Elara Bennett is a finance strategist and business analyst, sharing insights on market trends, investment strategies, and corporate growth. She blends data-driven research with practical advice to help professionals and investors make smarter decisions.

A Bitcoin Miner Just Bought $1.6 Billion in Chips From the Guy Who Owns Its Stock

Three years ago IREN dug for Bitcoin. This week it agreed to spend about $1.6 billion on Dell systems packed with Nvidia's Blackwell GPUs for a data center in Childress, Texas, and the stock jumped almost 29% in a day. The pitch is clean: it's not a miner anymore, it's an AI cloud company, and the run-rate revenue climbs toward $4.4 billion by early 2027. Yahoo Finance Here's the part the headline skips. The $1.6 billion buys hardware to feed a five-year, $3.4 billion AI cloud contract with Nvidia. And Nvidia isn't just the customer at the other end of that contract. Nvidia also holds an option on up to 30 million IREN shares at $70 apiece, a stake worth around $2.1 billion. BigGo FinanceThe Motley Fool So read the loop slowly. Nvidia takes a position in IREN. IREN turns around and buys Nvidia chips through Dell. Nvidia books the sale, the revenue looks real, the stock of both companies goes up. The money makes a lap and comes home. This isn't IREN's invention. It's the move of the whole AI build-out right now. Nvidia put as much as $100 billion into OpenAI to fund data centers stuffed with Nvidia's chips. Somebody on the internet called Nvidia the central bank of AI, and it stuck because it's basically true. JPMorgan looked at IREN's version of this and slapped a Sell on it, flagging the circular nature of the Nvidia relationship. business-standardBigGo Finance We've watched this film before. During the dotcom run, Cisco lent telecoms the money to buy more Cisco routers. The sales looked great until the capital dried up and the whole thing collapsed. Vendor financing isn't a cri

Nobody on That Trading Floor Has to Make Your Mortgage Payment

Here's the line that should make you laugh, then make you angry: lower Treasury yields and cheaper oil "may support a Wall Street rebound." May. Support. A rebound. That's the financial press telling you the market might go up if two things that have been jerking around for three months happen to jerk in the friendly direction for a day. And they're not wrong, exactly. The 10-year yield did pull back from 4.69%, the highest it's been since January of last year. Crude did drop under $100 a barrel after holding above it for weeks. Stocks did claw back the loss. All true. But watch what that framing quietly does. It turns a war into a weather report. The war started February 28. Oil spiked, inflation came back, and the bond market did what bond markets do when they get scared, which is sell off and drag every borrowing rate in the country up behind it. The 10-year yield is the thing your mortgage actually follows, not the Fed, not the headlines, that one number. So when traders panic, a couple in Ohio who found a house they could finally afford watches the rate on it climb before they can sign. That's not a "rebound." That's their down payment buying less every Tuesday. And here's the part I can't get past. Back in March, the 30-year fixed dipped below 6% for the first time since 2022. Economists got excited, called it a psychological breakthrough, figured it might thaw the frozen housing market. People who'd been waiting two, three years started running the numbers again. Then the oil shock hit and rates went right back up. One Zillow economist put it about as bluntly as anyone in that world will: those households missed a flash sale. A flash sale. Like the thing that decides whether a family of four gets a yard is a doorbuster that closed before they got to the register. Now the rate is back near 6.5%, mortgage applications have cratered, and the same financial pages that ran "buying a home just got more expensive" in April are running "rebound may be supported" in May. Same chart. Different mood. Both t

