Tracks market momentum, valuation shifts, and investor sentiment across public companies and sectors.

Same Tape, Different Stories: Why Fed Opening Hours, Dow New Highs, and SpaceX Momentum Point to a Portfolio Reset

TL;DR: The three headlines together describe a market split rather than a simple up or down day. One lane is macro: the Fed meeting opens with broad buying and index-level support, most clearly reflected in Dow strength. Another lane is composition: mega-trade stories in AI and communication/media are dictating which names attract incremental demand, as shown by SpaceX and Fox-related activity. For finance teams, the takeaway is to separate systemic tone from stock-specific thesis, then rebalance around dispersion instead of treating all leaders or laggards as one risk bet. In practice: favor liquidity discipline and scenario-based sizing over headline certainty. The market is giving two messages at once The first headline says the broad tape is not broken by worry at all: the session opened with a Fed-centered backdrop, a context investors still over-weight heavily even when price action is not fully synchronized. The second headline reinforces the same point by repeating the broad-index narrative (Dow making another record, market tone still constructive). That is useful because it suggests macro liquidity has not been withdrawn. Why this matters for positioning When markets say "risk-on" in index form but "risk-selective" in constituents, portfolio managers usually face a temporary skew: quality, balance-sheet strength, and narrative clarity get rewarded more than indiscriminate beta. In that environment, one-size-fits-all exposure changes become dangerous, while selective conviction trades become attractive. Dow leadership versus tech softness is not a contradiction A headline about the Dow gaining while tech slips can look contradictory at first glance, but it usually means the path of least resistance in the index is being carried by sectors with steadier cash-flow profiles or defensive trade structures. You are seeing a breadth transfer inside growth-heavy markets: risk appetite exists, yet not all risk assets are priced as equally attractive. That divergence is itself valuable information. Reading index strength correctly The index is a weighted story. If leadership narrows to a smaller group, that is often a warning sign about disp

Markets at Record Highs With No Iran Breakthrough: Why This Week’s Data Is the Real Market Switch

TL;DR: Record highs are not proof that geopolitical risks have disappeared, only that investors expect either a quick reduction in headline anxiety, or enough earnings and liquidity support to absorb bad news. The stronger signal for the next move is likely the economic calendar, where one print can flip positioning instantly. Watch volatility conditions, earnings durability, and whether policy expectations are repriced before reacting to every political update. A resilient process is not to predict Tehran outcomes in advance, but to pre-commit risk response levels to future data points and stick to them. The Tape Is Calm, but Not Decisive This setup is paradoxical: headline risk remains, but assets are still near records. The current logic is often misunderstood as naïveté; in practice, it can reflect a sophisticated bargain among participants. Many are paying for three things: optionality against a negative surprise, income from equity exposure, and confidence that any geopolitical escalation that materially changes cash flow expectations has not yet materialized. A key lesson from the J.P. Morgan discussion is that no-news stability is not equivalent to no-risk pricing. It is often a temporary equilibrium where holders accept headline uncertainty because the distribution of expected outcomes still favors a contained path. J.P. Morgan frames this tension as markets holding near highs amid unresolved Middle East headlines. What the Market Is Really Discounting The current question is not “Will there be progress in diplomacy?” but “What would make the repricing math break?” 1) Volatility Is Being Borrowed, Not Earned When investors believe downside is capped, risk premia compress and implied hedging costs look expensive. That can keep broad indices supported, but it also raises sensitivity to data-dependent reversals. You can

