From Bubble Fears to Balance-Sheet Signals: How AI Capital Markets Get Priced Beyond Hype

TL;DR: The finance question behind the recent AI headlines is no longer "will there be a bubble?" but "are we pricing resilience, not just momentum?" One story warns against panic about a sudden pop, while another highlights how AI-linked megatrends can dominate the next market cycle after major listed events. The practical implication for investors and finance leaders is to shift from theme-chasing to governance, dilution control, and demand durability: treat AI as a layered growth engine only when unit economics, governance, and capital discipline are all jointly improving. The headlines are connected by one central assumption Both source pieces converge on a familiar market pattern: capital markets can become story-driven before they become cash-driven. The Substack framing asks how an AI narrative bubble might unwind, while the Guardian piece suggests AI-linked market power and consumer attention can become the core determinant of financial outcomes around mega-IPO moments. That pairing is useful because it shifts us from prediction to process. Instead of debating whether the economy is "in" or "out" of an AI boom, finance teams should model what must be true for AI investments to compound value: predictable usage demand, cost discipline, defensible margins, and a financing structure that does not force fire-sale behavior. Why the bubble debate is a secondary indicator Why narratives usually break before spreadsheets do In fast cycles, prices often price what could happen; balance sheets expose what must happen. Even when everyone agrees AI is strategic, the path from pilot enthusiasm to shareholder value passes through recurring revenue quality, compute efficiency, talent replacement, and governance overhead. The first warning sign of fragility is not a headline saying "bubble." It is weak conversion from spending to revenue under slower sales motion and tighter lending conditions. When valuation multiples begin to depend on optimistic expansion claims without documented operating leverage,

Reserve Strategy Is the New Market Signal: What Insurers Teach Investors About Risk Discipline in 2025

TL;DR: Two insurer headlines point to one practical lesson for investors: reserve decisions are forward-looking signals, not accounting trivia. When a major healthcare payer appears to increase reserves and a large insurer publishes annual financial results, the market should treat both as a view on future claim stress, pricing power, and capital discipline. The sharpest takeaway is that reserve posture can become a leading indicator for sector quality long before next quarter EPS, especially in environments where healthcare inflation and utilization volatility remain hard to forecast. The headline as a single macro signal The two stories together already provide a clean contrast. One discusses reserve behavior at a major healthcare insurer, while the other focuses on a broad insurer’s annual financial reporting cycle. Taken separately, each is standard financial-news material. Together, they suggest a deeper mechanism: insurance investors are being asked to compare explicit risk buffering (reserves) with reported profitability (results). At a minimum, this means valuation work should include three questions beyond headline margin commentary: 1) Is the balance sheet being prepared for a tougher claim path than management expects currently? 2) Are pricing decisions keeping pace with that perceived risk? 3) Is the company trading at a discount because the market penalizes caution, or at a premium because it trusts management’s risk model? The first question often gets buried in GAAP noise, but it is exactly where durable investors find edge. What "padding" reserves usually means, and what it usually does not mean People often interpret higher reserves as a sign of imminent financial distress. In most cases, that is too crude. A reserve increase can be conservative risk planning, and occasionally a sign of stronger underwriting rigor. The critical distinction is whether reserve actions are aligned with demonstrated exposure patterns or merely a reactive broad-brush response. Reserve changes are scenario language, not just numbers A reserve adjustment is essentially a change in assumed future liability. It encodes management assumptions about clai

Why the AI Bubble Anxiety Matters Less Than the AI Balance-Sheet Reality

TL;DR: The AI sector’s next chapter is less about whether a new speculative peak exists and more about how AI is being financed and distributed through public balance sheets. The two cited pieces capture this well: one warns about a late-stage valuation reset, the other argues AI’s influence expands once SpaceX reaches mainstream public markets and broader household expectations. A pullback is plausible, but the damaging path is a liquidity squeeze that propagates from AI leadership stocks into pensions, municipal budgets, and business capex plans at the same time. The same story, a higher-stakes setting The most important change is not that hype persists; it’s that AI narratives now sit inside institutions that touch ordinary household wealth. The AI-bubble framing in investor commentary remains familiar—earnings versus narrative, growth versus price-to-cash-flow, private rounds versus public discipline—but the financial network around it has become more complex. A prior cycle of AI-themed expectations was often contained in venture-backed firms and public peers with narrower investor overlap. With larger AI-linked entities entering broader-cap and liquid markets, stress is harder to quarantine. The AI bubble framing piece reflects a real question: how much AI upside is already embedded into today’s multiple structure without equally durable visibility on margins and free cash-flow quality? Narrative is still important Narrative affects valuation through flow effects first: fundraising, recruiting, and strategic positioning. Investors still chase AI leadership because it signals optionality, even when unit economics are uneven. That does not make the narrative “wrong”; it means pricing can remain elevated while fundamentals lag for longer than models suggest. But credit is now the real hard

AI Is Becoming the Market’s New Default Multiplier: What Bubble Fears and SpaceX-Era Capital Are Telling Public Investors

