Construction Spending Is Hiding a Finish-the-Backlog Economy

TL;DR: The June 1, 2026 Census construction spending release looked decent on the surface: total spending rose 0.4% in April to a $2.172 trillion annual rate. The more useful business read is narrower. Housing completions and public work are still keeping dollars moving, but private nonresidential spending slipped and new home sales are slowing. This is starting to look less like a broad building boom and more like a finish-the-backlog economy.

##The headline says growth. The mix says caution.

It is easy to look at a higher construction spending number and say the U.S. building machine is still humming.

That is not quite what the April data says.

The same Census release that showed total construction spending up 0.4% also showed private residential spending up 0.8% and private nonresidential spending down 0.2%. Public construction also rose 0.4%, with education and highways both positive.

That mix matters because it tells you where money is actually being released. Homebuilders are still turning prior starts into finished product. Governments are still funding roads and schools. But the corporate side of the building economy is no longer moving with the same confidence.

The lazy read is that construction is resilient. The better read is that construction is still billing, while fresh private appetite is becoming more selective.

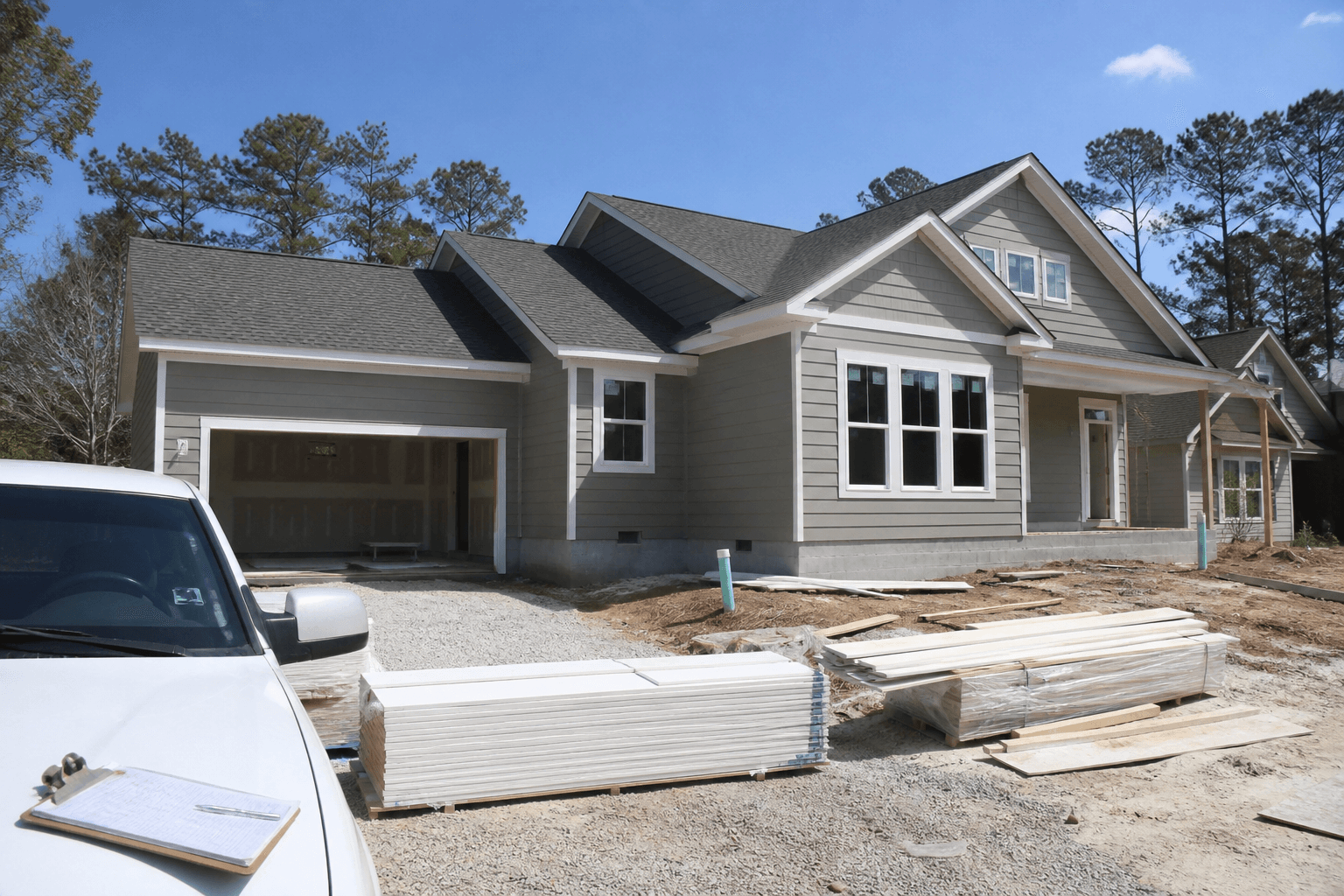

##The housing site still looks busy for a reason

On an ordinary suburban job site, the difference is hard to miss. The siding is on. The driveway gravel is down. Materials are stacked out front. The house looks active because it is close to the finish line, not because the builder suddenly wants to break ground on three more streets.

That is exactly what the April housing data suggests.

The April new residential construction report showed housing starts falling 2.8% from March to a 1.465 million annual rate, while housing completions rose 4.8% to 1.449 million. Single-family starts fell 9.0%, even though total permits increased 5.8%.

That is a very different message from a clean demand boom.

#Completions pay the bills faster than new starts

Finished or nearly finished homes turn into closings, draws, supplier payments, and revenue recognition. Starts consume land, labor, and financing before the cash comes back.

When completions rise while single-family starts fall, builders are often choosing cash conversion over fresh risk. They are trying to harvest what is already in the pipeline before committing harder to the next batch of inventory.

##The sales desk is softer than the job site

The demand side reinforces the same point.

The April new home sales report showed sales falling 6.2% from March to a 622,000 annual rate. Inventory for sale rose to 489,000 homes, or 9.4 months of supply, while the median sales price climbed to $422,500.

This is where the business-model shift shows up. Builders are not only managing lumber, drywall, and subcontractors anymore. They are managing time on balance sheet.

If homes are taking longer to clear and months of supply is rising, the carrying cost of each completed house starts to matter more. The economics move away from pure volume and toward incentives, financing support, pricing discipline, and regional product mix.