No-Shock Equities: How to Trade a Record Tape When Diplomacy Stays Incomplete

TL;DR: Stocks at record highs can coexist with unresolved geopolitical headlines because markets are currently pricing uncertainty as an existing condition, not a sudden regime shift. The practical lesson from this setup is simple: stop trying to forecast the diplomatic outcome and instead map what would actually change your positioning first. For finance teams, the edge is sequence management—what data, rate signals, and liquidity conditions can rotate risk gradually versus what actually breaks the tape. In a no-resolution environment, the best portfolio edge is less tactical prediction and more disciplined scenario architecture tied to observable triggers. Market signal: why a record tape can persist without a settlement The headline framing is clear: equity values can remain elevated even when a geopolitical issue remains unresolved. This is not paradoxical for markets that are fundamentally discounting probabilities. If the probability-adjusted distribution of risk already includes the adverse scenario, fresh headline noise has less immediate impact unless it creates incremental surprise. What “no resolution” contributes to valuation The unresolved issue can keep a drag premium in valuations, but it does not automatically force de-risking. Markets react to marginal information. If earnings quality, liquidity, and macro policy conditions stay stable, participants can continue to reward cash-flow compounding and multiple stability despite policy uncertainty. Investors then are not being reckless; they are expressing that uncertainty is already priced and waiting for evidence. Why this matters for business desks and CFOs Corporate treasuries and fixed-income committees should not confuse headline stress with terminal risk. If funding markets remain stable and operating conditions are intact, a board may still approve capex and buybacks while increasing contingency planning. That split—the continuation of operations plus contingency hedging—is exactly what a priced-in headline world produces. The practical task becomes preserving optionality at the operating level while avoiding emotional overreaction in financial policy. What the week’s calend

Beyond Geopolitics: Why Record Markets Ignore Iran Headlines and Watch the Data Calendar Instead

TL;DR: Global equities can stay near record levels even when headlines are sharp, because investors are increasingly pricing policy uncertainty as a manageable variable and letting near-term U.S. economic data set the true tone for risk appetite. A stalled geopolitical story like Iran creates noise, but not necessarily a sustained repricing of cash flows. The sharper catalyst this week is the macro calendar itself—especially inflation, employment, and growth data that can move policy expectations more directly than diplomacy headlines. In practice, strategy is shifting from narrative trading to data-weighted positioning. Why unresolved geopolitics is not automatically a bearish regime The most debated question this cycle is not whether geopolitics matters—of course it does—but whether it is the primary factor in market pricing every day. The first candidate headline frames the paradox directly: markets at record highs despite unresolved Iran tensions. That setup often reflects a classic “risk-on with selective hedging” state, where participants accept headline uncertainty so long as central bank reaction functions remain readable. It is exactly when policy signals become clear that equities re-rate quickly; when they do not, equity buyers often stay in. Data, not headlines, has become the weekend-to-weekday pivot The second source emphasizes this: this week’s watch list is about what the economy prints. That framing is important because it defines where money can move fastest. Which releases most often alter equity risk faster than diplomacy In the near term, three kinds of reports usually dominate decisions: Inflation trajectory (or at least the direction of trend) Labor strength and its implications for discretionary demand Policy language from officials after seeing the data set Markets tend to respond less to geopolitical headlines when those reports arrive with clarity. A stable macro read can support “growth despite noise,” while a hotter surprise can compress multiples even if geopolitica

Beyond the AI Hype Cycle: The Hidden Balance-Sheet Risk in America’s Growth Story

TL;DR: America’s AI boom still feels vibrant on headlines, but investors may be pricing the story as if execution friction were costless. The key issue is whether AI spending is converting into durable cash flow while finance conditions remain volatile. This is where the next repricing can begin: not when headlines turn negative, but when balance sheets show slower payoffs than expected. With next week’s economic calendar in focus, decision-makers should watch hiring, inflation signals, and financing conditions as closely as they watch AI-capex announcements, because those inputs determine which winners remain. Why the AI cycle feels stronger than many participants admit The headline point is clear: confidence is not gone. The latest coverage framed the U.S. AI boom as still carrying momentum and broad participation across sectors Financial Times context. Yet the market often confuses deployment intent with deployment outcome. Companies can announce AI initiatives, but investors eventually care about net contribution to margin, cash flow stability, and debt-servicing flexibility. That is why AI discourse now needs a maturity lens: not "How many projects?" but "How much of each project reaches scale without depressing returns?" The strongest companies are not necessarily the loudest spenders. They are the ones that can absorb the upfront costs and then improve unit economics. In finance terms, AI is becoming a working-capital and operating-leverage question, not only a growth narrative. The accounting lag is the real headline risk AI programs often show long delays between launch headlines and revenue translation. During that gap, firms can look expensive unless they can clearly signal milestones: deployment density, productivity per head, and customer retention tied to AI features. If those signals arrive while financing is expensive, the valuation reset can be swift. If they arrive with strong demand and stable rates, the valu

