Thoma Bravo's Kneat Deal Prices Life-Sciences Validation Workflows

TL;DR: Thoma Bravo agreed to buy Kneat for about C$650 million, and the interesting part is not the take-private premium. It is the kind of software being priced: digital validation and quality-process automation for life-sciences companies. In regulated pharma and medtech, workflow software can become sticky because replacing it means revalidating evidence, approvals, audit trails, and trust.

##What Thoma Bravo Is Really Buying In Kneat

Thoma Bravo's all-cash deal for Kneat values the company at roughly C$650 million, with shareholders set to receive C$6.50 a share if the transaction clears approvals.

That is the headline. The better business question is why a private-equity software buyer wants a company built around validation records, quality workflows, and life-sciences compliance.

Kneat is not selling a prettier spreadsheet. It is selling a system of record for work that regulated manufacturers cannot casually improvise.

#Why validation software is not ordinary SaaS

In a normal software budget, a department can replace a tool because a cheaper vendor appears, a contract expires, or a CFO wants consolidation.

In a regulated life-sciences plant, the decision is messier. The software touches evidence that a process, system, cleaning method, package line, or equipment setup was tested, approved, and controlled.

That makes the switching cost procedural, not just technical.

##Why The Validation Desk Has Pricing Power

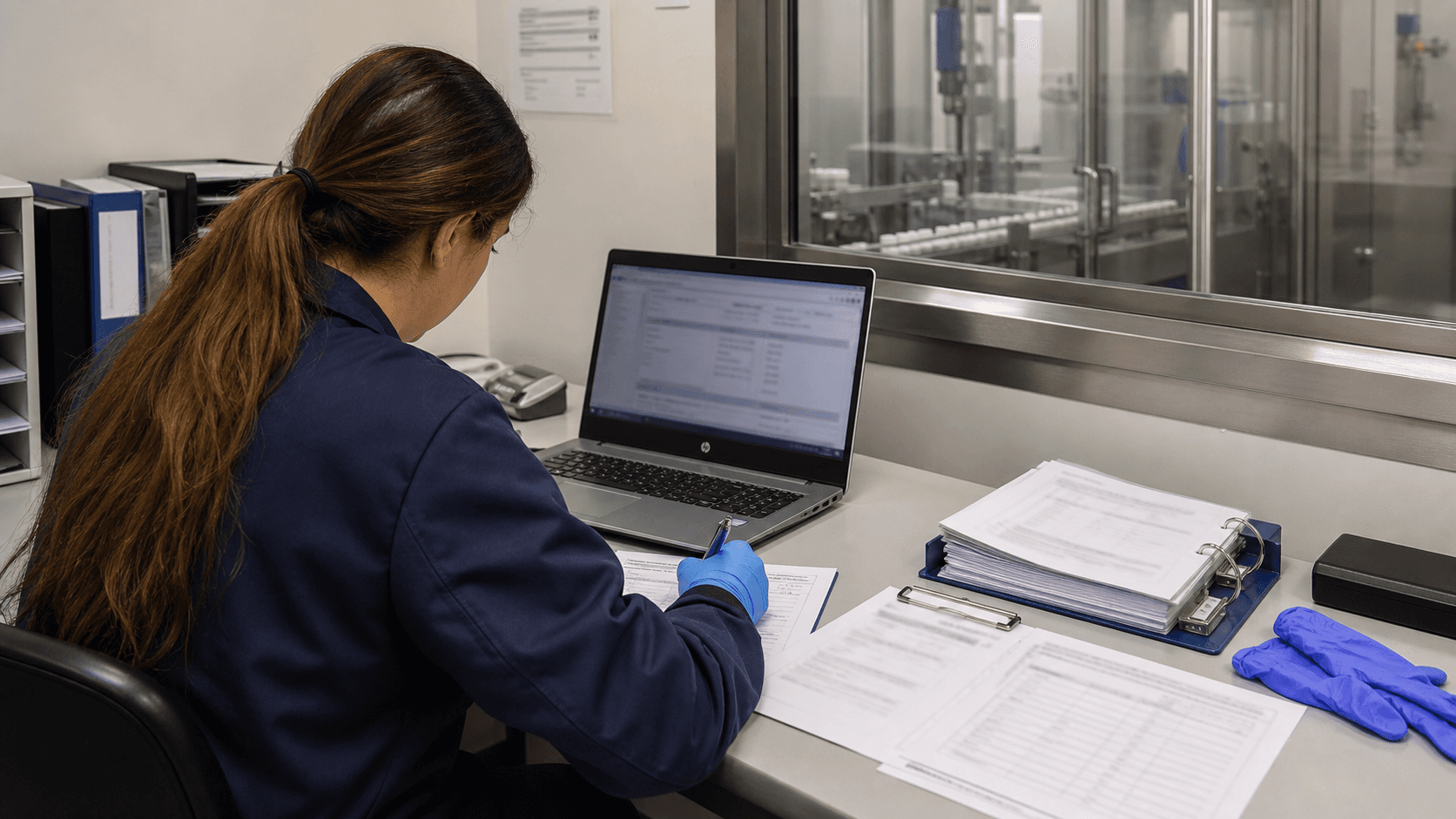

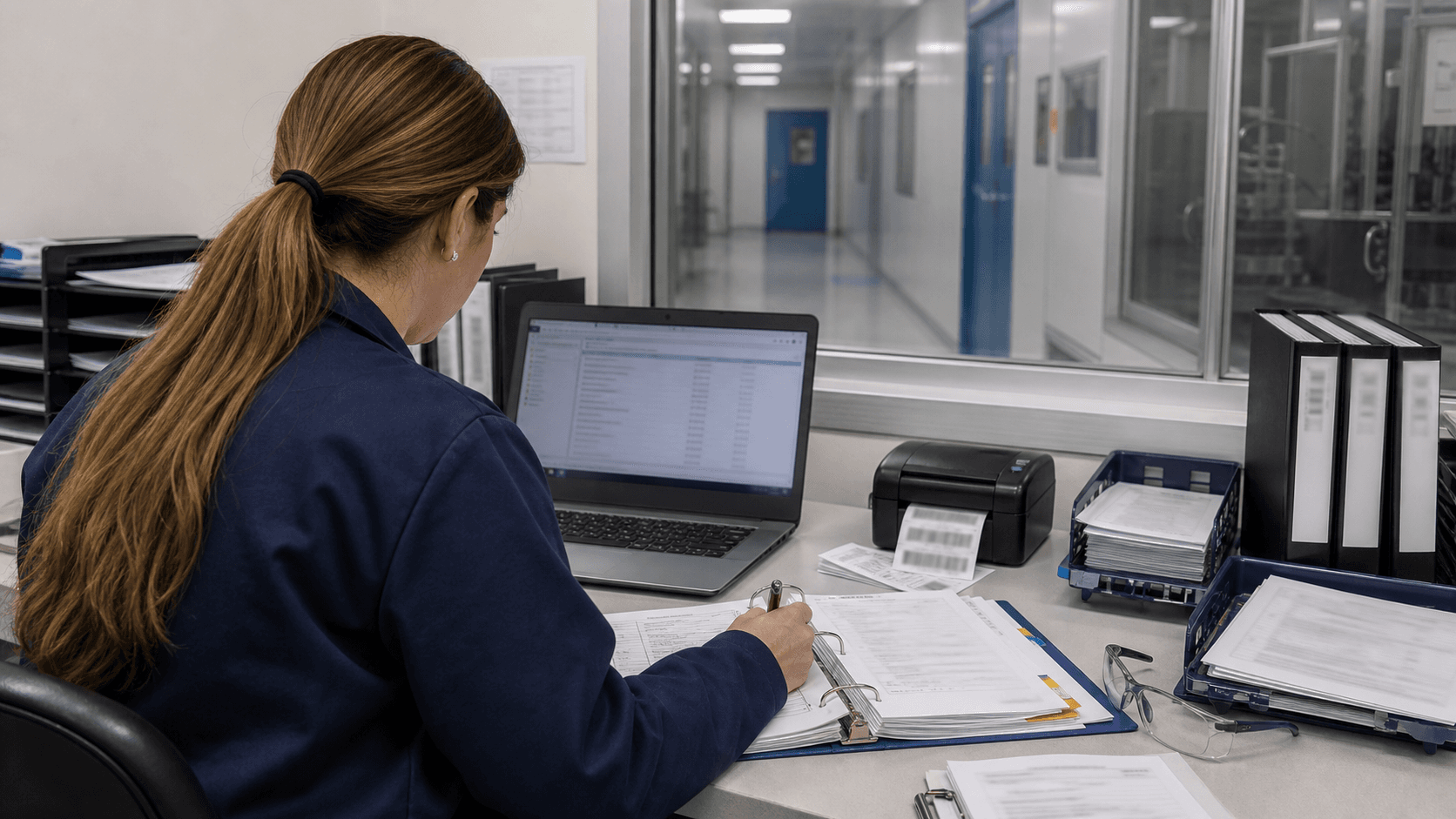

Picture a quality-assurance worker at a desk beside a cleanroom window. There is a laptop, a stack of validation forms, a binder, gloves, and a production line behind the glass.

