Medicare Is Turning GLP-1s Into a Carve-Out Business

The hottest obesity-drug story in America is not the next trial result. It is a payment design experiment hidden inside Medicare.

On May 6, CMS said eligible Medicare beneficiaries will be able to get certain GLP-1 medicines for $50 a month starting July 1, 2026, through December 31, 2027, under the Medicare GLP-1 Bridge. That sounds like a pricing headline. It is also a business-model headline, because CMS is not handling this like a normal Part D drug benefit.

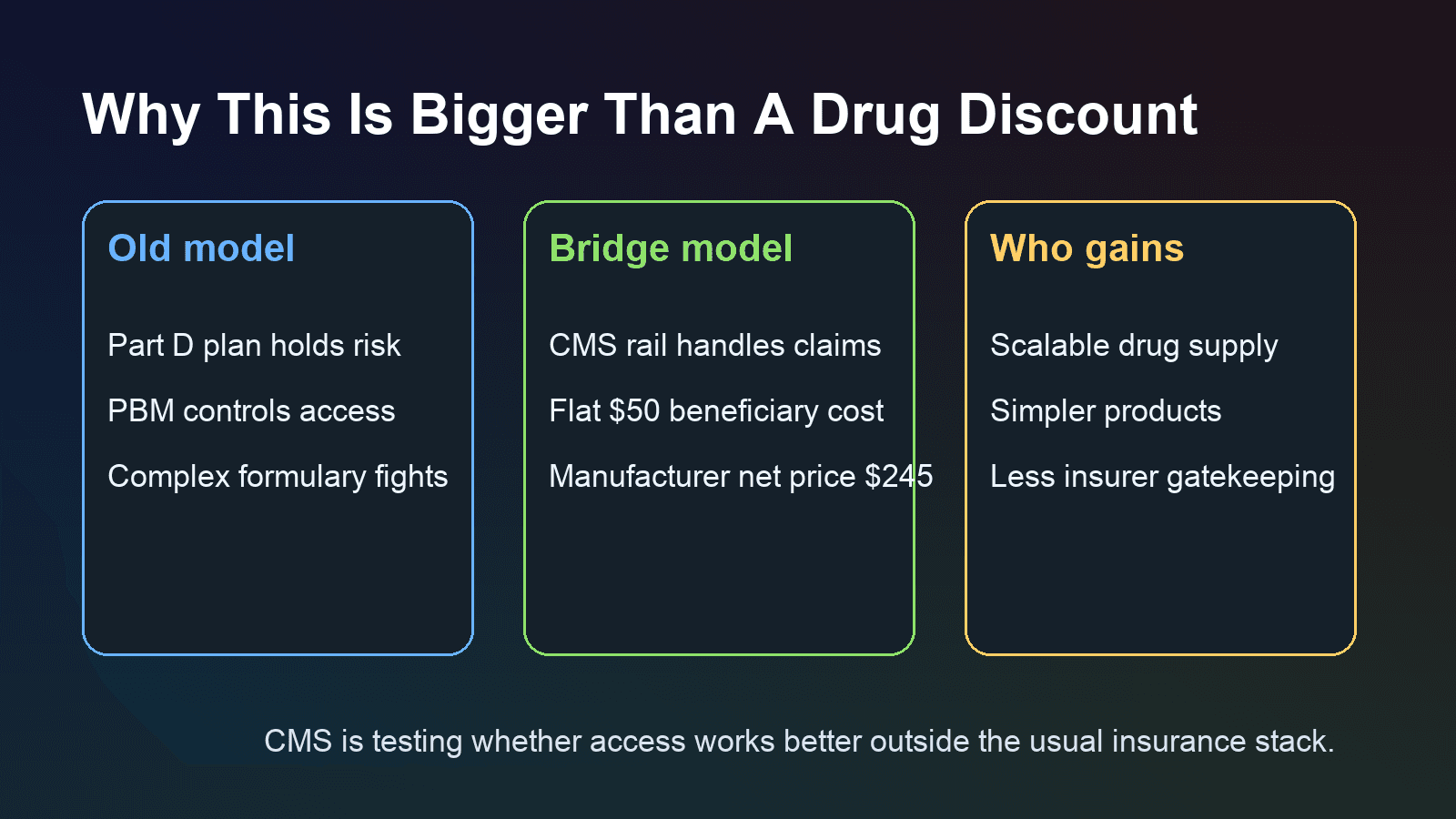

The important detail most casual readers are missing is that the Bridge operates outside the ordinary Part D coverage and payment flow. CMS said it will use centralized processes for claims adjudication and pharmacy payment, and its May 7 guidance said a central processor will handle prior authorization, claims processing, and pharmacy payment. On the Bridge FAQ page, CMS goes further: Part D sponsors will not carry risk for eligible GLP-1 drugs furnished through the program. That means Medicare is temporarily pulling one of the most expensive, politically sensitive drug categories out of the usual insurer and PBM control loop and testing a carve-out model instead.

That matters because it changes who owns the economics. In a standard drug benefit, health plans and pharmacy benefit managers manage formularies, utilization, and patient cost sharing. In the Bridge, participating manufacturers provide eligible drugs at a net price of $245 per monthly supply, the beneficiary pays a flat $50 copay, and the claim runs through a CMS-specific payment rail rather than the usual Part D flow. If this structure works operationally, the lesson for Washington will be bigger than obesity treatment: some high-cost therapies may be easier to expand by carving them out of insurance complexity than by asking plans to absorb more risk.

That is why the latest Lilly news matters as more than product chatter. On May 22, Lilly said its oral GLP-1 Foundayo produced up to 13% mean weight reduction in adults 65 and older without type 2 diabetes in a new analysis, and it highlighted that Medicare beneficiaries will be able to access Foundayo through the Bridge at a $50 monthly copay starting July 1. A simpler pill with fewer administration frictions is exactly the kind of product that becomes more powerful when the payer side is centralized. It reduces not only patient hassle, but also the operational mess that plans usually monetize through formularies, exceptions, and gatekeeping.

The commercial stakes are already large. Lilly reported first-quarter 2026 revenue of $19.8 billion, with key products generating $13.4 billion, led by Mounjaro and Zepbound. A day earlier, Lilly also posted pivotal Phase 3 obesity data showing retatrutide delivered 28.3% average weight loss over 80 weeks at the top dose. In other words, supply, product variety, and clinical efficacy are all moving in the same direction at the same time Medicare is experimenting with a new payment architecture.

This is why the Bridge could end up mattering even if it remains temporary. Investors often frame obesity drugs as a volume story for drugmakers and a cost problem for insurers. The Bridge suggests a third possibility: obesity treatment could become a carve-out utility, where the government standardizes access, manufacturers compete on supply and simplicity, and traditional plan managers lose some leverage over the most important part of the transaction.

There are still obvious constraints. Eligibility is limited. Drugs used for indications already coverable under the basic Part D benefit stay in the regular plan process. CMS will have to prove the central processor can handle prior authorization and pharmacy workflows smoothly. And if utilization surges, the budget pressure will become impossible to ignore.

But the strategic signal is already clear. Medicare is not just making GLP-1s cheaper for seniors. It is testing whether the fastest way to scale a politically popular therapy is to route around parts of the insurance stack. If that logic spreads, the real losers may not be rival drugmakers. They may be the intermediaries that used to control access.