Follows macro policy, credit markets, and earnings quality with a focus on what long-term investors should watch next.

Beyond Record Highs and Diplomacy: Using June 15–19 Data to Test Whether Equities Stay Complacent

TL;DR: These two headlines describe a market that is not denying risk, but pricing it differently: one piece emphasizes an upcoming economic calendar, the other asks why equities can still sit near record highs without a near-term Iran diplomatic reset. For finance and business readers, the practical insight is that the week’s edge is procedural. Translate each data and policy signal into trigger rules before the market moves, so risk is managed by process, not by narrative certainty. Why these two headlines should be read together The two stories are complementary rather than contradictory. A data-first lens says near-term price action is often shaped by what is released, not what is rumored. A markets lens says record levels can persist even when headline geostrategic uncertainty remains. Together, they imply a key regime: the tape is rewarding resilience in the macro signal chain while demanding proof of reversal when expectations shift. The practical read is simple: don’t confuse short-term calm with long-term resolution. Calm in price can coexist with unresolved risk if flows, liquidity, and corporate earnings visibility still hold. That’s why one publication tracks the week’s economic sequence while another asks the exact same risk-management question from a geopolitical angle. Why "no Iran resolution" is not automatically a bearish signal Investors often treat unresolved diplomacy as a binary input: either solved (good) or unsolved (bad). In practice, markets often treat it as a volatility input with a threshold-based impact. This is why stocks can remain stable: not because the issue is irrelevant, but because it is not yet a first-order shock. Uncertainty becomes meaningful when it starts crossing three concrete channels at once: policy reaction expectations, trade/energy cost assumptions, and demand confidence. [J.P. Morgan’s framing](https://news.google.com/rss/articles/CBMizgFBVV95cUxNQ3o0YTF6TDN4XzFLLXRCOFFJelJRWjBiY1dRV0hiZXI3NUdnVm5zcVRibDNrODd2UjFLTDhieExrVFZaUE1rUWdYZlZjVU1wbW40ZENodDQ2c

Calendar Supremacy: How Record Markets Price Data Rhythm Over Geopolitical Silence

TL;DR: The most useful story in this week’s markets is not a single catalyst but a sequencing problem: price discovery is being driven by the near-term economic print calendar and the technical resilience of earnings narratives. In that setting, “no Iran resolution” is becoming a temporary background fact, not a missing trigger. For investors and finance teams, the edge is to separate what matters this week from what is already priced in, then allocate liquidity only after fresh data confirms or denies your thesis. The hidden driver this week: sequencing beats headlines Why markets are trading on rhythm, not rhetoric The two source clues are enough to map a central tension: next week is an economic-data week, while markets are simultaneously dealing with unresolved geopolitics. The practical signal is that traders are choosing the one that is measurable over the one that is narratively loud. Kiplinger’s June 15-19 data watch framing is effectively a map of what can move valuations quickly. The second clue, J.P. Morgan’s framing around record highs without an Iran resolution, says markets are not denying risk—they are assigning it a lower immediate probability than the data stream behind them suggests. This distinction matters for finance professionals, especially treasury desks, CFOs, and portfolio managers who need to decide when a “headline event” is now versus “expected event” for earnings, funding, and inventory planning. For many teams, this is why risk committees have moved from macro fear narratives to data gates: each publication, payroll beat, or inflation print is treated as either confirmatory or destabilizing. Portfolio implication for now When risk is being repriced through a short sequence of known events, the right response is often boring: keep directional exposure sm

When Geopolitics Stalls, Markets Price the Data: Why Equities Can Stay Elevated Without an Iran Deal