Why the AI Bubble Is a Risk of Mispricing, Not a Binary Crash: What Finance Teams Should Watch This Week

TL;DR: The AI story in markets is shifting from a binary debate about collapse versus permanence into a balance-sheet reality check: can companies convert AI spending into durable cash flow when the next set of economic indicators arrives? Finance teams should treat AI as a second-order productivity thesis, not a one-off earnings headline. On the one hand, AI can still accelerate margins and command premium multiples; on the other, macro data on jobs, inflation, and spending can quickly reprice those expectations. The same week that fuels AI exuberance can also expose leverage and funding stress if growth decouples from returns. Start by linking narrative to cash-flow assumptions, not slogans. (AI bubble stress framing). This week, investors should watch whether macro data changes the cost of capital more than the narrative changes the growth story. Why the Market Needs a Better AI Bubble Test The central question is not whether AI is “real enough,” but whether AI is priced as a utility business, a platform monopoly, or a speculative bet. Investors have not priced this uniformly. Some pockets of the market are using one multiple across all AI-adjacent firms, while credit desks are implicitly testing each business on cash conversion. From headline buzz to cash conversion The practical test is simple: are AI investments producing measurable productivity gain within current cost structures? If infrastructure spend rises but operating leverage improves, the valuation premium can be defended. If revenue grows but free cash flow stays negative, the market is betting on future re-rating through refinancing or higher prices, which is a weaker foundation. Finance teams should avoid binary calls and model a few “if-this-happens-then-that” pathways. What investors usually miss is the timing mismatch. AI spending decisions are often annualized over five years, while funding markets reprice quarterly. That gap creates volatility cycles: strong narrative qua

AI’s Real Risk Is Not a Coding Mistake but a Repricing Engine for Mainstream Wealth

TL;DR: The two headlines suggest a shift from “AI as a hype-led upside story” to “AI as a macro-financial transmission channel.” When a sector’s valuation is driven as much by narrative momentum as by operating leverage, small disappointments can trigger broad repricing across capital markets. The practical lesson for finance leaders is to stop treating AI as a siloed innovation theme. Build policy, credit, and risk checks that assume slower monetization, tighter financing conditions, and investor sentiment that can flip from euphoric to defensive at short notice. The lesson hidden in two very different headlines The prompt about an AI bubble collapse and the debate around SpaceX’s IPO both point to one idea: expectations are now a financial instrument in their own right. The first headline asks what happens if AI valuation optimism unwinds, while the second argues that AI outcomes will shape ordinary Americans’ financial futures. Put together, they suggest market narratives are no longer abstract commentary—they are balance-sheet events. From a finance perspective, this matters because narratives affect: Earnings multiples companies can command before proving revenue durability. Credit pricing as lenders reassess sector cashflow stability. Household allocation behavior when the public links retirement and income security to headline AI winners. In practical terms, risk is spreading from “can these firms innovate?” to “can the ecosystem keep rewarding growth longer than it can fund itself?” Why “bubble” language still misses the real trigger A bubble is often a mismatch, not a miracle A classic bubble warning is not necessarily a sudden stop in technology progress. It is usually a mismatch between valuation assumptions and the speed of monetization. AI-heavy firms can look expensive because investors pay for future optionality, but optionality is hard to convert into operating leverage when hiring, compute costs, and customer conversion remain uncertain. This distinction matters for finance teams: if risk committees only monitor headline margins and revenue growth, they may miss the more subtle pressure point—durable willingness of capital