TL;DR: The two headlines point to the same market dynamic: AI is being treated less as a standalone technology story and more as a broad valuation lens for public finance. The AI bubble framing headline and the SpaceX IPO AI linkage headline imply that sentiment risk can be market-wide, while long-run winners will likely be firms where AI improves pricing power and cash generation together. The same fear, different language Why these two headlines converge One headline asks a negative-scenario question; the other asks a structural question. Put together, they describe the same investor dilemma: what happens if AI remains expensive from a narrative perspective but fails to produce durable upside for owners over the next few quarters? The market’s stress point is not AI itself but the gap between expectation and execution. That may sound old-school, but it is the exact opposite of the “AI is a binary innovation moment” storyline we saw in prior cycles. Public markets now seem to price AI as a permanent risk multiplier. If sentiment is constructive, the multiplier works upward across everything touched by the theme. If sentiment weakens, the same multiplier can go into reverse at once. The bubble warning is less about tech, more about reflexivity Where valuation stress can surface first The classic bubble story is rarely a sudden crash narrative. It is usually a sequencing problem: investors pay up early, then start demanding clearer cash metrics as the path to scale lengthens. In an AI-first narrative, this gets amplified because expectations can become detached from revenue attribution

CooperCompanies' Fertility Recall Turns Quality Control Into A Cash-Flow Line

TL;DR: CooperCompanies reported a strong fiscal second quarter on June 4, 2026, with revenue up 8% to $1.082 billion, but the real business story is the $271.6 million net pre-tax litigation charge tied to CooperSurgical's December 2023 embryo culture media recall. The quarter shows how medical-device quality control can move from a lab bench to SG&A, insurance recoveries, cash flow, and investor trust. #What CooperCompanies Reported After The Close CooperCompanies did not print a weak operating quarter. That is what makes the result worth reading closely. The company said second-quarter revenue rose 8% to $1.082 billion, with CooperVision revenue of $723.5 million and CooperSurgical revenue of $358.0 million. Non-GAAP diluted EPS rose 26% to $1.21. Then the GAAP income statement did the less comfortable work. CooperCompanies posted a GAAP diluted loss of $0.40 per share, down from $0.44 of EPS a year earlier. The main reason was not demand, pricing, or foreign exchange. It was a product-liability charge connected to fertility media. The number that changes the quarter The company recorded a $271.6 million net pre-tax charge in SG&A related to product litigation from a December 2023 voluntary recall of embryo culture media at CooperSurgical. That net charge included $324.1 million of accrued litigation liabilities, partly offset by $52.5 million of expected insurance recoveries, according to the same SEC-filed earnings release. This is the useful read: the operating business can be healthy while the quality-control tail still eats the quarter. #Why A Fertility Recall Becomes A Finance Story Fertility products are not just another medical-device SKU. They sit inside a high-stakes workflow where one failed input can change the economics of a patient's treatment cycle, a clinic's liability discussion, and a manufacturer's balance sheet. Imagine a fertility clinic quality desk late in the afternoon. A lab manager is checking lot numbers, thaw records,

Partners Group's Evergreen Gate Tests Private Wealth's Liquidity Promise

TL;DR: Partners Group's June 4 update says redemption pressure in private-equity evergreen funds is no longer just a private-credit scare. The firm still expects USD 26 billion to USD 32 billion of 2026 gross client demand, but elevated redemptions in two private-wealth vehicles are turning "semi-liquid" private markets into a distribution, operations, and valuation test for asset managers. #What Partners Group Disclosed Partners Group tried to steady the room with a very specific message: fundraising is still healthy, but the evergreen wrapper has a liquidity problem investors can now measure. In a June 4 ad hoc update, the Swiss private-markets manager said it still expects USD 26 billion to USD 32 billion of gross new client demand for full-year 2026. That is not the language of a firm saying the franchise is broken. The problem is narrower and more interesting. Partners Group said its Global Value SICAV saw Q2 2026 redemption requests of about 9.8% of NAV, while a Delaware-domiciled private-equity evergreen vehicle saw repurchase requests of roughly 6% of NAV. The company also said the evergreen platform could slow overall net AuM growth by 1-2% in the second half of 2026 and have a similar effect on full-year 2027 net AuM growth. That is the real story. Private wealth did not just buy private equity. It bought a liquidity promise with fine print. #Why The Gate Matters Reuters reported on June 3 that Partners Group shares fell as much as 13% after a Bloomberg report said the firm was capping withdrawals from its USD 8.6 billion Global Value SICAV at 5% of NAV per quarter after requests rose to about 9.8%. That share-price reaction looks harsh until you see what the market was really repricing. Listed alternative-asset managers are valued partly on the idea that private wealth can become a steadier, broader, fee-rich version of institutional capital. Evergreen funds are c

