INNIO's IPO Makes Gas Engines A Public-Market Power Bet

TL;DR: INNIO priced an upsized $2.43 billion IPO, but the company is not getting the money. The offering is all secondary shares from its selling shareholder, while public investors are buying exposure to gas-engine power systems used in data centers, microgrids, industrial sites, and compression. The business implication is simple: the market is treating behind-the-meter reliability as investable infrastructure, even when the IPO proceeds mainly create sponsor liquidity.

##What INNIO Actually Sold

INNIO said it priced 90 million common shares at $27 each, up from a planned 75 million-share offering. The shares were expected to begin trading on the Nasdaq Global Select Market under the ticker INIO on June 4, 2026, with closing expected on June 5.

That makes this look like a clean public-market debut. It is cleaner to read it as a transfer of risk and liquidity.

The prospectus says the selling shareholder, AI Alpine, is selling the shares, and INNIO will not receive proceeds from the sale. It also says AI Alpine will still hold about 88% of the voting power after the offering, assuming the underwriters do not exercise their option.

So the public market is not just financing a growth story. It is putting a public price on a sponsor-controlled industrial asset.

##Why The No-Proceeds Detail Matters

#The IPO cash is not buying new factories

This is the detail casual readers miss. A primary IPO can fund capacity, debt reduction, sales hiring, or research. A secondary-heavy IPO does something else: it gives existing owners a path to liquidity while public investors take the next leg of valuation risk.

That does not make the deal bad. It does make the deal more honest.

INNIO is not pitching a blank frontier dream. The prospectus shows 2025 revenue of $2.64 billion, adjusted EBITDA of $549 million, and first-quarter 2026 revenue of $668.6 million. This is an operating company with equipment, service, parts, and a large installed base.

But the use-of-proceeds signal still matters. Public buyers are not funding the machine so much as buying into the machine after private ownership has already built the story.

