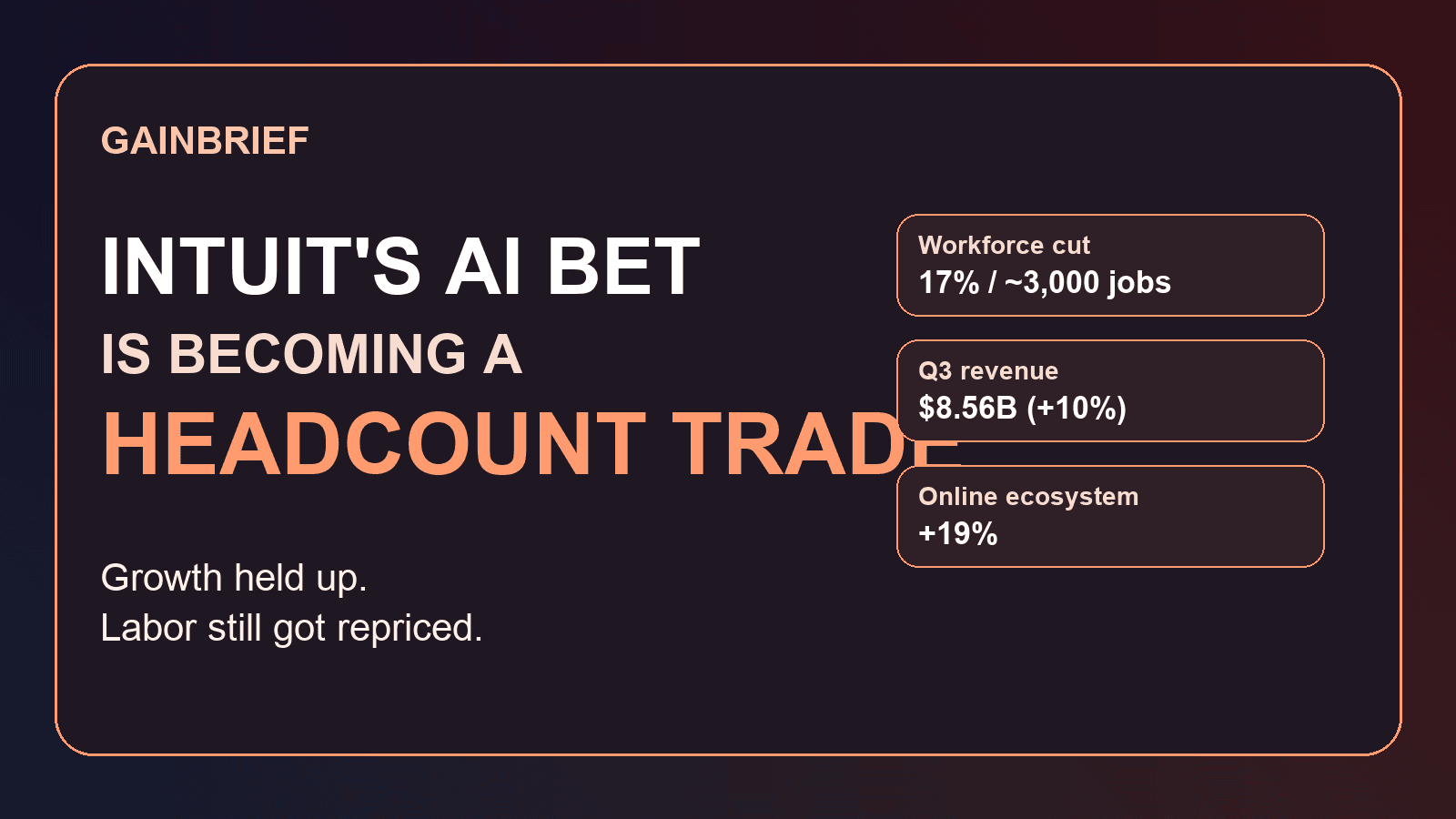

Intuit's AI Bet Is Becoming a Headcount Trade

Intuit delivered the kind of quarterly update public software companies usually want to celebrate. On May 20, the company raised full-year revenue guidance, reported third-quarter revenue up 10% to $8.56 billion, and said non-GAAP operating income grew 8% to $4.68 billion.

Then, on the same day, Reuters reported that Intuit planned to cut about 17% of its workforce, or roughly 3,000 employees, to sharpen focus on its biggest bets, including artificial intelligence. The stock fell anyway.

The thing most casual readers are missing is that this was not just a cost-cutting announcement sitting next to a decent earnings print. It was a signal that AI inside financial software is becoming a headcount story before it becomes a clean new revenue story. The key question is no longer whether companies like Intuit can add AI features. It is whether they can use AI to remove enough labor, service, and complexity fast enough to defend margins before AI makes parts of their legacy workflow less special.

That is a more uncomfortable shift than the usual software narrative. Investors were already worried that generative AI could weaken the pricing power of tax and accounting products by making advice, search, and form-filling cheaper. Reuters said those fears were one reason Intuit shares dropped after hours even as the company lifted guidance. Intuit's answer is increasingly to present itself not just as a software vendor with AI add-ons, but as a productivity machine that can reorganize around AI while competitors and customers are still figuring out what gets automated next.