TL;DR: The takeaway from these two headlines is not that geopolitics has become irrelevant, but that its effect is being repriced. If markets are already discounting a stable or at least manageable worst-case path, unresolved issues—such as the Iran settlement question—can coexist with record asset prices. In that regime, investors start rotating from headline fear toward macro data as the immediate governor of risk, especially when the next week contains a concentrated set of economic signals that can quickly alter interest-rate and earnings expectations. Why record highs can coexist with unresolved geopolitical friction The first headline, focused on the June 15-19 economic calendar, frames a familiar but often overlooked truth: in modern markets, timing matters as much as narrative. If decision-makers can anchor on a schedule of verifiable information, they become less reactive to single headlines and more process-driven. The second headline signals the market posture directly: equities can hold record levels even when a diplomatic path remains uncertain. That is not a contradiction. It usually reflects an internal risk reclassification: Geopolitical risk is still present and priced, but The incremental shock from “no new development today” is smaller than the uncertainty already built into expectations. In practice, that means asset prices can stay high if cash-flow outlooks, liquidity conditions, and policy expectations are not being materially disrupted in the near term. What to watch in the June 15-19 calendar before changing your stance The most useful takeaway from a weekly checklist is not just what events occur, but how fast the repricing happens once they are released. A major reason investors tolerate unresolved headlines is that they are waiting for hard data to confirm either resilience or fragility. Which data points usually matter most first For equity risk, investors usually triage macro data into three buckets: 1) Inflation trajectory signals (pricing and duration sensitivity), 2) Growth durability signals (earnings visibility), and 3) Financial-condition signals (credit and funding stress). Only when at least

Why Equities Stay Elevated as Geopolitics Stall: The Data-Dependency That Keeps Prices Supported

TL;DR: The current setup is not a contradiction but a pricing sequence: markets sit near records because investors are already treating unresolved diplomacy as a manageable policy backdrop while waiting on fresh U.S. data to change the valuation equation. In this week’s environment, the actionable edge is to monitor which data points re-anchor discount rates, earnings expectations, and liquidity conditions. If jobs, inflation, and credit internals stay stable, risk assets can absorb geopolitical stalling; a surprise in one of those channels can shift the tone faster than any headline statement. Beyond the Headline Paradox The story this week is not “optimism despite conflict,” but “uncertainty already embedded.” The first headline says investors should watch economic data closely across the coming week, while the second highlights stock strength even without a geopolitical settlement. Put together, it suggests the market is behaving in a very specific way: it is trading a probability-adjusted path, not a binary outcome. Why records can coexist with unresolved risk In finance, a record index is rarely a statement about peace; it is often a statement about cash-flow confidence, financing conditions, and balance-sheet durability. If firms keep generating credible revenue growth and margins remain passable, investors keep paying for that future. The unresolved headline risk then becomes a discount or premium term in valuation rather than a trigger for a complete de-risking. A practical implication: if your process still treats geopolitical headlines as all-or-nothing, you miss the actual driver. Treat it as a factor in expected scenario weights. The Practical Lens: What This Week’s Data Can Reprice The second key takeaway from the data-focused agenda is that not every macro release matters equally. The market has a hierarchy, and in current conditions that hierarchy is usually: inflation path, labor-market trend, and credit behavior, then rates expectations. The noise around geopolitics is secondary unless it reaches those channels. The macro release filter Instead of reacting to every number, use this triage: High impact if it changes the

Data-First Risk: Why This Week’s Market Upside Hinges on Surprises, Not Rhetoric

TL;DR: U.S. markets are treating this week as a data decision point, not a headline-only one, so valuation can stay elevated while conviction remains conditional. The message in the current headlines is clear: investors are tolerating geopolitical noise because policy and earnings still look credible enough in aggregate, but the next 24–48-hour move is more likely driven by whether economic releases confirm or disconfirm the base case. In practical terms, firms should prioritize scenario-based risk budgets and execution discipline over broad bullish/bearish positioning tied to a single narrative. (Source context: Kiplinger’s weekly economic data calendar, JP Morgan on record highs without an Iran breakthrough A market at record levels, not because it is fearless, but because it is selective Markets at record highs without a major geopolitical resolution can look contradictory until the mechanism is separated into two layers: valuation support and volatility patience. Valuation support is currently coming from the same place it often does during uncertain periods—profit resilience, liquidity preference, and the belief that recession risk is manageable for now. Volatility patience reflects the market’s willingness to discount only direct shocks and ignore unresolved uncertainty that has not yet moved balance sheets or policy language. This does not imply complacency. It implies conditionality. Risk assets are effectively pricing a path with upside optionality but limited near-term downside if incoming data stays inside forecast bands. The moment inflation, employment, or policy language deviates, that structure can repri

