INNIO's IPO Makes Gas Engines A Public-Market Power Bet

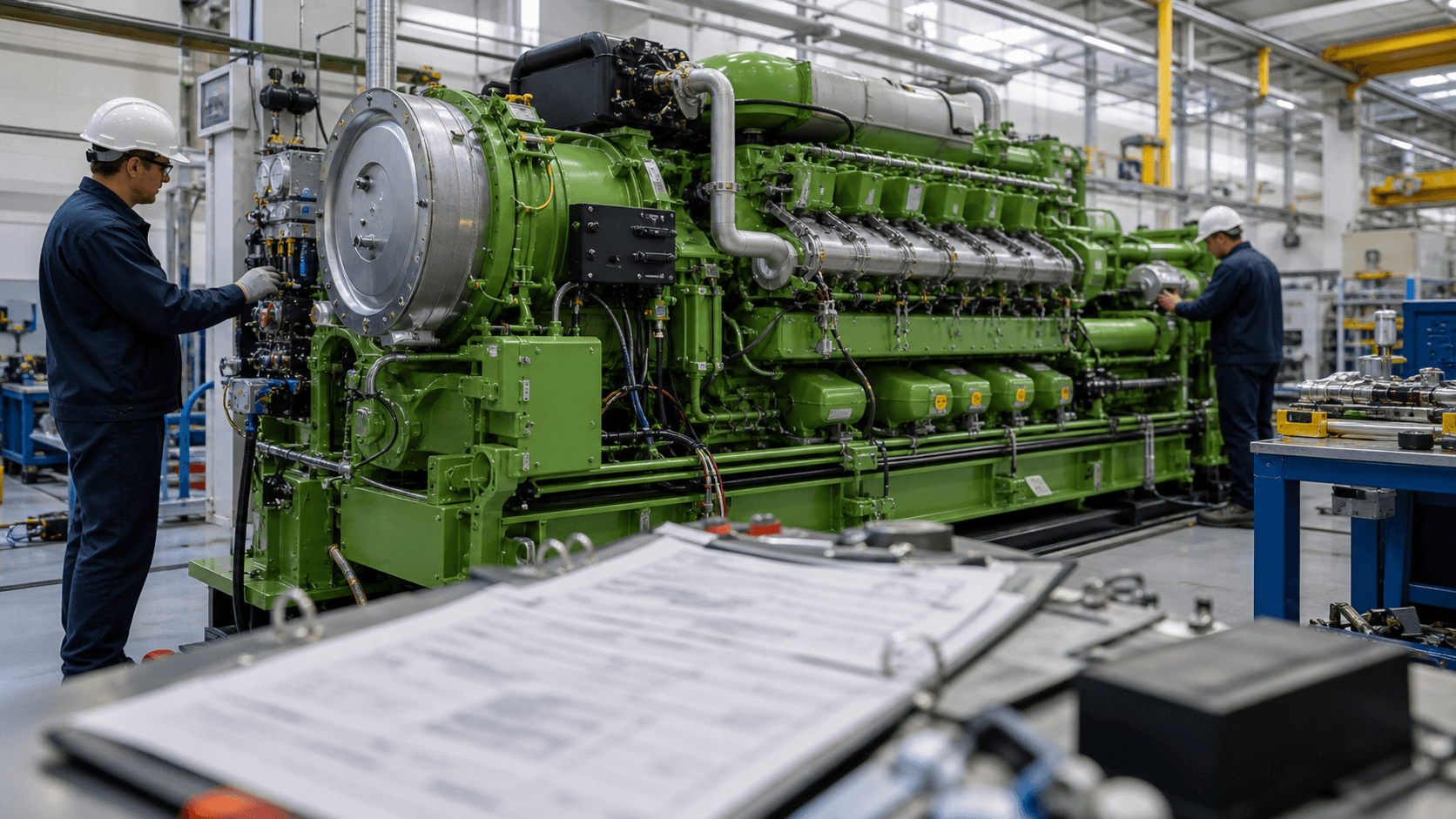

TL;DR: INNIO priced an upsized $2.43 billion IPO, but the company is not getting the money. The offering is all secondary shares from its selling shareholder, while public investors are buying exposure to gas-engine power systems used in data centers, microgrids, industrial sites, and compression. The business implication is simple: the market is treating behind-the-meter reliability as investable infrastructure, even when the IPO proceeds mainly create sponsor liquidity. #What INNIO Actually Sold INNIO said it priced 90 million common shares at $27 each, up from a planned 75 million-share offering. The shares were expected to begin trading on the Nasdaq Global Select Market under the ticker INIO on June 4, 2026, with closing expected on June 5. That makes this look like a clean public-market debut. It is cleaner to read it as a transfer of risk and liquidity. The prospectus says the selling shareholder, AI Alpine, is selling the shares, and INNIO will not receive proceeds from the sale. It also says AI Alpine will still hold about 88% of the voting power after the offering, assuming the underwriters do not exercise their option. So the public market is not just financing a growth story. It is putting a public price on a sponsor-controlled industrial asset. #Why The No-Proceeds Detail Matters The IPO cash is not buying new factories This is the detail casual readers miss. A primary IPO can fund capacity, debt reduction, sales hiring, or research. A secondary-heavy IPO does something else: it gives existing owners a path to liquidity while public investors take the next leg of valuation risk. That does not make the deal bad. It does make the deal more honest. INNIO is not pitching a blank frontier dream. The prospectus shows 2025 revenue of $2.64 billion, adjusted EBITDA of $549 million, and first-quarter 2026 revenue of $668.6 million. This is an operating company with equipment, service, parts, and a large installed base. But the use-of-pro