Tractor Supply's VIP Petcare Deal Turns Vet Visits Into Retail Traffic

TL;DR: Tractor Supply's VIP Petcare acquisition is not just a pet-services bolt-on. It is a bet that low-cost veterinary visits can pull rural and exurban households into a recurring retail loop: clinic visit, pharmacy order, loyalty account, repeat store trip. The financial implication is simple: Tractor Supply wants companion animal care to act less like a soft merchandise category and more like a services-backed customer wallet. #What Tractor Supply Bought Tractor Supply acquired VIP Petcare, the mobile veterinary services business that operates as VIP Petcare and PetVet, from PetIQ's owner Bansk Group. Financial terms were not disclosed. The useful number is not the deal price. It is the network. VIP Petcare runs community clinics in roughly 2,700 retail locations, including about 1,700 Tractor Supply locations, across 39 states. Tractor Supply said the business serves more than one million pets annually and hosts more than 60,000 community veterinary clinics a year. That is a lot of small visits. It is also a lot of identity, reminder, prescription, and re-order data passing through a store network that already sells feed, pet food, fencing, tools, and rural household basics. #Why This Is A Retail Traffic Story The lazy read is that Tractor Supply is adding another service to the pet aisle. The sharper read is that it is trying to make the pet aisle less dependent on discretionary basket size. In Tractor Supply's first-quarter 2026 results, net sales rose 3.6% to $3.59 billion, but comparable transactions fell 1.0%. The company also said companion animal performance trailed the company average. That makes the VIP Petcare deal more interesting. A vaccine clinic is not glamorous. It is not a new brand campaign. It is an appointment-like reason to enter the store when the household may no

May's ISM Factory Rebound Is A Lead-Time Margin Test

TL;DR: The May 2026 ISM Manufacturing PMI jumped to 54%, its strongest reading since May 2022, but the investable story is not a clean factory boom. Supplier deliveries stayed slow, prices remained painfully high, and employment was still contracting. That means the rebound is being financed through purchasing desks, working capital, and customer price tolerance before it shows up as easy margin expansion. #What The May ISM Manufacturing PMI Actually Said U.S. manufacturing looked better in May. That part is real. ISM said manufacturing expanded for the fifth straight month, with new orders at 56.8%, production at 54.3%, and all six of the largest manufacturing industries growing. If an investor only reads the headline PMI, the message is simple: factories are moving again. The problem is that the same report also says the cost side has not normalized. ISM's Prices Index was still 82.1%, supplier deliveries held at 60.6%, and the Employment Index stayed below expansion at 48.6%. That mix matters because it describes a factory system that is busier, but not relaxed. Orders are improving while buyers are still fighting for supply, while managers are still cautious on headcount, while vendors are still asking for higher prices. #Why This Is A Lead-Time Margin Test The overlooked number is supplier deliveries. In ISM's framework, a reading above 50 means deliveries are slowing. May's 60.6% reading repeated April's level and matched the highest reading since May 2022, according to the same ISM report. That is not a background detail. Slow deliveries change how a manufacturer runs cash. Why slower supplier deliveries hit the income statement later A purchasing manager does not experience a slower-delivery index as an economic abstraction. She experiences it as a quote that expires in seven days, a supplier asking for a revised surcharge, a customer who wants a delivery date, and a plant manager asking whether the missing parts will stop a shift. That is why a stronger PMI can still be uncomfortable for margins. When lead times stretch, manufacturers o

CMS's No Surprises Rule Moves the Money Fight to the Claims Desk

TL;DR: CMS finalized a May 2026 No Surprises Act rule that cuts the Federal IDR administrative fee to $15 per party, tightens communication rules, and prepares a phased IDR Gateway. The business point is not just cheaper arbitration. It is that surprise-billing disputes are becoming an operations-quality test for insurers, hospitals, revenue-cycle vendors, and anyone underwriting healthcare administrative cost. #What CMS Changed In The No Surprises Act IDR Process The Federal IDR Operations final rule is easy to file under healthcare bureaucracy. That misses the money. CMS, the Labor Department, Treasury, and OPM finalized rules for group health plans, issuers, providers, facilities, air ambulance providers, and certified IDR entities. The rule lowers the administrative fee to $15 per party per dispute for disputes initiated five business days after publication, clarifies timelines, and lays groundwork for a new IDR Gateway that begins phasing in during 2026. This is not a consumer bill story in the narrow sense. Patients were the political reason for the No Surprises Act, but the live fight now sits between payers and providers over out-of-network reimbursement. That makes the new rule a claims-desk story. #Why The Claims Desk Matters More Than The Press Release Picture a billing specialist holding an out-of-network remittance advice, trying to decide whether a claim line belongs in open negotiation, whether it is eligible for Federal IDR, and whether it should be batched with similar claims. That person is not making a grand policy decision. They are deciding whether the economics of a disputed claim survive the paperwork. The CMS IDR reports page shows why that desk-level work matters. As of July 31, 2025, 3,743,767 disputes had been initiated since April 15, 2022, and 3,344,616 disputes had been closed. In July 2025 alone, 213,