From Hype to Household Leverage: Why AI Risk Is Becoming a Balance-Sheet Problem

TL;DR: The real issue behind today’s AI headlines is not a simple bull-versus-bear debate; it is a financing and transmission question. The first headline’s bubble framing asks what happens when valuation narratives outrun cash flow. The second asks whether a major AI-linked mega-IPO can make ordinary households more financially exposed to AI cycles than they realize. Put together, the risk is this: AI shocks can move from private fundraising and valuations to public wealth, retirement assets, and credit conditions faster than typical market cycles suggest. The headlines are two angles on one system The first piece, framed as a “what if the AI bubble popped,” should be read as a stress-test prompt, not a crash forecast. The second, from a major newspaper on SpaceX’s IPO trajectory, is a concentration test for household finance. Both are coherent once you see AI as a liquidity network rather than a pure technology story. A useful entry point is this chain: private AI financing influences venture and debt markets, those shifts influence public expectations, and expectations then filter into valuations, payroll strategies, and consumer confidence. As the AI-bubble framing article suggests, and as the IPO headline raises a broader audience risk story. What an AI bubble pop would likely look like in practice Narrative first, cash-flow second Classic bubbles are not obvious at the start. They become obvious once revenue and margin stories cannot keep up with the capital already invested. In AI, this dynamic can be amplified because the narrative has often outrun three elements that usually con

Beyond the Bubble Narrative: How AI Concentration, Not Headlines, Should Drive Positioning in Public Markets

TL;DR: The biggest AI question for finance readers is less "is the bubble real?" than "can the system reprice AI risk without destabilizing portfolios." The two headlines point to the same structural issue: when AI expectations become concentrated in a few channels, both panic and euphoria can move markets faster than fundamentals. Treat AI exposure as infrastructure risk—liquidity, governance, and cash-quality—not just top-line growth, and you can use fear and confidence extremes to improve positioning rather than react emotionally. AI commentary is noisy because people default to binaries. One side says everything is overvalued and will collapse; another side says AI will define the next decade and never look back. Both can be wrong for the same reason: each ignores transition risk. The value question is not whether AI is a good long-term force; the hard question is whether capital can be allocated efficiently across the full chain of development, deployment, and monetization. Why AI headlines are a stress test for portfolio process The "AI bubble" framing is less a prediction than a reminder that valuation discipline can drift when capital cycles become narrative-driven. In other words, price can detour from durable value for a while, but process still governs long-term survival. Concentration matters more than sentiment headlines In AI cycles, return dispersion is often low across mega-theme names and high beneath the surface. If most market beta depends on a small subset of companies, any policy, execution, or sentiment shock to that subset can spill into broad liquidity conditions. This is not a prediction engine statement; it is basic market plumbing. Public-story dependency creates policy sensitivity The [SpaceX-related AI-linked IPO framing](https://news.google.com/rss/articles/CBMieEFVX3lxTE1NQXhPQzdPQlR4Q2ZJUnpqckZLUEJqNlpUbjlVLVBBQ2M2WUpzRDVEOVllZW54NVhGdHE0Y1huSnpLdER6alZlYXdvTzkxNHg2VkxDOUJUbEdITFBEckc0VHNTOTh0T2RLUGVwWXdyZ3VUV

Columbus McKinnon's Kito Crosby Deal Moves The Test To The Balance Sheet

TL;DR: Columbus McKinnon reported strong fiscal 2026 demand after closing the Kito Crosby acquisition, with record orders and a much larger backlog. The useful investor read is not simply that industrial lifting equipment is healthy. It is that the company has moved from proving demand to proving integration math: debt, preferred equity, interest expense, amortization, and working-capital discipline now decide whether bigger scale becomes better equity value. #What Columbus McKinnon Actually Reported Columbus McKinnon, the Nasdaq-listed maker of hoists, crane components, lifting hardware, securement products, and industrial motion systems, posted a bigger business on June 4 because it is now digesting Kito Crosby. The company said fiscal 2026 orders rose 20% to a record $1.2 billion, while fiscal 2026 net sales rose 24% to $1.2 billion. Fourth-quarter orders reached $442.8 million, and backlog ended March 31, 2026 at $519.6 million. That sounds like a clean industrial-demand story. It is not that clean. The same release also included a $238 million fourth-quarter net loss, a $200 million non-cash goodwill impairment tied to the company's sustained stock price decline, $36.8 million of inventory step-up amortization, and $68.1 million of deal-related costs. The quarter is a reminder that acquisition scale arrives on the income statement before it becomes operating trust. #Why The Backlog Is Only Half The Story The warehouse scene is easy to picture. A customer needs hoists, slings, crane parts, or below-the-hook lifting gear because a plant, warehouse, shipyard, energy project, or fabrication shop cannot move heavy materials with a spreadsheet. That kind of demand is real. It is also not the whole investment case anymore. What changed after Kito Crosby closed? Columbus McKinnon completed the Kito Crosby acquisition on February 3, 2026, adding a large lifting and securement platform to its existing i

