Travelers Wedding Claims Put Vendor Deposits On The Insurance Desk

TL;DR: Travelers' 2025 wedding insurance claims data says vendor-related problems caused 55% of paid wedding insurance claims for the fifth straight year. The business implication is not romantic at all: weddings have become small, concentrated supply chains where households prepay multiple vendors months ahead, then discover that the real financial risk sits in contracts, deposits, weather timing, and proof-of-insurance workflows.

##What Travelers' Wedding Claims Data Actually Shows

Travelers said on June 1, 2026 that vendor-related issues were the leading cause of paid wedding insurance claims in 2025, representing 55% of claims. Illness or injury accounted for 16%, extreme weather for 10%, accidental damage or injury for 6%, and military deployment for 3%.

That is a useful insurance statistic. It is also a cleaner consumer-finance signal than another survey about how expensive weddings feel.

The overlooked point is simple: the largest risk is not the single big check. It is the chain of small counterparties around the event.

A venue deposit goes out. A catering invoice follows. A photographer, rental company, florist, travel block, rehearsal dinner, and liability requirement all become separate promises. One vendor failure can force a household to replace capacity quickly, usually at a worse price and with less bargaining power.

##Why This Is A Deposit-Risk Story, Not A Wedding Story

The Knot's 2026 Real Weddings Study put the average U.S. wedding cost at $34,200 for couples married in 2025. That number gets attention because it is large and easy to quote.

But the insurance mechanism is more interesting than the average bill.

The household is acting like a project-finance sponsor without calling it that. Money is committed before the service is delivered. Contracts are spread across vendors. Weather, illness, travel problems, and venue rules can change the economics after deposits are already sunk.

