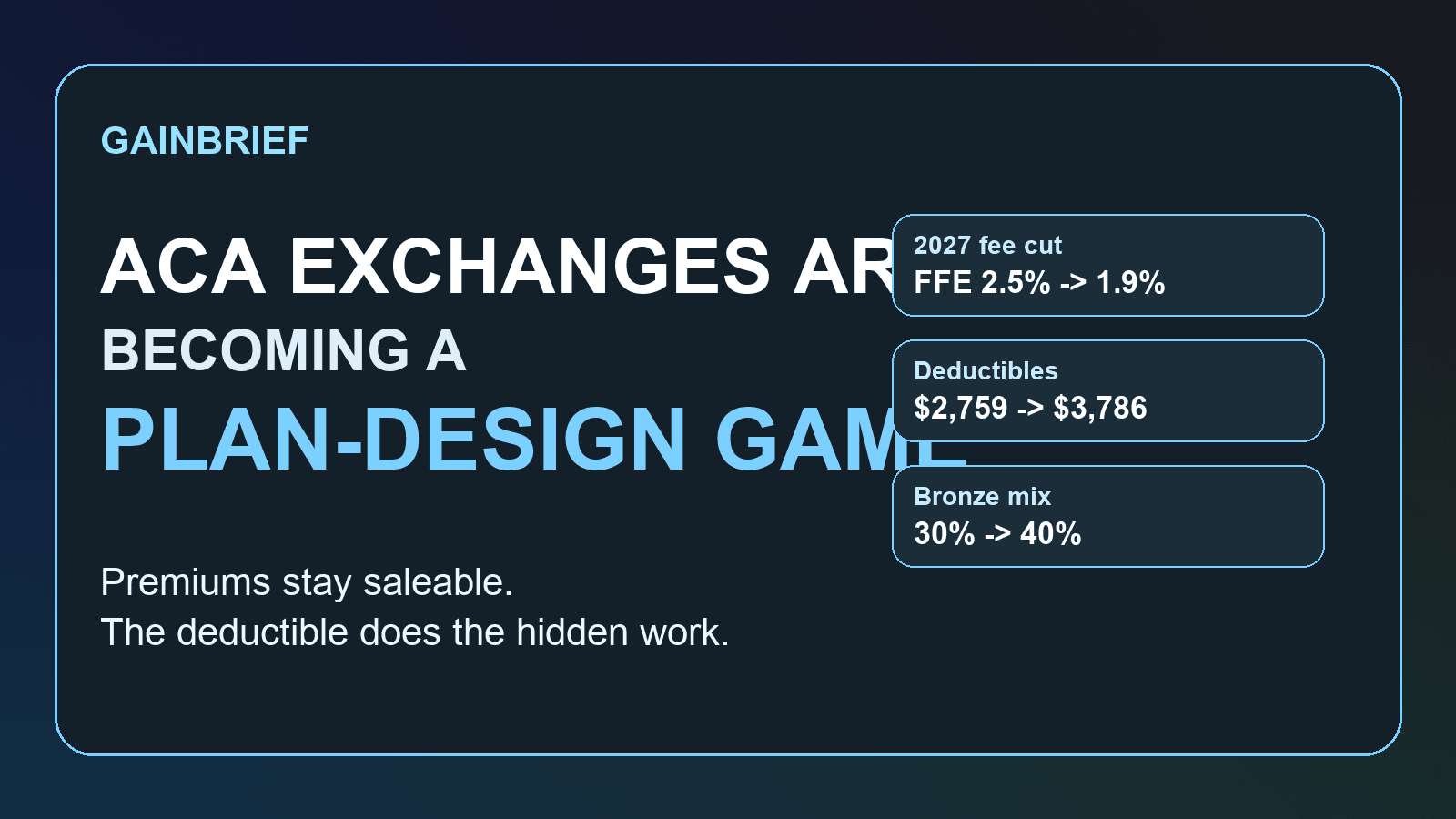

ACA Exchanges Are Becoming a Plan-Design Game

The newest Affordable Care Act exchange rule looks, at first glance, like housekeeping. On May 15, CMS cut federal exchange user fees for 2027, tightened eligibility checks, and gave insurers more flexibility in how they design marketplace plans.

That sounds like a regulator trying to trim costs and clean up enrollment. It is also a business story about how health insurers protect revenue when true affordability is getting worse.