Revolut's U.S. Bank Plan Turns Stablecoins Into Deposit Features

TL;DR: Revolut's U.S. stablecoin push matters because it treats stablecoins as a checking-account feature, not a separate crypto gamble. Once a fintech wants the charter, the deposit, and the customer app all at once, the business stops looking like speculative finance and starts looking like a fight over who owns the cheapest balance sheet and the fastest money movement. The interesting scene is not a trader staring at token prices. It is a customer opening one app and seeing insured cash, cross-border transfers, and stablecoin tools sit next to each other as ordinary account features. Reuters reported on June 3 that Revolut's U.S. bank plans to offer stablecoin services alongside FDIC-insured products such as checking and high-yield accounts, which is a much bigger commercial signal than another crypto rollout headline. Reuters via The Block The second scene is more bureaucratic and more important. The FDIC's pending de novo list now includes Revolut, PayPal, Mercury, Nubank, Affirm, Upstart, and others, which tells you the real race is not just about user growth. It is about getting closer to deposits, settlement, and fee pools without renting so much infrastructure from partner banks. FDIC The Real Product Is The Balance Sheet Revolut's own OCC application is unusually blunt about the logic. The proposed bank says it wants to provide services to U.S. customers "at lower cost and with greater efficiency" than its current partner-bank model, and it wants to fold deposits, credit, FX, investment tools, and digital-asset features into one app. OCC application That is the tell. Stablecoins are being marketed as innovation, but the commercial prize is cheaper funding, better payment economics, and tighter customer retention. If a fintech can keep your paycheck, your debit card, your travel FX, your remittance flow, and your stablecoin balance in

Travelers Wedding Claims Put Vendor Deposits On The Insurance Desk

TL;DR: Travelers' 2025 wedding insurance claims data says vendor-related problems caused 55% of paid wedding insurance claims for the fifth straight year. The business implication is not romantic at all: weddings have become small, concentrated supply chains where households prepay multiple vendors months ahead, then discover that the real financial risk sits in contracts, deposits, weather timing, and proof-of-insurance workflows. #What Travelers' Wedding Claims Data Actually Shows Travelers said on June 1, 2026 that vendor-related issues were the leading cause of paid wedding insurance claims in 2025, representing 55% of claims. Illness or injury accounted for 16%, extreme weather for 10%, accidental damage or injury for 6%, and military deployment for 3%. That is a useful insurance statistic. It is also a cleaner consumer-finance signal than another survey about how expensive weddings feel. The overlooked point is simple: the largest risk is not the single big check. It is the chain of small counterparties around the event. A venue deposit goes out. A catering invoice follows. A photographer, rental company, florist, travel block, rehearsal dinner, and liability requirement all become separate promises. One vendor failure can force a household to replace capacity quickly, usually at a worse price and with less bargaining power. #Why This Is A Deposit-Risk Story, Not A Wedding Story The Knot's 2026 Real Weddings Study put the average U.S. wedding cost at $34,200 for couples married in 2025. That number gets attention because it is large and easy to quote. But the insurance mechanism is more interesting than the average bill. The household is acting like a project-finance sponsor without calling it that. Money is committed before the service is delivered. Contracts are spread across vendors. Weather, illness, travel problems, and venue rules can change the economics after deposits are already sunk. The planner's desk is where the risk