From Headline Noise to Execution Risk: How 2026 Markets Reprice Trump-Era Policy Without Rewriting Portfolios

TL;DR: The two headlines indicate a practical shift for 2026 investing: markets are not merely reacting to presidential policy headlines, but repricing execution risk as quickly as legislative, regulatory, or tariff signals become operational. In practice, that means the edge is no longer in guessing what the policy story says today, but in identifying which companies can turn policy tailwinds into repeatable cash flow this quarter. Weekly market structure remains the reality check: if breadth and earnings-quality rotate away from one-way macro bets, capital preserves itself by rewarding disciplined balance sheets and downside-ready pricing power over slogan-driven stories. Use as the lead visual to anchor that contrast. 1) Policy as a Market Variable, Not a Prediction Contest The U.S. Bank headline, the headline message is clear enough: investors are asking “who wins, when, and with what certainty?” under a pro-growth, policy-voltaic administration. The same question appears in almost every desk note this year, but most portfolios still confuse campaign rhetoric with accounting reality. The Market Is Pricing Certainty, Not Promise When policy discussions are broad, investors split into two camps: one that buys the narrative and one that waits for implementation milestones. The winning camp is smaller but steadier. They demand: Defined regulatory language, not broad intent. Observable tax and cost impacts, not campaign promises. Evidence in order books, capex guidance, and margin commentary. That is how a weekly headline wave becomes a stock-specific alpha opportunity. Why 2026 Feels Different From Prior Election Cycles A useful lens is to treat each policy area as a project pipeline, not a static bullish or bearish tag. Trade ideas s

The AI Bubble That Might Not Pop: Why June’s Macro Readout Could Reshape AI Capital Spending

TL;DR: AI strategy discussions are now less about choosing sides in a technology war and more about surviving the next financing cycle. The two source headlines combine into one practical signal: a hypothetical “AI bubble” crash matters less than whether upcoming macro data changes the cost and availability of capital. If inflation and growth signals stay mixed, the first real adjustment is likely not layoffs alone, but slower software, hiring, and cloud commitments. For finance and business teams, the advantage will go to firms that pre-commit to cash-flow proof now, not narrative-based optimism. This is a valuation-to-earnings pivot, not a hype narrative war. (Big AI bubble framing) The bigger question behind the two headlines The first headline asks a classic market question: what if AI enthusiasm unwinds? The second places that question inside a near-term timing frame by pointing finance teams toward key macro releases in a specific week. Put together, this suggests a shift in what matters for board-level decisions. The market’s previous AI playbook rewarded “strategic optionality.” Firms announced initiatives early, bet on top-line story, and expected follow-on rounds or favorable financing to smooth execution risk. In a less forgiving macro tape, strategy language is being replaced by a more operational test: Does this AI deployment generate measurable margin or retention improvement within this quarter or two? Is the spend incremental or merely aspirational? Can the team explain downside if capital costs rise or demand cools? Why an AI bubble pops quietly, not dramatically A “pop” in finance terms often looks like price compression before anyone names the event. Valuation drift vs. revenue reality When growth multiples are priced on future optimism, tiny disappointments in adoption speed can trigger multiple contraction. This is not necessarily a crisis, but it is a compounding drag on funded expansion. A practical implication:

Beyond Rocket IPOs: Why AI Wealth Effects Depend on Who Owns the Equity and Debt

TL;DR: The SpaceX-era AI headline cycle is pushing a broader shift in finance: households, retirement systems, and credit markets are being priced around speculative, narrative-heavy AI earnings stories. As argued by the AI-bubble framing, valuation momentum can outpace cash generation. For finance and business leaders, the key move is to treat AI exposure like a two-sided macro risk—potentially redistributive upside plus heightened liquidity and confidence shocks—by stress-testing, diversifying, and demanding clearer governance. In short, the strategy is not to avoid AI, but to stop pricing everything as if growth alone can survive repeated valuation reset cycles. The headline is a macro signal, not just a company story The headline about a major private-to-public tech transition is important, but its deeper lesson is market architecture: AI firms are becoming social and fiscal reference points for a broad class of investors. This matters because valuation narratives can migrate from stock exchanges into household expectations and institutional balance sheets faster than traditional sector news. A clean takeaway appears in the Guardian framing: after one flagship IPO, many will infer that everyone’s retirement, savings, and debt tolerance now hinges on AI valuation paths.[https://news.google.com/rss/articles/CBMieEFVX3lxTE1NQXhPQzdPQlR4Q2ZJUnpqckZLUEJqNlpUbjlVLVBBQ2M2WUpzRDVEOVllZW54NVhGdHE0Y1huSnpLdER6alZlYXdvTzkxNHg2VkxDOUJUbEdITFBEckc0VHNTOTh0T2RLUGVwWXdyZ3VUVjZNQ0Jadw?oc=5] When public headlines become personal finance anchors, volatility is no longer just about one firm’s multiple; it becomes a confidence variable in credit behavior, spending cycles, and hiring. Why this matters even if fundamentals remain strong When AI narratives rise quickly, firms can finance expansion with easier debt, but lenders and creditors also adjust margin assumptions. If everyone assumes AI cash flows will compound faster than they historically can, short-term leverage looks cheaper than it is. Finance professionals should treat AI as a cross-asset transmission channel, not a vertical. AI wealth effects are now distributed through households, not just funds The S

Beyond the Hype Curve: How AI Public-Market Shifts Turn Household Finance Into a Volatility-First Problem

TL;DR: The biggest financial shift after a high-profile AI company goes public is that ordinary households become indirectly exposed to a new kind of market regime risk. Public AI sentiment can amplify volatility in retirement portfolios, borrowing conditions, and business spending plans simultaneously. If AI enthusiasm cools sharply, the shock does not remain a sector story; it quickly becomes a household and SME cash-flow story. A resilient response is to separate upside participation from baseline survival: protect liquidity, de-risk concentration, and only keep controlled exposure to AI upside. Why AI IPO headlines are now a balance-sheet signal, not just a stock story The headline framing from the Guardian piece—that Americans’ financial future could be tied to AI after a major IPO—captures a structural change, even if the exact price path is debated. When mega-cap expectations are centered in one narrative, households stop experiencing AI as a distant technology trend and start experiencing it as a personal wealth condition. This is especially true in retirement accounts, home-ownership balance sheets, and working capital reserves of businesses that borrow against market confidence. In the Guardian framing, a large AI-linked public valuation can become the anchor many people unconsciously use for confidence assumptions. The three channels through which AI market sentiment reaches ordinary money Household balance sheets react through three channels First, portfolio beta: AI mega-stories can raise the market-to-market ratio and influence correlated mega-caps, not just direct AI holdings. Second, wealth and spending psychology: perceived paper gains can raise discretionary spending and risk-taking, while paper losses force cuts in non-essential spending quickly. Third, credit conditions: lenders, suppliers, and counterparties often interpret market valuation trends as proxy information, even when fundamentals are unrelated. Why downs