#This is a working-capital story disguised as a housing story

A builder can post respectable spending activity and still feel tighter inside the business.

Land is financed. Materials are financed. Construction draws are financed. Unsold completed inventory is financed. The moment new home sales soften, the question changes from "Can we build?" to "How long do we want to hold what we built?"

That is why the April data matters beyond homebuilders. Banks, building-products companies, appliance makers, title firms, and local service businesses all depend on how quickly construction dollars turn into completed transactions.

##Why private nonresidential is the quieter warning

The more underappreciated part of the June 1 release may be the 0.2% decline in private nonresidential construction spending.

This is not a crash. It is something more useful for investors: a sign that the broad capex story is narrowing.

Public work can stay firm because funding was already appropriated. Residential can still print decent spending because projects already underway need to get finished. Private nonresidential is where CFO confidence shows up fastest, because that is where office, industrial, commercial, and other business projects have to keep earning fresh internal approval.

If that line keeps softening while headline spending stays positive, the U.S. building economy will look healthier than it really feels underneath.

##What the market is likely missing

The market tends to treat construction as one big cyclicality bucket. April's data argues for a more specific view.

- Homebuilders are increasingly being paid for finishing inventory, not for proving demand is broad.

- Public construction is cushioning the aggregate number, which makes the private economy look stronger than it is.

- Suppliers and lenders tied to fresh private project formation may feel pressure before the topline construction data turns obviously weak.

That is why this release matters now. A finish-the-backlog economy can still produce respectable revenue for a while. It just does not create the same next-quarter demand signal.

The building economy is still working. The question is how much of that work is tomorrow's growth, and how much is yesterday's commitment finally getting invoiced.

#FAQ

Why is higher construction spending not automatically bullish?

Because the composition matters. April 2026 spending was lifted by residential and public construction, while private nonresidential slipped. That can mean money is still being spent without signaling broad new corporate confidence.

Why do completions matter more than starts in this article?

Completions convert pipeline into revenue and cash faster. When completions rise while single-family starts fall, builders may be prioritizing balance-sheet turnover over new speculative growth.

What is the main Gainbrief takeaway for investors?

The April construction data points to a narrower building economy than the headline suggests. Companies tied to finishing projects and public work may hold up better than businesses that need a fresh wave of private corporate building demand.