Uniti's Fiber Notes Say Broadband Has Entered The ABS Era

TL;DR: Uniti's new $1.14071 billion Kinetic fiber securitization looks like a telecom financing footnote. It is actually a business-model reveal. Broadband buildout is being pushed onto the structured-finance desk, which means the real product is no longer just internet access. It is a stream of household payments and network uptime that can be packaged, reserved, and stress-tested like an asset-backed bond. #What Uniti Is Really Selling Uniti did not announce a normal corporate debt raise. It used a bankruptcy-remote subsidiary to launch secured fiber network revenue term notes backed by residential fiber assets and customer agreements across 10 states, with an anticipated repayment date in June 2033. The company also said it expects to enlarge the existing liquidity funding note facility and extend its maturity to match the new notes. That sounds technical because it is technical. It is also the point. When a broadband company funds growth this way, management is telling the market that fiber is mature enough to be financed like an income stream instead of a speculative build story. The network still matters, but the underwriter now cares just as much about monthly collections, churn, reserve coverage, and service continuity as about trenching and strand miles. #Why This Matters More Than A Telecom Headline Uniti is not a tiny experiment in rural broadband anymore. In its March 31, 2026 10-Q, the company said it had approximately 240,000 fiber route miles across 47 states, served more than 1.0 million customers, and had 564,000 residential fiber customers with 1.9 million fiber-equipped households. That scale helps explain why the company thinks securitization can work. So does the operating profile. In first-quarter 2026 results, Uniti said Kinetic generated [$548.0 million of revenue, $235.5 million of contribution margin, and $251.9 million of capital expenditures](https://investor.uniti.com/news-releases/news-release-details/uniti-group-inc-report

REPAY's KUBRA Deal Says The Best Fintech Rails May Be The Bills

TL;DR: REPAY closed its $372 million cash acquisition of KUBRA on June 1, 2026, and the interesting part is not plain fintech dealmaking. It is a portfolio shift toward the kind of payment flow people do not casually cancel: utility bills, government payments, insurance notices, and other recurring obligations. In payments, the safer moat may be the unavoidable invoice. #What REPAY Actually Bought Most payments stories get told from the checkout page forward. More taps. Faster authorization. Better conversion. That is real, but it is also crowded. KUBRA lives in a different corner of the stack. When REPAY first announced the deal on March 30, it said KUBRA serves some of the largest utility, government, and insurance entities in North America, reaches over 40% of households in the U.S. and Canada, serves more than 250 clients, and helps create a combined company with more than $130 billion in annual payment volume. That is not a shopping-cart asset. It is an invoice-and-reminder asset. The distinction matters because bills behave differently from discretionary spend. A consumer can abandon a retail cart. A household can postpone buying sneakers. It is much harder to ignore the power bill, the water bill, the insurance premium, or the government notice that keeps showing up. #Why Bill Pay Is A Different Payments Business The strongest payment rails are often the least glamorous ones. Picture the moment KUBRA really owns. A customer opens a utility email after dinner, clicks into a familiar portal, checks the amount due, toggles autopay, and closes the laptop. Nobody calls that fintech magic. But from a business standpoint, it is a remarkably sticky workflow. The payer is not browsing. The biller is not begging for attention. The transaction is tied to an ongoing service relationship that the household needs to keep active. That produces better commer