Beyond the Hype Cycle: How a SpaceX-Scale AI IPO Could Redraw Market Rules

TL;DR: The headlines are pointing to one durable investor lesson: AI is shifting from a software story to an infrastructure story, and infrastructure is financed, managed, and punished by markets differently. A major AI-linked IPO can trigger broad risk repricing across growth equities, but that does not automatically mean a collapse. The distinction that matters is between companies with durable cash generation and those whose valuations rely on keeping the story alive. If you map that distinction before the next cycle of capital flows, you protect both upside participation and downside resilience. ) Why the AI IPO narrative now looks like a balance-sheet story The first headline implies what many already feel: if a flagship company with AI, autonomy, and heavy infrastructure undertones goes public at scale, investors may start treating AI less like a software layer and more like a long-cycle physical/economic platform. When AI is tied to manufacturing, logistics, energy, launches, hardware, and service ecosystems, it resembles infrastructure more than a pure technology play. From narrative to governance In such a regime, disclosure quality becomes central. Investors will care less about press-release velocity and more about how capital is deployed: capex governance, margin behavior, contract mix, and failure tolerance. The article context about AI becoming tied to America’s financial future is less about hype and more about governance: can firms convert hype into cash-producing infrastructure returns? The shift in valuation language Under a narrative-only frame, “AI upside” can justify wide multiples with little scrutiny. Under a balance-sheet frame, multiples are disciplined by conversion timelines, debt capacity, and downside optionality. [The Guardian framing](https://news.google.com/rss/articles/CBMieEFVX3lxTE1NQXhPQzdPQlR4Q2ZJUnpqckZLUEJqNlpUbjlVLVBBQ2M2WUpzRDVEOVllZW54NVhGdHE0Y1huSnpLdER6alZlYXdvTzkxNHg2VkxDOUJUbEdITFBEckc0VHNTOTh0T2RLUGVwWXdyZ3VUVjZNQ