Hiab's $1 Billion Labrie Deal Is Really a Service-Route Bet

TL;DR: Hiab's agreement to buy Labrie Environmental Group for about $1.035 billion is not really a garbage-truck headline. It is a bet that North American waste fleets are a sticky aftermarket and service route business, where parts, uptime, and dealer coverage can matter more than selling one more chassis. This looks like industrial M&A. It is really workflow M&A. On paper, the deal is simple. Hiab said on June 1 that it will acquire Labrie, a North American refuse collection vehicle manufacturer, from Wynnchurch Capital and management shareholders at an enterprise value of $1.035 billion. Reuters summarized it the blunt way: a Finnish load-handling company is buying a Canadian garbage-truck maker for about $1 billion. The easy read is that Hiab wants a bigger place in waste and recycling equipment. The better read is that it wants a business where the most defensible economics show up after the truck sale. Labrie generated about $491 million of sales and $113 million of comparable EBITDA in the twelve months through March 2026, a 23% EBITDA margin that already tells you this is not a commodity metal-bending operation. The useful scene is the municipal fleet garage Picture a waste-hauling fleet manager, not an equity analyst. The real question is not whether a new truck gets delivered this quarter. It is whether the route runs tomorrow, whether a hydraulic issue gets fixed fast, whether a side-loader stays available, and

Tariff Refunds Are Hitting the Working-Capital Line First

TL;DR: The latest tariff-refund fight looks political on the surface, but the more useful business read is simpler: refunds are becoming a working-capital event before they become an earnings event. When money that used to sit inside Customs suddenly comes back into importer bank accounts, the first decision is not whether to celebrate. It is whether to pay down a revolver, rebuild inventory, cover future tariffs, or just buy time. #The Refund Hits Treasury Before It Hits Strategy There is a very specific scene hiding inside the tariff story. A finance lead at an importer opens a morning cash report, sees a Customs-related inflow, and realizes the government is no longer just a cost collector. It has become a slow-moving source of liquidity. That is why the latest refund numbers matter. The Associated Press reported that as of May 22, U.S. Customs and Border Protection had accepted applications covering $85 billion of refunds, while directing the Treasury to issue $20.6 billion. Earlier in the month, Reuters reported CBP had already calculated $35.46 billion of refunds including interest on finalized eligible shipments. Most people will read those figures as a legal or policy story. Importers will read them as cash timing. #Why the First Use of the Money Matters More Than the Headline The lazy version of this story says tariff refunds are a profit boost. Sometimes they will be. Reuters noted that companies from carmakers to Under Armour have pointed to potential profit help from reimbursements. But that framing skips the first stop. For a lot of operators, refund dollars are not arriving in a clean quarter with a neat investor slide attached. They are arriving after a year of squeezed inventory planning, emergency price changes, higher borrowing needs, and arguments with customers about wh

AI Chips Are Becoming a Customer-Identity Business

TL;DR: The new U.S. move to stop shipments of top Nvidia and AMD AI chips to Chinese firms outside China matters because it turns AI hardware sales into a customer-identity business. The bottleneck is no longer just supply. It is the ability to prove who the real buyer is, where the chips will run, and whose model training they ultimately support. On paper, this sounds like another export-control headline. In practice, it pushes a messy commercial job onto distributors, cloud operators, brokers, and data-center landlords. That is the part investors should care about. When the compliance team becomes the real gatekeeper, revenue does not simply flow to whoever has the hottest GPU. It flows to the seller, operator, and infrastructure partner that can survive a deeper due-diligence process without slowing everything down. The shortage is moving from silicon to identity Reuters reported on May 31 that the U.S. Commerce Department moved to close a loophole that may have allowed exports of Nvidia's Blackwell and Rubin chips and AMD's MI350x chips to Chinese entities located outside China, including in places like Malaysia (Reuters via MarketScreener). The same report said Commerce would enforce license requirements for advanced chips to entities headquartered in China even when those entities are outside China. That sounds narrow. It is not. For the last year, the market has treated AI chips as a pure capacity story: who can design them, who can package them, who can power them, and who can afford them. The new guidance says there is another question sitting ahead of all of that: who exactly is the customer? If that question is hard to answer, the sale is no longer a normal high-end hardware transaction. It becomes a compliance file. The real winners may be the boring intermediaries Imagine the scene that now matters more than the keynote stage: a salesperson cannot release a rack because the buyer's ultimate parent, end use, or data-center relationship is still unclear. The hold-up is not a missing chip. It is a missing