##Where The Real Demand Is Coming From

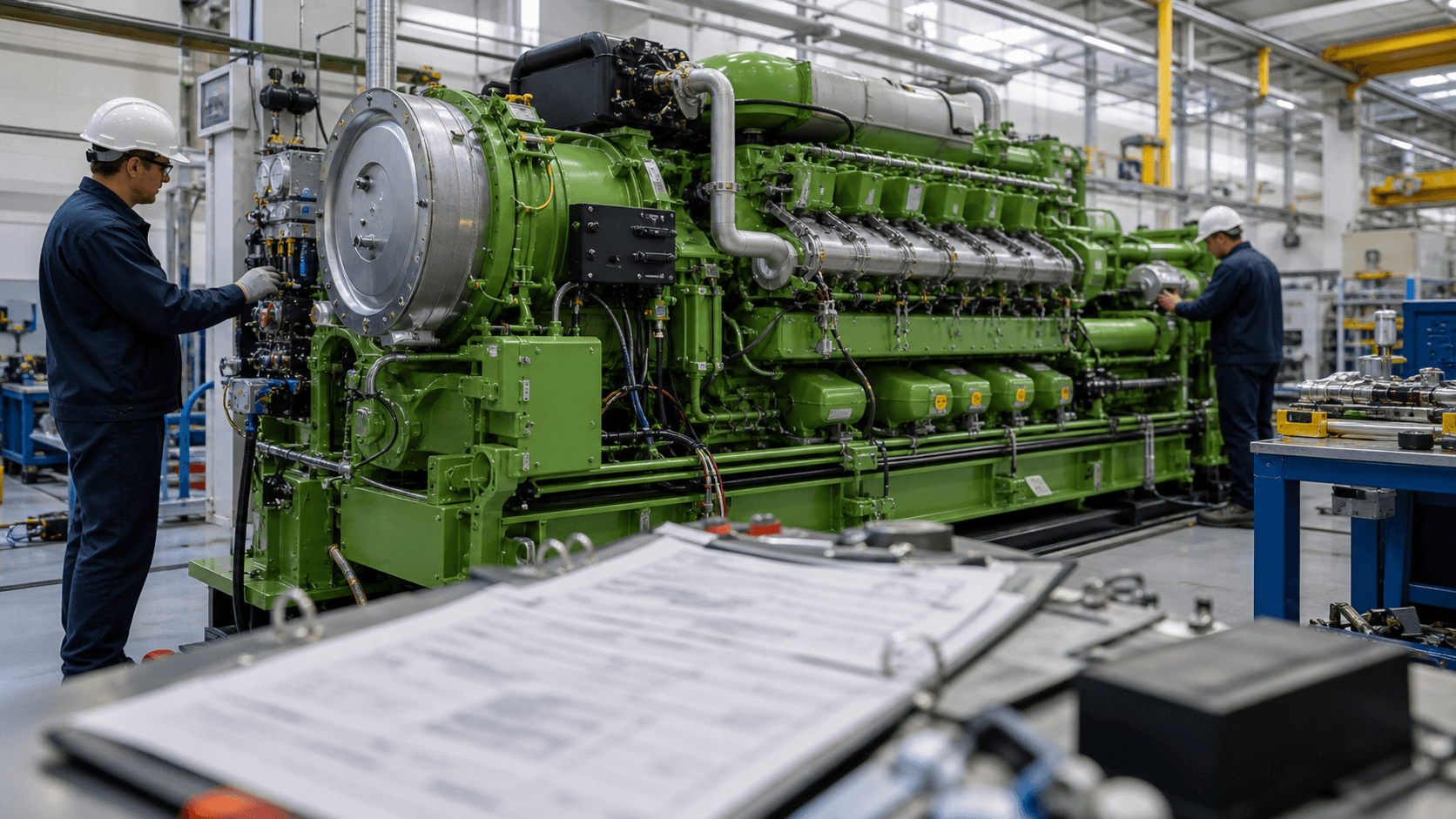

INNIO describes itself as a global distributed energy solutions provider that designs, manufactures, and services power systems under the Jenbacher and Waukesha brands. Its own release points to data centers, microgrids, grid stabilization, industrial energy, and gas compression.

That mix is why the IPO belongs on a finance desk, not a technology desk.

The customer problem is ordinary and expensive: a data-center developer, factory operator, or energy-service provider cannot wait for perfect grid capacity if the site needs reliable power now. A gas engine is not glamorous. It is a schedule tool.

#Services make the installed base more than hardware

The prospectus breaks the business into equipment and services, and the services line is the part investors should watch closely. Engines need parts, regular service, overhauls, remanufacturing, monitoring, and controls across their lifecycle.

That turns an industrial sale into a long service relationship. It also changes the margin question.

If INNIO is only selling engines into a hot power cycle, investors are buying a cyclical equipment story. If services attach deeply to the installed base, investors are buying recurring maintenance economics tied to uptime.

##Who Is Really Taking The Bet

The obvious buyer is an investor who wants exposure to electricity demand without buying a regulated utility or a hyperscaler. INNIO offers a different wrapper: distributed generation, fast-start reliability, and service revenue around equipment that sits close to the load.

The less obvious buyer is the CFO inside a constrained project.

Imagine a colocation site with customers signed up, racks planned, and interconnection timing still uncertain. The project team does not need a speech about energy transition purity. It needs a practical answer to a commercial question: can the site commit to uptime without letting the grid queue control the revenue start date?

That is where behind-the-meter equipment earns its premium.

##What Investors Should Watch Next

The risk is that public markets confuse power scarcity with pricing power. They are related, but not the same thing.

Three handoffs matter now:

- Equipment orders need to become delivered systems, not just backlog excitement.

- Services revenue needs to prove it can smooth the cycle when equipment demand cools.

- Sponsor control needs to coexist with public-shareholder discipline, especially after a no-proceeds IPO.

INNIO may be a useful public proxy for the most physical part of the AI and industrial power buildout. But the cleaner question is not whether electricity demand is rising. It is whether investors are being paid enough to own a controlled company after the sponsor has already taken the first public-market exit.

#FAQ

What did INNIO price in its IPO?

INNIO priced 90 million common shares at $27 each, an upsize from the originally proposed 75 million shares. The company expected the shares to trade on Nasdaq under the ticker INIO.

Does INNIO receive money from the IPO?

No. The prospectus says the shares are being sold by the selling shareholder and that INNIO will not receive proceeds from the sale.

Why is this relevant to AI infrastructure investors?

Data centers need reliable power before they can turn buildings, chips, and customer contracts into revenue. INNIO gives public investors exposure to the behind-the-meter equipment and service layer that can help projects manage that power-timing problem.