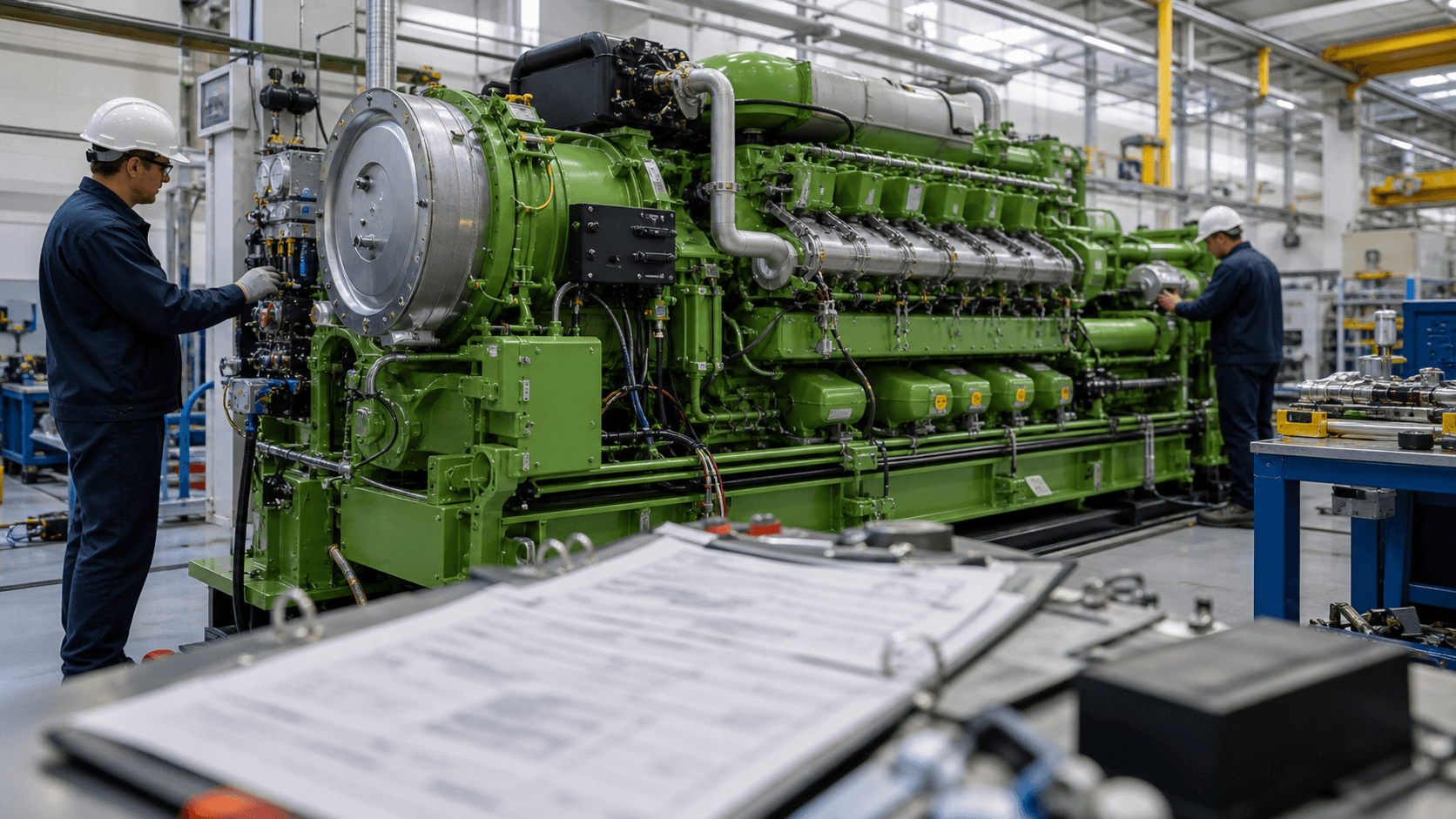

INNIO's IPO Makes Gas Engines A Public-Market Power Bet

TL;DR: INNIO priced an upsized $2.43 billion IPO, but the company is not getting the money. The offering is all secondary shares from its selling shareholder, while public investors are buying exposure to gas-engine power systems used in data centers, microgrids, industrial sites, and compression. The business implication is simple: the market is treating behind-the-meter reliability as investable infrastructure, even when the IPO proceeds mainly create sponsor liquidity. #What INNIO Actually Sold INNIO said it priced 90 million common shares at $27 each, up from a planned 75 million-share offering. The shares were expected to begin trading on the Nasdaq Global Select Market under the ticker INIO on June 4, 2026, with closing expected on June 5. That makes this look like a clean public-market debut. It is cleaner to read it as a transfer of risk and liquidity. The prospectus says the selling shareholder, AI Alpine, is selling the shares, and INNIO will not receive proceeds from the sale. It also says AI Alpine will still hold about 88% of the voting power after the offering, assuming the underwriters do not exercise their option. So the public market is not just financing a growth story. It is putting a public price on a sponsor-controlled industrial asset. #Why The No-Proceeds Detail Matters The IPO cash is not buying new factories This is the detail casual readers miss. A primary IPO can fund capacity, debt reduction, sales hiring, or research. A secondary-heavy IPO does something else: it gives existing owners a path to liquidity while public investors take the next leg of valuation risk. That does not make the deal bad. It does make the deal more honest. INNIO is not pitching a blank frontier dream. The prospectus shows 2025 revenue of $2.64 billion, adjusted EBITDA of $549 million, and first-quarter 2026 revenue of $668.6 million. This is an operating company with equipment, service, parts, and a large installed base. But the use-of-pro