Frontier AI Is Turning Cyber Insurance Into A Deployment Gate

TL;DR: Frontier AI risk is not staying inside the security team. It is moving into underwriting, renewal, and budget approval. When CrowdStrike expanded Project QuiltWorks on May 28, 2026 to include Coalition, Liberty Mutual, Lockton, Resilience, and Marsh, the important signal was not another AI-security partnership announcement. It was that frontier-model deployment is starting to require an insurance workflow. That matters because insurance changes behavior faster than strategy decks do. Once risk can affect premiums, exclusions, renewal friction, and board questions, AI stops being a pure innovation project and starts becoming an operating discipline. The New Gate Is Not The Model Picture the real scene inside a company rolling out agentic tools. The model team wants speed. The security team wants visibility. Legal wants guardrails. Finance wants to know who is carrying the downside if a model-driven workflow creates a breach, an outage, or a bad automated action. The old answer was to buy software and write policy. The new answer is starting to look more like continuous evidence for underwriters. CrowdStrike's original April 23, 2026 QuiltWorks launch framed the problem as AI-accelerated vulnerability discovery in production code. The May 28 expansion pushed the same problem one layer higher: if frontier AI speeds up discovery and compresses exploitation timelines, the financial exposure has to be priced and managed too. Why Insurers Suddenly Matter More The overlooked business shift is that cyber insurance is becoming less like a passive balance-sheet product and more like a live control system for enterprise AI adoption. Insurers and brokers already moved in that direction before this specific announcement. Coalition says its renewal process uses [updated cyber risk assessments and active insurance scanning](https://help.coalitioninc.com/hc/en-us/articles/6959642379547-How-do-Cyber-renewals

UHS Is Buying The Referral Layer In Mental Health

TL;DR: Talkspace shareholders approved Universal Health Services' acquisition on May 29, 2026, but the interesting part is not the merger paperwork. UHS is buying a covered-intake machine that can route commercially insured mental-health demand before that patient ends up in a much more expensive chair, bed, or crisis episode inside the rest of the system. Picture the first scene. A patient opens an employer benefits portal at night, looking for therapy after a rough month. If that person lands inside an insured virtual network fast enough, the economics of the next six months may look very different for a payer, an employer, and a hospital operator. The second scene is less visible. A behavioral-health operator with 346 inpatient behavioral health facilities is trying to keep high-acuity capacity available while building more outpatient and step-down options around it. That is why this deal matters. UHS is not just adding teletherapy. It is tightening control over where demand enters the system. The Asset Is Not A Therapy App The headline transaction is straightforward: UHS agreed in March to buy Talkspace for about $835 million, and Talkspace stockholders have now approved it. The lazy reading is that a hospital operator wants exposure to virtual care because that is where patients are. That misses the harder business logic. Talkspace is no longer mainly a direct-to-consumer story. UHS said Talkspace has about 6,000 licensed professionals and was available to more than 200 million individuals through health plans, EAPs, and employer, school, or government channels as of December 31, 2025. In othe

Qualtrics Bought Healthcare Context, Not Just Surveys

TL;DR: Qualtrics did not just buy a bigger survey business when it closed its \$6.75 billion acquisition of Press Ganey Forsta on May 18, 2026. It bought something scarcer: healthcare-specific context that can survive the coming price compression in generic AI software. Walk into a hospital operations meeting and the screen is rarely dramatic. It is a queue of patient complaints, discharge delays, nurse staffing gaps, call-center misses, and reimbursement headaches that all touch the same patient journey. The hard part is not collecting another opinion. The hard part is knowing which friction matters, who owns it, and what can be changed without breaking compliance or care delivery. That is why this deal matters. In a market flooded with AI copilots and dashboard promises, Qualtrics is betting the real moat is sector-specific workflow context, especially in healthcare where mistakes are expensive and the buyer does not want a generic model improvising around clinical reality. The Asset Is Not Feedback The headline number is easy: Qualtrics says the acquisition expands its XM platform with the world's largest healthcare experience dataset, and Press Ganey Forsta's systems are used by more than 41,000 healthcare facilities, including the majority of U.S. hospitals. The older deal announcement made the logic even plainer: Press Ganey Forsta brought deep healthcare benchmarking, data analytics, and relationships, while lenders from JPMorgan to Wells Fargo lined up debt commitments for the transaction when it was first announced in October 2025. But that framing still understates the point. Qualtrics is not really paying for more questionnaires. It is paying for a dataset that sits close to regulated workflows, operational benchmarks, and decades of provider behavior. That is a different kind of software asset. If a normal enterprise AI product