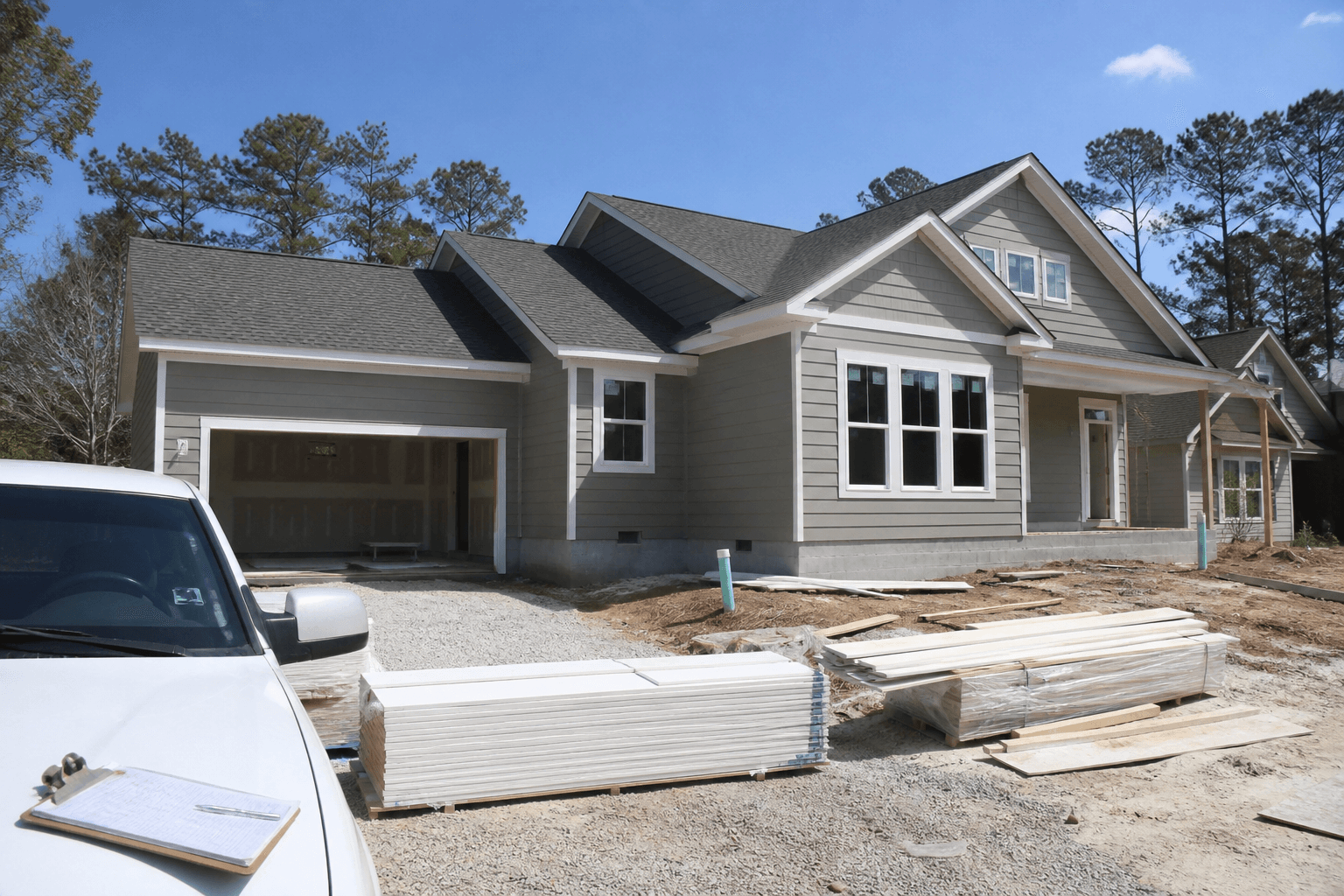

Construction Spending Is Hiding a Finish-the-Backlog Economy

TL;DR: The June 1, 2026 Census construction spending release looked decent on the surface: total spending rose 0.4% in April to a $2.172 trillion annual rate. The more useful business read is narrower. Housing completions and public work are still keeping dollars moving, but private nonresidential spending slipped and new home sales are slowing. This is starting to look less like a broad building boom and more like a finish-the-backlog economy. #The headline says growth. The mix says caution. It is easy to look at a higher construction spending number and say the U.S. building machine is still humming. That is not quite what the April data says. The same Census release that showed total construction spending up 0.4% also showed private residential spending up 0.8% and private nonresidential spending down 0.2%. Public construction also rose 0.4%, with education and highways both positive. That mix matters because it tells you where money is actually being released. Homebuilders are still turning prior starts into finished product. Governments are still funding roads and schools. But the corporate side of the building economy is no longer moving with the same confidence. The lazy read is that construction is resilient. The better read is that construction is still billing, while fresh private appetite is becoming more selective. #The housing site still looks busy for a reason On an ordinary suburban job site, the difference is hard to miss. The siding is on. The driveway gravel is down. Materials are stacked out front. The house looks active because it is close to the finish line, not because the builder suddenly wants to break ground on three more streets. That is exactly what the April housing data suggests. The April new residential construction report showed housing starts falling 2.8% from March to a 1.465 million annual rate, while housing completions rose 4.8% to 1.449 million. Single-famil

Salesforce's AI Story Just Picked Up a Treasury Cost

TL;DR: Salesforce's quarter was good enough to brag about product momentum and soft enough to require balance-sheet help. That is the real signal. When a software company says AI is working but also leans on a $25 billion debt-funded accelerated buyback that cuts full-year cash-flow growth guidance to roughly 4% to 5%, the market is no longer grading the story like early-stage magic. It is grading it like a mature capital-allocation problem. Picture two rooms inside the same company. In one, product teams are showing off AI adoption: Salesforce reported record first-quarter fiscal 2027 results on May 27, with revenue of $11.1 billion and raised full-year revenue guidance, while highlighting growing AI usage and product activity in its release (Salesforce). In the other, the treasury team is staring at the cost of convincing public investors to wait. That same release said operating cash flow growth and free cash flow growth guidance were cut to about 4% to 5% because