Ciena's Quarter Says AI Needs a Traffic Budget

TL;DR: Ciena's June 4 quarter is not just another AI-adjacent earnings beat. It shows that the AI buildout is moving into a less glamorous but more durable line item: bandwidth. When revenue jumps to \$1.57 billion, up 40% year over year, and management lifts full-year guidance only one quarter after guiding for \$1.5 billion plus or minus \$50 million in Q2 revenue and \$5.9 billion to \$6.3 billion for fiscal 2026, the useful read is not "AI still hot." The useful read is that hyperscalers are now paying to move AI traffic, not just to create it. #Why This Quarter Matters More Than The Stock Move Most people still picture the AI spending boom as a chip story. That was fine when the main debate was who could get enough GPUs. It is less fine now. Once those clusters are installed, the next constraint is whether the data, training traffic, and inference requests can move fast enough between racks, campuses, and regions to keep the expensive compute busy. That is why Ciena's quarter matters. The company reported adjusted operating margin of 19.5%, up from 8.2% a year earlier, and raised fiscal 2026 revenue guidance to \$6.3 billion plus or minus \$100 million. A boring network supplier is not supposed to print results that look like this unless the customer problem has become urgent. The sharp point is simple: AI capex is no longer just a silicon budget. It is becoming a traffic budget. #What The GPU Story Misses Look at the physical workflow, not the AI keynote. An operations manager does not get paid because a model benchmark looks good on a slide. They get paid when the cluster trains on schedule, inference latency stays acceptable, and the expensive hardware does not sit around waiting on a slower network layer. That changes what buyers are optimizing for. Bandwidth is turning into utilization insurance I

QXO's $3 Billion Notes Put Building-Products Rollups On The Debt Desk

TL;DR: QXO's June 2 plan for a $3 billion senior-notes offering turns the TopBuild acquisition from a splashy building-products rollup into a credit-market test. The hidden issue is not whether QXO can announce scale. It is whether the company can make branch logistics, procurement, installation density, and working capital move fast enough to pay for the financing stack behind a $17 billion deal. #What QXO Is Really Financing QXO is not simply borrowing to buy a company. It is borrowing to buy a workflow. The planned notes are split into $1.5 billion due 2031 and $1.5 billion due 2034, with proceeds expected to help fund QXO's planned acquisition of TopBuild. If issued before the deal closes, the proceeds are expected to sit in escrow until the acquisition is completed. That escrow detail sounds technical. It is actually the whole story in miniature. The money is ready before the operating integration is real. Bond buyers are being asked to fund a future in which QXO can turn insulation distribution, installation crews, branch routing, supplier purchasing, and customer service into a larger, tighter machine. #Why The Debt Desk Matters More Than The Deal Headline QXO's April agreement to acquire TopBuild valued the company at about $17 billion. The combination would make QXO the second-largest publicly traded building-products distributor in North America, with more than $18 billion of combined revenue and more than $2 billion of combined adjusted EBITDA. Those are clean headline numbers. They are also not enough. The better question is whether QXO can convert scale into boring operating leverage. In building products, the profit does not show up because a spreadsheet says "national platform." It shows up when a branch manager has the right inventory, a contractor gets the delivery window promised, a truck route avoids a wasted run, and purchasing has enough volume to lean on vendors without damaging service. The finan

26North's Annuity Deal Turns Insurance Into a Private Credit Pipe

TL;DR: 26North Re said on June 1, 2026 it will buy Independent Insurance Group, owner of Independent Life, the insurer it described as the only carrier exclusively dedicated to structured settlement annuities for personal-injury claimants. The easy read is that another alternative-asset firm wants insurance float. The better read is narrower and more interesting: 26North is buying a liability origination machine in a corner of insurance where the product is not sold with flashy yield, but through trust, case design, and long-duration payment certainty. #The Interesting Part Is Not The Headline Picture the first scene: a settlement planner and a plaintiff attorney leaning over a payment schedule for an injured claimant. This is not a mass-market annuity pitch. It is a workflow built around customizing tax-advantaged periodic payments that may need to last for decades, sometimes for people who cannot easily absorb investment mistakes or liquidity shocks. That makes the insurer behind the promise part financing vehicle, part operating utility. Independent Life's own launch materials framed the company this way from the start in 2018: a focused insurer created specifically for structured settlements rather than a large life carrier squeezing the business in beside unrelated product lines. That is why the buyer matters. 26North Re already had about $13 billion of assets on a pro forma basis, while parent 26North Partners managed about $37 billion across private equity, private credit, insurance, and reinsurance strategies. It is not entering this market because structured settlements are glamorous. It is entering because a controlled liability stream can be a very good home for originated assets. #Why A Monoline Carrier Is Different From Generic Float Casual readers hear "insurance acquisition" and jump straight to Buffett-style float