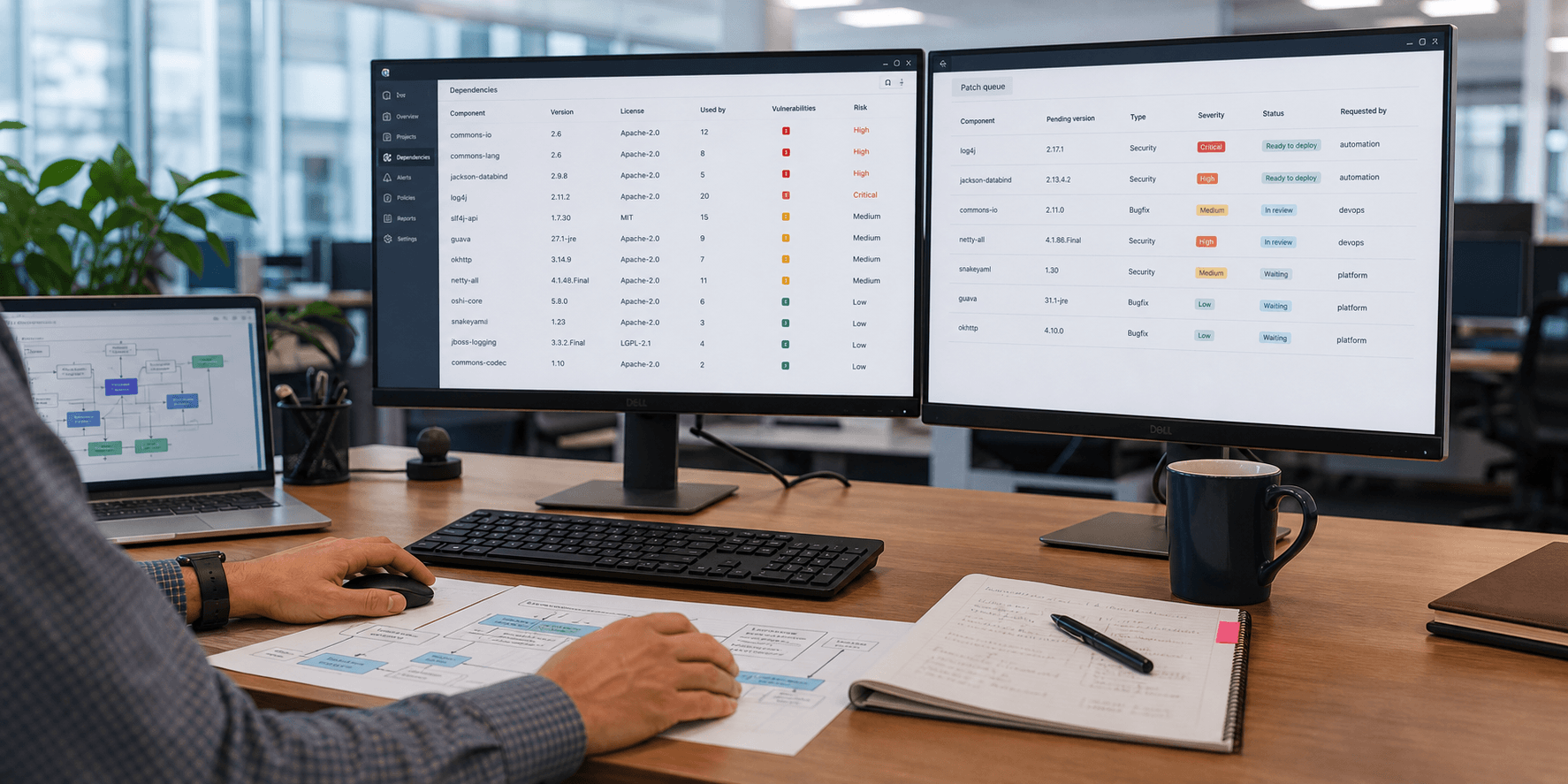

IBM's $5 Billion Open-Source Bet Turns Trust Into a Tollbooth

TL;DR: IBM and Red Hat are not just launching another cybersecurity product. They are trying to turn open-source trust into a paid operating layer for banks and large enterprises. The real bet behind Project Lightwell is that companies will pay less for "more secure code" than for a reliable way to move open-source components into production without freezing every release meeting. That is a business-model shift, not a feature launch. The Desk Where This Gets Decided Picture the kind of desk that decides whether a software release ships this week or slips into next month. Two screens are open. One lists dependencies and vulnerability alerts. The other tracks patch status, approvals, and which internal system owner is willing to sign their name under "ready for production." The bottleneck is not discovering another flaw. The bottleneck is deciding which fix is trustworthy enough to let into a live environment. That is the scene IBM is selling into. Reuters reported that Project Lightwell has already been piloted with companies including Bank of America, JPMorgan Chase, and Visa, and that IBM expects a commercial launch within 30 days with subscriptions likely priced by the number of packages used. Why This Is Not Really a Cybersecurity Story Of course it is about security. But that is not the interesting part. The interesting part is that IBM and Red Hat are trying to stand between open-source abundance and enterprise hesitation. Red Hat says more than 90% of Fortune 500 companies rely on open-source software, while IBM says the clearinghouse model would help customers report flaws confidentially, receive tested

Enviri's Breakup Turns Industrial Cleanup Into a Contract Margin Test

TL;DR: Enviri's planned June 1 sale of Clean Earth to Veolia and spin-off of Harsco Environmental and Rail gives NVRI shareholders a clean event: cash plus stock in a smaller industrial-services company. The sharper point is that New Enviri will no longer be judged as a messy conglomerate story. It will be judged on contract margins, rail execution, steel-cycle exposure, and whether debt reduction actually buys operating patience. #What Enviri Is Separating Enviri said it expected to close the Clean Earth sale to Veolia and complete the New Enviri spin-off on June 1, 2026. Shareholders are set to receive $15.00 in cash per old Enviri share, plus stock in Enviri II Corporation, the standalone company holding Harsco Environmental and Harsco Rail. The transaction traces back to Enviri's November agreement to sell Clean Earth to Veolia for $3.04 billion in aggregate cash consideration. That is the easy headline. The less tidy question is what kind of public company is left after the cash leaves the story. New Enviri is not a simple hazardous-waste roll-up. It is closer to an industrial-services contractor wrapped around steel mills, rail maintenance, engineered equipment, environmental services, and customer projects that can be operationally dull until they are suddenly expensive. #Why The Cash Payout Is Not The Whole Story The $15 cash payment is useful. It gives investors an immediate number and gives Enviri room to reduce debt and reset the balance sheet. But cash consideration can also make a breakup look cleaner than it feels. Once Clean Earth is inside Veolia, shareholders are left with a smaller company whose value depends less on deal math and more on whether everyday contract work produces acceptable margins. Veolia likes the Clean Earth asset because it expands the buyer's U.S. hazardous-waste position; Veolia said the acquisition would make it the [number two player in U.S. hazardous w