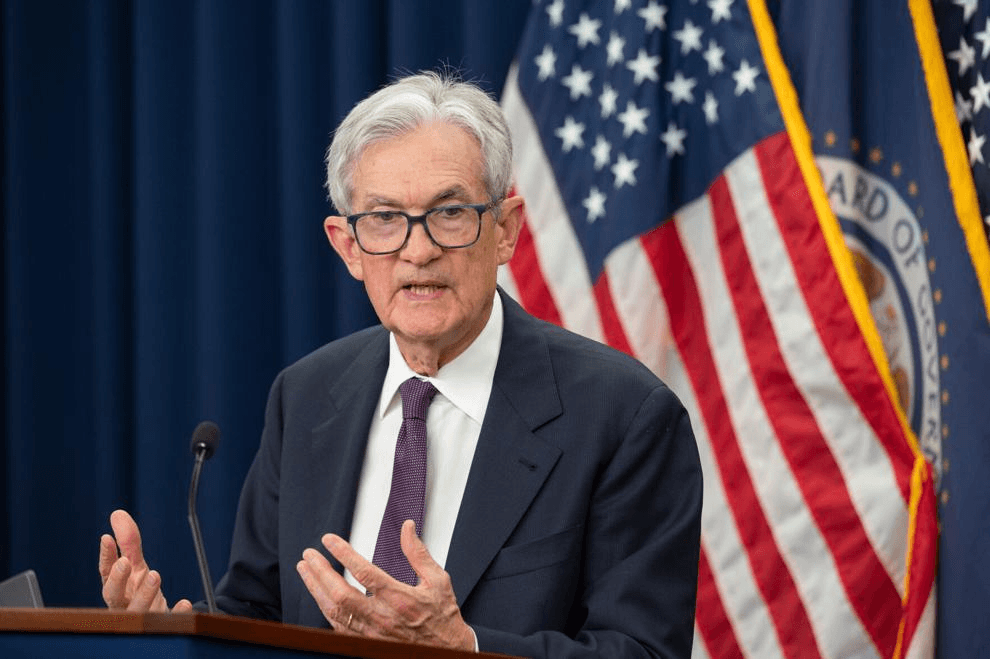

The Fed Chair Who Stayed to Protect the Institution While People Ran Out of Money

Jerome Powell stepped down as Federal Reserve chair this week after eight years that will probably be remembered less for what he did right and more for what ordinary people couldn't afford by the time he left. Tomato prices are up 40 percent over the past year. Overall groceries cost 30 percent more than they did six years ago. Rent is climbing steady. A recent college graduate working in hospitality in Boston told a reporter that grocery shopping used to be mindless but now it's "strategic"—she plans every purchase around saving money she barely has. This is the economy Powell exits. A news cycle all about him defending the Fed's independence against Trump's bullying gets written, and somewhere a 25-year-old is buying fewer vegetables because the arithmetic doesn't work anymore. Powell inherited a lucky hand in 2018. Unemployment was already low, inflation was too low, and the Fed's benchmark rate sat at 1.25 percent. Then came the pandemic, the supply-chain chaos, and two administrations pumping trillions into the economy. Inflation ripped higher. By the time Powell started raising rates seriously in 2022, the damage was already baked in. Rents had jumped, groceries had jumped, and they've stayed jumped. Raising rates after the spike doesn't un-spike the prices. It just makes borrowing expensive for the people who weren't at the party but have to pay for cleanup. The Fed kept rates near zero longer than it should have in 2021 and 2022, and Powell admits as much in interviews. But by then the narrative had shifted. Powell stopped being the guy who moved too slow and became the guy defending institutional independence. When Trump came back into office, he went after Powell—investigations, threats, demands that rates be slashed. Powell, to his credit, stayed put. Didn't resign, didn't fold, kept the Fed's seat at the table when politicians were trying to turn it into a joke. That's the story that sold: Powell as the guardian of the temple. The story no one tells is the one about the people for whom independence meant nothing. Lower-income households "economize," Powell himself said in recent interviews—they trade down from brands, cut purchases, stre

They Hired Him to Cut. The War Had Other Plans.

Gold sits near $4,520 an ounce. Read that number twice. A few years back the gold bugs sounded like cranks at a barbecue, and now the metal is parked at a level that would have gotten you laughed out of the room in 2021. It slipped a little Friday, half a percent, because the dollar firmed up and oil stayed hot and the market started betting the Fed might actually raise rates before the year is out. Sixty percent odds of a hike by December, says the CME FedWatch tool. Not a cut. A hike. Now hold that next to the other thing that happened Friday. Kevin Warsh got sworn in as Fed chair, in the East Room of the White House, Clarence Thomas holding the bible, Trump beaming in the front row. First time a Fed chair has been sworn in at the White House since Greenspan in 1987. The whole point of putting Warsh there was rates. Trump spent a year hammering Powell to cut, even floated 1%, and went looking for a chair who saw it his way. He found one. And the guy walks in the door to an economy that wants the opposite of what he was hired to do. Here's the part I keep chewing on. Warsh used to argue that AI would juice productivity, push prices down, give the Fed room to ease. Reasonable take. Then the US and Israel went to war with Iran, crude blew from the low $70s to north of $115 in two weeks, and gas at the pump went from $2.98 in late February to $4.56. You can't AI your way out of a gas pump. Inflation's running 3.8% year over year, the hottest in three years, and energy alone is up almost 18%. The man's whole framework got mugged by a tanker route. So picture who actually eats this. Not the gold trader, he's fine, he's up. I mean the couple who did everything the responsible adults told them to do. They waited. They didn't stretch for a house at 7%, they sat tight, they watched, because everybody said rates were coming down. And rates did come down. Earlier this year the 30-year dipped under 6% for a blink. A Redfin economist put it plainly: house hunters waited for rates to drop, they finally fell below 6%, and then they bounced right back. The war did it. The window opened a crack and slammed on their fingers. There's a loan officer in suburban Atla