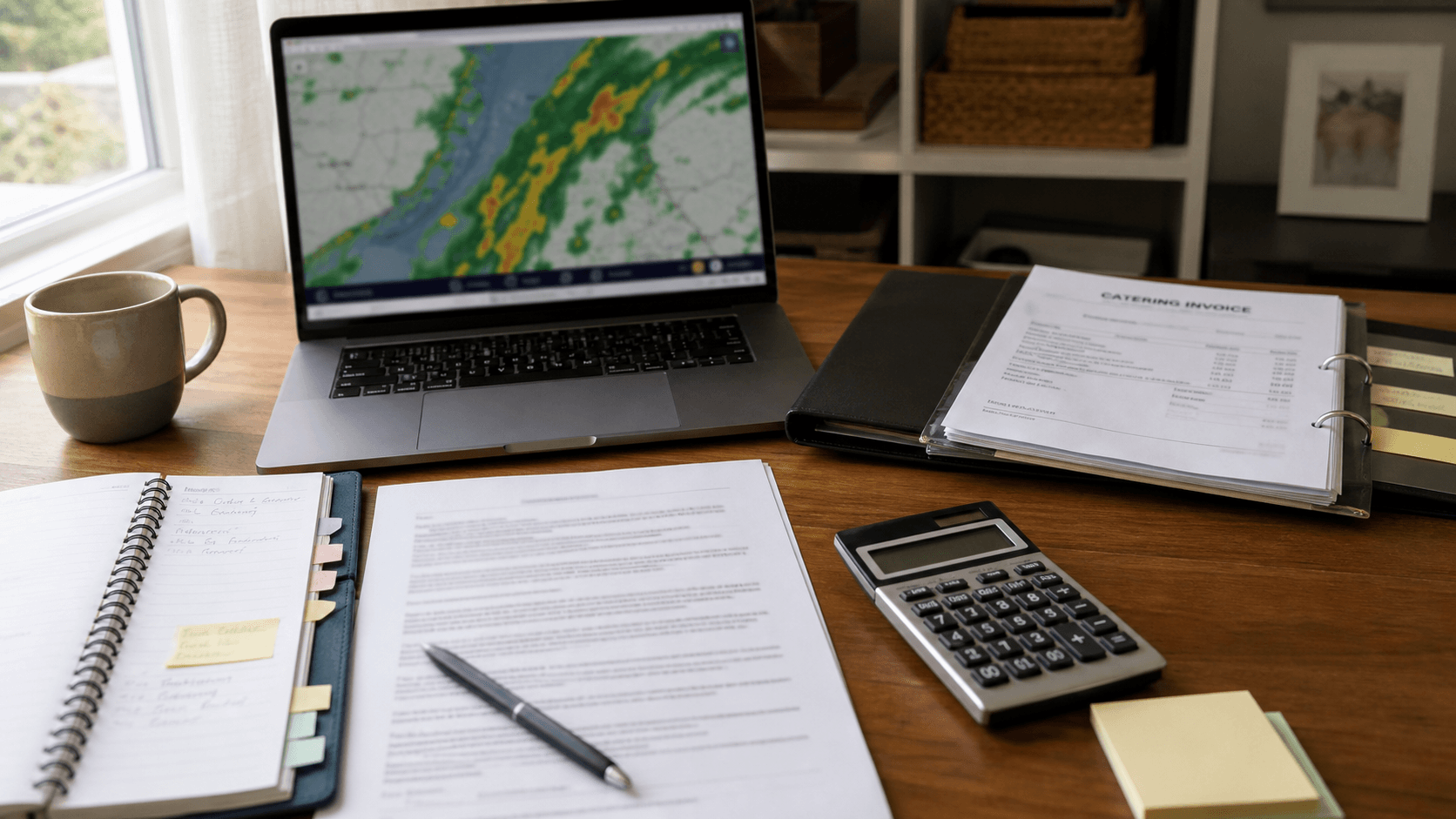

#The planner's desk is where the risk appears

Picture the boring desk before a Saturday wedding: a laptop open to a weather map, a venue contract with tabs, a catering invoice, a calculator, and a note that proof of insurance is due before the final walkthrough.

Nothing in that scene looks like Wall Street. But the logic is familiar.

Someone has already paid. Someone else has promised performance. If the handoff fails, the replacement cost is higher than the planned cost because time has become scarce.

That is why vendor failures showing up as 55% of paid claims matters. It suggests the weak point in the event budget is not extravagance. It is counterparty reliability.

##Where Specialty Insurance Finds Its Quiet Growth

Travelers is not a wedding company. It is a property-casualty insurer, and it reported nearly $49 billion of revenue in 2025 in the same release. Wedding insurance is tiny next to auto, home, business insurance, and bond lines.

Tiny does not mean irrelevant.

Specialty personal lines work when the customer can see a narrow, expensive failure mode at the exact moment money is being committed. A couple may not think in actuarial terms. They do understand the feeling of wiring a venue deposit and wondering what happens if the caterer disappears, a storm closes roads, or a family illness forces a change.

For insurers, that creates a product with a clear trigger:

- the insured event is specific;

- the purchase moment is tied to a deposit;

- the distribution channel can run through planners, venues, agents, and online quote flows;

- the claim story is easy for customers to understand before they buy.

The product does not need to be glamorous. It needs to sit close to the cash-flow moment.

##Who Actually Pays When The Vendor Chain Breaks

The first loser is usually the household, because deposits and replacement costs hit before reimbursement is available. The second loser can be the venue or planner, because a failed vendor turns into a service problem even when the venue did nothing wrong.

The third player is the insurer, which has to price a risk that looks mundane until a cluster of vendor failures, weather events, or liability incidents hits the same season.

#Why venues quietly care about the policy

Many venues do not want to underwrite guests' liability, alcohol-related incidents, property damage, or cancellation fights through goodwill. They want proof that a third party is standing behind the event.

That moves wedding insurance from "optional add-on" to part of the operating checklist. The policy becomes a risk-transfer document that helps the venue protect its own calendar, staff, and insurance program.

This is the part casual readers miss. The buyer may think the policy protects a beautiful day. The business system uses it to protect deposits, capacity, and liability allocation.

##What Investors Should Take From The Data

This is not a call that wedding insurance will move Travelers' stock by itself. It will not.

The more durable lesson is about product design in insurance. The best small policies often attach to a moment when consumers can name the specific thing that might go wrong. A vague fear is hard to monetize. A venue deposit, storm deadline, and vendor contract are much easier.

That is why this data belongs on a finance site. It shows how personal insurance can grow by turning household events into priced operational risk, one boring checklist at a time.

#FAQ

Why did Travelers' wedding claims data matter for finance readers?

Because it showed that vendor issues, not abstract wedding inflation, were the largest paid-claim driver in 2025. That points to counterparty and deposit risk inside household spending.

Is wedding insurance a major business line for Travelers?

No. It is small compared with Travelers' main property-casualty businesses, but it is a useful example of how specialty insurance attaches to narrow, high-stress consumer cash-flow moments.

What is the key business takeaway?

Weddings are not just emotional events. They are prepaid vendor networks, and prepaid vendor networks create insurable financial risk when time, weather, liability, and replacement costs collide.