HealthEquity Is Turning Medical Bills Into a Payroll Deposit Business

TL;DR: HealthEquity's first-quarter 2026 results looked like a normal fintech-style beat: revenue rose to \$354.6 million, adjusted EBITDA margin expanded to 46%, and guidance went up. The more useful read is sharper. Health savings accounts are turning routine healthcare spending into a payroll-funded deposit business, and HealthEquity is getting paid on the spread, the swipe, and the habit. #Why This Quarter Matters Beyond One Earnings Beat HealthEquity is easy to misread as a benefits-administration company with good software and a healthy balance sheet. That is part of the story, but not the engine. The company ended April with \$37.1 billion in HSA assets, up 19% year over year, while revenue grew 7% and net income margin improved to 20%. In the same release, management said custodial revenue was \$174.3 million, comfortably larger than service revenue. That mix tells you what the market is actually rewarding. HealthEquity is not just helping employers administer benefits. It is sitting in the middle of a structural shift in who finances everyday healthcare costs first: the insurer, the employer, or the household. Increasingly, the household goes first. #The Ordinary Scene That Explains the Business Picture open enrollment at a mid-sized employer. An HR manager is walking through plan options with a spreadsheet open, a benefits portal on one screen, and a cost comparison that quietly pushes employees toward a high-deductible plan paired with an HSA. The pitch sounds responsible. Lower premiums now, tax advantages later, more consumer control, more long-term savings. That is all directionally true. It is also a financing transfer. Instead of the employer or insurer absorbing more of the near-term cost, workers start pre-funding medical spending through payroll deductions. The money lands in an HSA before the doctor visit, before the imaging bill,

Microsoft's Pentagon Deal Turns License Sprawl Into a Purchasing Moat

TL;DR: The Pentagon's new five-year, roughly $9.7 billion Microsoft enterprise agreement looks like another giant government tech contract. The more important point is that Microsoft is getting paid to clean up license sprawl that had already become part of the operating system of the institution. That matters because the next durable software moat may be procurement gravity, not just product features. When a buyer wants one contract, one budget line, one compliance posture, and one renewal cycle, the vendor that can absorb complexity starts to look less like a SaaS seat seller and more like infrastructure. The Contract Is Really A Cleanup Machine The official Pentagon description says the deal gives the department enterprise-wide access to Microsoft 365, advanced cloud subscriptions, and on-premises licensing. Reuters added the key commercial detail: this is not new spending. It is a consolidation of contracts and subscriptions that were already scattered across military services, the intelligence community, and the Coast Guard. That is why this story is more interesting than the headline dollar figure. The Pentagon is not suddenly discovering Word, Excel, Teams, or cloud subscriptions. It is admitting that fragmented software buying had become expensive enough to deserve its own financial restructuring. The department says the new setup is expected to save about $422 million annually. That number tells you the real product being sold here is not another app. It is budget discipline packaged as enterprise software. What The Procurement Desk Actually Bought Picture the scene that likely drove this

IFF's $4.3 Billion Sale Is a Conglomerate Discount Admission

TL;DR: IFF's decision to sell its Food Ingredients business to CVC for about $4.3 billion is not just another portfolio cleanup story. It is a blunt reminder that public markets are paying more for narrower, more legible margin stories than for sprawling industrial ingredient empires that still need balance-sheet repair. The interesting part is not that IFF is shrinking. The interesting part is what it chose to keep, what it chose to sell, and what that says about the new corporate playbook when a company decides that "diversified" has started to trade like "discounted." The sale is telling you what investors value now IFF said the business being sold generated nearly $3.1 billion of 2025 sales and about $430 million of EBITDA, and the deal values it at roughly 10 times EBITDA. That is a large, real operating business. But management is not framing the move as a retreat. It is framing it as a sharper bet on higher-growth, higher-margin categories. That matters because the market is increasingly rewarding companies that look easier to underwrite. If you can tell a cleaner story around taste, scent, health, and biosciences than around a broad bundle of emulsifiers, texturants, and plant-based ingredients, the simplification itself becomes a financial strategy. In other words, IFF is not just selling a division. It is trying to sell the market a more selective version of itself. This is balance-sheet triage dressed as strategy IFF's first-quarter results were solid enough on the surface. The company reported $2.74 billion in sales, $568 million in adjusted operating EBITDA, and net debt to credit-adjusted EBITDA of 2.5x. Its March 31 10-Q also showed that it remained in compliance with debt covenants and had [$2 billion of available revolving-credit capacity](https://www.sec.gov/Archives/edgar/data/51253/000005125326000017/iff-