The Fed’s New Risk Is Not Talking Less. It’s Being Trusted Less

Kevin Warsh’s skepticism of forward guidance sounds like a technical debate. Should the Fed tell markets what it expects to do, or should it wait, meet, and decide? But the bigger issue is credibility. If a new Fed chair arrives after intense White House pressure for lower rates, then says he wants less forward guidance, investors will ask a blunt question: is this disciplined humility, or a way to make policy less accountable? That is why Claudia Sahm’s warning matters. Her concern is not that the dot plot is sacred. It is that the Fed spent two decades building more transparent communication, and Warsh seems willing to pull part of that structure apart without yet offering a better replacement. The timing is awkward. Warsh took office as Fed chair on May 22, 2026. The Fed’s April 29 implementation note kept the federal funds target range at 3.50%-3.75%. April FOMC minutes showed higher Treasury yields, higher near-term inflation compensation, and continuing pressure from the Middle East conflict. This is not a quiet backdrop for a communications experiment. The labor market is also not cleanly strong. BLS reported April payrolls rose by 115,000, while unemployment held at 4.3%. That is not recessionary panic, but it is soft enough that every inflation and jobs print now matters more. Warsh has a reasonable point: forecasts can trap policymakers. The March 2026 SEP had Fed officials projecting 2026 PCE inflation at 2.7%, up from 2.4% in December. Forecasts move. Overconfident guidance can make a central bank slow to adjust. But markets do not need perfect forecasts. They need a reaction function. If Warsh weakens the dot plot and forward guidance, he has to replace them with something clearer: how much inflation persistence matters, how much labor-market weakening matters, and how the Fed separates data dependence from political pressure. That is the real test. Less guidance can work if it means less false precision. It fails if it means less transparency. For investors, this is not a simple bullish o

Nvidia Found 80 New Data Centers. Someone Near Them Is Paying for It.

Nvidia just had the kind of quarter that makes analysts run out of adjectives. Eighty-two billion in revenue. Profit up triple digits. The CFO bragged that the company is now standing up AI compute in more than 80 sites that each pull over 10 megawatts. The stock fell 1.8% the next day. That drop is the part everybody wrote about, and it's the least interesting thing here. What caught me was the framing. Nvidia spent the call selling a new story: it doesn't need the giant cloud companies anymore. There's this whole second bucket now, christened ACIE, which is finance-speak for everyone who isn't Amazon or Google. Sovereign governments. Old-line enterprises. Standalone AI clouds. It came in at $37 billion, basically dead even with the hyperscalers. AI cloud revenue more than tripled year over year. The pitch writes itself. We used to lean on four customers. Now the demand is everywhere. Everywhere. Sit with that word a second. Because "everywhere" is also where the power has to come from. Those 80-plus sites Colette Kress mentioned with such pride, each eating more than 10 megawatts, do not run on enthusiasm. They run on the same grid your refrigerator does. And the bill for hooking them up, the new substations and transmission lines, the utilities mostly spread across every ratepayer on the system, whether or not a single server in that building does anything for you. You can watch it land. In Georgia, a typical household power bill has climbed to around $175 a month, roughly six times higher across two years, while the utility asks to spend $15 billion more on capacity it needs mostly to feed data centers. A woman outside Atlanta told a reporter the price was running her pocket. That's the voice that doesn't make it onto the earnings call. There's no slide for her. This is the quiet handoff nobody on the call names. The article I read about the quarter called it "a business beyond hyperscale," like that's pure good news, a company outgrowing its dependence. Read it from the other end of the wire and it says

The Stock Tripled. The Chip It Sells Is Still Losing.

Here's the thing nobody chasing Intel right now wants to sit with. The stock is up 222% this year. The product that's supposed to justify any of it just lost another six points of market share. That's the whole tension in one breath. Mercury Research put Intel's slice of the server CPU market at 66.8% for the first quarter, down from 72.8% a year before. Servers are the crown jewel, the chips that run the world's data centers, and Intel is bleeding them to AMD one quarter at a time. Not crashing. Bleeding. The slow kind that's easy to talk yourself out of noticing while the share price does something the opposite of slow. And look at how AMD is winning, because the texture matters. Its EPYC chips made up only about a third of the units sold. But it pulled in 46.2% of the revenue. People are paying a premium for the AMD part. Lisa Su called it four straight quarters of record server CPU revenue, growth over 50% with both cloud and enterprise buyers leaning in. When customers cheerfully pay more for your rival's chip than for yours, that's not a market-share blip. That's a verdict. Intel's defense, more or less, is that it can't make enough. Lip-Bu Tan told investors demand is running ahead of supply, especially for Xeon. Which sounds like a good problem until you remember the customer who can't get a Xeon doesn't sit and wait. They buy the EPYC sitting on the shelf. Supply you can't deliver is just demand handed to the guy across the street. So why is the stock at 222%? Because the turnaround story is real on its own terms. Earnings are projected to jump 159% this year. The 18A process is in production. There are reports of Apple, of Google Cloud, of Musk wanting the next node for his Texas fab. Tan's pitch that agentic AI needs more CPUs is not nothing. I get why people bought it. I get why they're still buying it. But the number I can't get past is 904. That's what Intel trades at against trailing earnings. Nine hundred and four times. The Nasdaq sits at 43. Even the forward multiple of 139 is a steep climb.