The job is not glamorous. It is also not optional.

When a drugmaker or medtech company moves from paper-heavy validation to digital workflows, the buyer is trying to reduce manual handoffs, missing signatures, duplicate records, and audit scramble. Kneat says its platform is used by 8 of the world's top 10 life-sciences companies, which tells you where the value lives: inside large, regulated operating systems that hate uncertainty.

The private-equity math is straightforward only on the surface. Kneat reported Q1 2026 SaaS revenue of $16.5 million and annual recurring revenue of $76.4 million, both up 20% from a year earlier. Those are software numbers, but the reason they matter is the domain.

Compliance workflow revenue is not magic. It can still slow. It can still be repriced. But it has one advantage many horizontal SaaS categories lack: customers do not wake up eager to disturb validated processes.

##Where The Hidden Cost Sits

The underappreciated cost is not the license fee. It is the internal burden of proving the new system can be trusted.

FDA's Part 11 framework covers electronic records and electronic signatures when companies maintain or submit regulated records electronically; the agency's guidance discusses validation, audit trails, record retention, and electronic signatures as recurring areas of concern. That matters because software in this corner is part of the evidence chain, not merely a productivity layer.

For a regulated manufacturer, the buyer's checklist is not just:

- Does the software save time?

- Does it integrate with existing systems?

- Does it reduce paper and review cycles?

- Can the audit trail stand up when a regulator, customer, or internal quality lead asks who changed what, when, and why?

That last question is where workflow software becomes financial infrastructure.

#The buyer is often buying fewer exceptions

The strongest enterprise software rarely wins because it is exciting. It wins because it makes exceptions less expensive.

In life sciences, every manual workaround can become a future investigation, deviation, delay, or audit finding. A missed signature is not a tiny clerical issue if it slows a batch release or creates uncertainty around a validated process.

That is the commercial logic behind Kneat. The platform sits where quality, operations, regulatory affairs, and IT all have veto power. A vendor embedded there is harder to rip out than a dashboard that only one department loves.

##Who Should Care Beyond Kneat Shareholders

This deal belongs on the Gainbrief beat because it shows a more durable corner of software M&A.

The market spent the last few years arguing about AI seats, copilots, and generic productivity tools. Those categories can be huge, but they can also be crowded, bundled, and repriced quickly.

Regulated workflow software is a different animal. The moat is not only code. It is the customer's fear of breaking a controlled process.

That has implications for several groups:

- For private-equity buyers, vertical compliance software can offer a cleaner retention story than broad SaaS exposed to seat cuts.

- For public software investors, revenue quality may depend less on "AI attached" and more on whether the product sits in an auditable workflow.

- For life-sciences operators, digital validation is a cost-control project only if it reduces review delays without creating new compliance risk.

The deal is also a reminder that healthcare technology is not only doctors, insurers, and claims. A lot of money sits in the quiet machinery that helps regulated products move from facility to customer without losing the paperwork trail.

##What The Deal Says About Software Valuation

The easy interpretation is that Thoma Bravo found another vertical SaaS asset to optimize privately.

The sharper interpretation is that software valuation is becoming more dependent on where the software sits in the customer's operating risk.

If a tool lives at the edge of a workflow, it can be negotiated like a nice-to-have. If it lives inside validation, quality evidence, audit readiness, and batch-release confidence, the conversation changes.

The customer is not only buying efficiency. The customer is buying fewer moments where someone has to stop production, reopen a file, chase a signature, or explain a data trail under pressure.

That is not a glamorous software story. It is a better one.

#FAQ

Why did Thoma Bravo agree to buy Kneat?

Thoma Bravo agreed to acquire Kneat in a transaction valuing the digital validation and quality-process automation company at about C$650 million. The strategic appeal is Kneat's position in regulated life-sciences workflows, where customers need reliable records, approvals, and audit trails.

Why does validation software matter for investors?

Validation software can be stickier than ordinary productivity software because it becomes part of a regulated evidence chain. Replacing it may require process review, system validation, training, and audit-risk management.

Is this mainly an AI software story?

No. The Kneat deal is better understood as a vertical compliance workflow story. The financial point is that regulated operating risk can support durable software demand even when broader SaaS categories face budget pressure and bundling risk.