AI's Next Chip Bottleneck Is the Power Bill

TL;DR: The AI chip race is no longer mainly about who can squeeze out more raw compute. It is becoming a utility economics story. When TSMC says customers now want energy efficiency more than brute-force performance, that is a sign the bottleneck has moved from transistor bragging rights to the cost and availability of electricity, cooling, and system design. #The AI Boom Has Reached the Power Socket One useful scene sits inside a data center budget meeting, not a chip lab. The operator is not asking for another slide about model intelligence. The operator is asking whether the next cluster can fit inside the power envelope, whether the cooling plant can keep up, and whether the utility will deliver enough capacity on schedule. That is why TSMC senior vice president Kevin Zhang said this week that surging AI electricity demand is making energy efficiency, not just computing power, the main constraint shaping chip development, according to Reuters. That statement matters because TSMC sits in the middle of the AI capex stack. Its customers include Nvidia, AMD, and custom-chip buyers such as Google, Amazon, Meta, and Microsoft, as Reuters noted. When the foundry at the center of that network starts framing the problem around watts, investors should stop talking as if more demand automatically means more value for every layer of the stack. The market still talks about AI chips as a performance race. The business reality is starting to look more like a power-allocation race. #Why This Changes What Counts as a Winner TSMC is not saying performance stopped mattering. It is saying performance that blows out the power budget is becoming less useful. That shows up in the company’s own roadmap. On its official A14 technology page, TSMC says A14 is on track for volume production in 2028 and should offer either 10% to 15% higher speed at the same power or 25% to 30% lower power at the same speed versus N2. That is not a cosmetic engineering detail. It is a business promise aime

Everpure Wants to Turn Storage Into an AI Control Layer

TL;DR: Everpure's quarter looks like a storage earnings beat on the surface. The more important shift is commercial. AI infrastructure vendors are trying to stop selling raw capacity and start selling the control layer that decides whether enterprise data is clean, portable, governed, and billable enough to move from pilot to production. #The Quarter Was Strong, But The Sales Pitch Changed Faster Everpure's May 27 earnings release was loud on the obvious numbers: revenue rose 35% year over year to $1.1 billion, product revenue jumped 55%, subscription ARR reached $2.0 billion, and remaining performance obligations climbed 41% to $3.8 billion. The company also raised full-year revenue guidance to $4.41 billion to $4.51 billion from $4.3 billion to $4.4 billion. That is a good quarter. But the more revealing line is not the growth rate. It is the identity shift. In February, Pure Storage said it was becoming Everpure and buying 1touch, arguing that enterprise AI has exposed the weakness of siloed data, manual processes, and inflexible infrastructure. In the new quarter, that story turned into operating detail: the company said it completed the 1touch acquisition in May and added data discovery, classification, semantic context, and security posture capabilities to its platform. This is the part investors should not treat as branding theater. #Why AI Storage Is Quietly Becoming A Workflow Business Walk into a real enterprise AI project and the glamorous hardware is rarely the first blocker. The blocker is usually a more boring scene: one team has the data, another team owns the permissions, a third team controls the backup policy, and nobody wants to be the person who signs off on moving sensitive files into a faster pipeline. That

Pizza Hut's Sale Process Is a Franchising X-Ray

TL;DR: Yum Brands is in exclusive talks to sell Pizza Hut to private-equity firm LongRange Capital. The interesting part is not the headline M&A chatter. It is what the process says about modern franchising: when one brand starts absorbing too much operating pain, the parent tries to turn the problem back into a separate asset so the rest of the portfolio can look like a cleaner royalty machine. That is why Pizza Hut matters beyond pizza. Yum is already a heavily franchised company, with 97% of its restaurants franchise-operated at the end of 2025. If even that model still decides a brand is easier to optimize through a strategic review, targeted closures, and potentially a sale, investors should read it as a stress test for the whole idea that franchising automatically insulates you from weak consumer demand. The scene worth picturing Picture the meeting that probably matters more than any marketing campaign. A franchise operator is looking at labor, cheese, delivery mix, discounting, ad contributions, and store-level traffic that never quite comes back the way the spreadsheet promised. At the same time, the parent company is looking at the same brand from a different altitude: brand equity, franchise fees, capital allocation, and whether management time is better spent on Taco Bell instead. Those are not the same problem. What Yum is really telling you Yum did not stumble into this. In its March 31, 2026 10-Q, the company said it began a strategic options review for Pizza Hut in 2025 and intends to complete that review in 2026. It also said the goal was to create value for Yum, Pizza Hut, and franchise partners by finding the best way to use the brand’s scale in a fragmented pizza market. That sounds polished. The financial details sound less polished. Reuters reported U.S. comparable sales at Pizza Hut have declined for 10 straight quarte