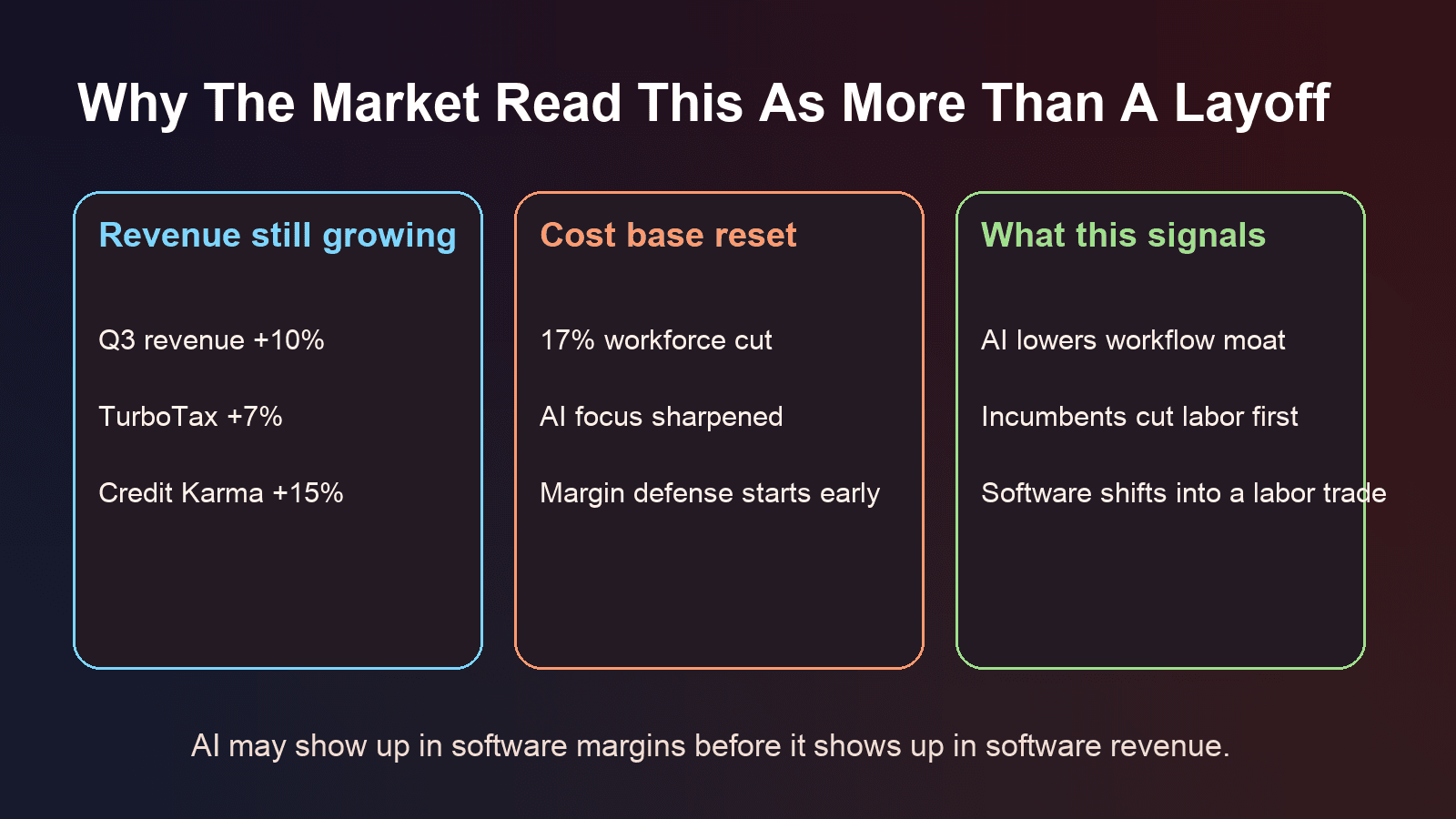

The quarterly numbers help explain why the company thinks it can make that move. Consumer revenue rose 8% to $5.3 billion, including 7% growth at TurboTax. Credit Karma grew 15% to $631 million. Intuit also said Global Business Solutions revenue increased 15%, with Online Ecosystem revenue up 19%. In other words, this is not a company cutting because demand suddenly collapsed. It is cutting while the business is still growing.

That matters because it changes how investors should read the restructuring. In an older software cycle, layoffs after a solid quarter might look like a one-time efficiency push. In this cycle, they look more like the operating logic of the business. If AI can handle more support, preparation, workflow routing, and product assistance, then a company that waits to reshape its cost base may discover that its margin structure is still human-heavy just as customers start expecting AI-enhanced service at software-like prices.

There is also a second-order implication for the broader fintech and enterprise-software market. The winners may not be the firms with the loudest AI demos. They may be the incumbents with enough distribution, data, and trust to use AI as a margin migration tool. Intuit has signed multi-year partnerships with OpenAI and Anthropic, according to Reuters, but the more revealing fact is what happened next: management paired the AI story with a major labor reset. That suggests the real commercial benefit of AI, at least in this stage, may be less about selling a brand-new product than about changing the cost structure of an old one.

This is why the market reaction was mixed. Raised guidance says the core franchise is holding up. The layoffs say management believes the core franchise still has to be rebuilt. Those two facts are not contradictory. They are the point. When a company with sticky products, seasonal tax demand, and growing small-business software revenue still decides to remove nearly a fifth of its workforce, it is telling investors that AI competition is already affecting how it allocates labor, even before it fully shows up in reported revenue.

That should make the Intuit story more interesting, not less. The bullish case is no longer simply that AI will help the company cross-sell more services or improve customer conversion. It is that Intuit can turn AI into a structural margin tool before AI turns more financial software into a lower-friction commodity.

If that reading is right, then this was not really an earnings story at all. It was a preview of what mature software companies may have to do when AI starts attacking workflow economics from the inside: keep the revenue engine running, cut the human scaffolding beneath it, and hope the market rewards the transition before customers start asking why the old pricing model still exists.