Waldencast's Obagi Sale Says Beauty Rollups Need a Hero Brand

TL;DR: Waldencast's agreement to sell Obagi Medical to Bridgepoint is not just a skincare portfolio shuffle. It looks more like an admission that public investors do not want a beauty holding company with too many stories at once. They want a cleaner machine with one hero brand, a simpler P&L, and fewer excuses. #What Waldencast Is Actually Selling The headline is straightforward. Waldencast said on June 1 that it will sell Obagi Medical to Bridgepoint in a deal valued at up to $460 million and use the transaction to strengthen the balance sheet and focus on Milk Makeup. The company said it expects to keep a minority equity interest in Obagi, which means this is not a total walk-away so much as a capital reset with an escape hatch. That matters because Obagi was not some random extra asset. It was one of the two core operating brands inside the public beauty platform. Waldencast's recent financial disclosures already pointed in this direction. In its March 13 full-year results, the company said the earlier Obagi Japan trademark sale brought in $82.5 million and that $77.5 million of the proceeds went to debt repayment. Monday's announcement makes the pattern harder to ignore: this company is not broadening the portfolio. It is simplifying it under pressure. #Why This Looks Like A Conglomerate Discount Story Beauty investors usually say they like diversification until the public numbers arrive. A multi-brand structure sounds safer in theory. In practice, it often creates a reporting problem. One brand needs marketing spend, another needs distribution repair, another needs inventory discipline, and management ends up spending more time explaining the mix than proving operating leverage. Waldencast is effectively choosing clarity. The market rewards one clean growth engine Milk Makeup is easier to narrate to public investors than a blended beauty portfolio with uneven channels and mixe

The .25 Trillion Credit-Card Balance Is a Cash-Flow Test

TL;DR: U.S. credit-card balances dipped seasonally in Q1 2026, but the real story is not consumer relief. The New York Fed still shows $1.25 trillion in card debt, serious card-delinquency flow around 7.1%, and rising credit limits. That combination says credit cards are becoming a cash-flow bridge for households and a pricing test for banks, retailers, and investors. #What the Credit-Card Data Actually Says The easiest mistake is to see a quarterly balance decline and call the consumer healthier. The New York Fed's Q1 2026 household debt report says credit-card balances fell by $25 billion in the first quarter, to $1.252 trillion. That sounds benign until you notice the annual change: card balances were still up $70 billion from a year earlier. The same report says aggregate card limits rose by $60 billion in the quarter. Lenders are not simply watching borrowers deleverage. They are still extending room. That is the business story. Why a lower balance can still mean more stress Credit cards seasonally improve after year-end spending, tax refunds, bonus payments, and household budget resets. A Q1 dip is not the same as a durable paydown. The better question is whether households are paying cards down because cash flow improved, or because they are temporarily using tax-season liquidity to reset before borrowing again. For banks and retailers, that distinction matters more than the headline balance. #Why Cards Are Becoming a Cash-Flow Product At a kitchen table, the card balance is not an abstract liability. It is groceries, a utility bill, an auto repair, a medical copay, and the line between paying this week or waiting for the next paycheck. That is why the Federal Reserve's March 2026 consumer credit release is worth reading next to the New York Fed report. Revolving credit increased at a 3.8% annual rate in Q1, and the rate on credit-card accounts assessed interest was 21.52%. At that price, a card is not cheap liquidity. It is expensive working capital for households. The hidden implication is simple: the credi