of the impact of a $25 billion debt issuance tied to an accelerated share repurchase, or ASR (Salesforce). The interesting part happened at the treasury desk The easy headline is that Salesforce beat and still disappointed. Reuters reported that the company guided second-quarter revenue below Wall Street expectations and that investors remain worried AI tools could pull work away from traditional software products (Reuters via KELO). That reaction matters more than the usual one-day stock move. It says the software market has entered a different phase. Investors are no longer asking only whether a company can bolt AI onto the product. They are asking whether AI can protect pricing, defend renewals, and keep seat-based economics from getting quietly negotiated downward. That is why the buyback matters. Salesforce's latest 10-Q shows the board authorized $50 billion of repurchases in February and that the company already made $25

The SEC's Form 10-S Proposal Turns Quarterly Disclosure Into a Market Signal

TL;DR: The SEC's May 2026 proposal to let U.S. public companies replace three quarterly Form 10-Qs with one semiannual Form 10-S looks like a reporting-cost story. The sharper finance implication is different: if adopted, disclosure cadence becomes a live market signal. Companies that keep quarterly detail may be buying trust; companies that opt out may save process cost but invite a wider information discount. #What the SEC Form 10-S proposal would actually change The SEC proposed amendments on May 5, 2026 that would allow domestic public companies to elect semiannual interim reporting instead of the current quarterly Form 10-Q rhythm. The mechanics matter. The proposal would create a new Form 10-S for the first six months of the fiscal year, while the annual Form 10-K would remain. Quarterly reporting would remain the default unless a company affirmatively opts into semiannual reporting. That sounds administrative. It is not just administrative. Public markets are partly a trust machine. A company does not only sell earnings. It sells measurement, cadence, comparability, and the feeling that outside investors are not always the last people in the room to learn what changed. #Why disclosure cadence would become a valuation signal The tempting argument is that fewer mandatory reports would free managers from short-termism. There is some truth there. A thin-margin manufacturer, a newly public software company, or a small-cap healthcare business can burn real time preparing quarterly disclosure. But investors will not stop wanting quarterly information because the SEC gives issuers a checkbox. The checkbox is really a trust choice Imagine an investor relations team on the Monday after a rough quarter. The CFO, controller, outside counsel, and audit partner are looking at the calendar. Under today's regime, the company has to file the 10-Q. Under the proposed regime, if the company has elected Form 10-S, the formal filing clock may be quieter. The market clock will not be. Customers may have slowed. Gross margin