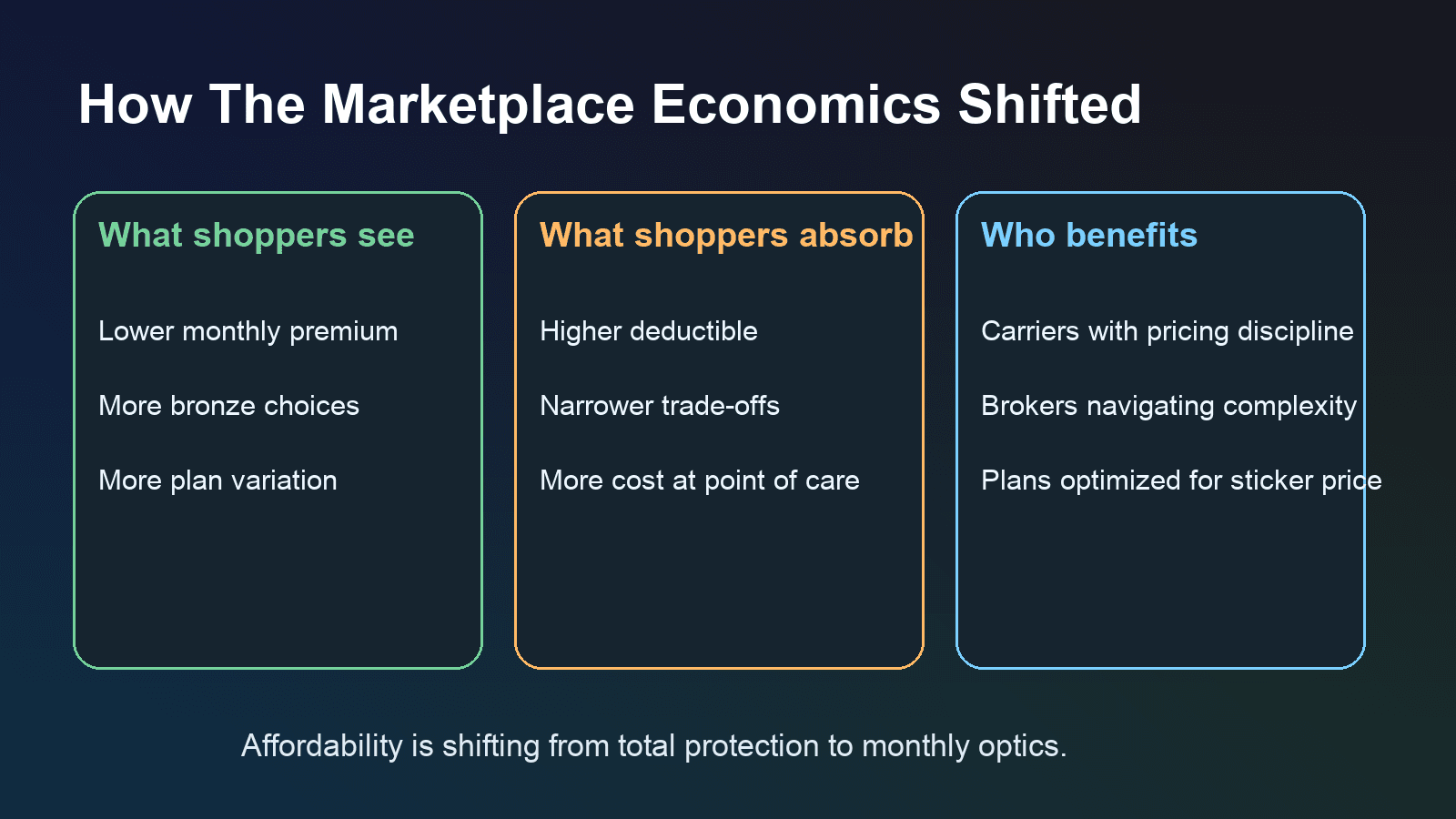

The thing most casual readers are missing is that the ACA marketplace is becoming less of a generosity contest and more of a plan-design contest. As enhanced subsidies disappear and consumers get squeezed, insurers do not need to make care meaningfully cheaper to stay competitive. They just need to make the monthly premium look survivable, even if the deductible gets pushed further into the future.

The recent numbers make that shift hard to miss. KFF said plan sign-ups fell to 23.1 million during the 2026 open enrollment period, and average effectuated enrollment could fall to about 17.5 million this year, potentially as low as 16.5 million, once nonpayment and attrition show up. At the same time, average monthly premium payments rose 58%, while average deductibles jumped 37% to a record $3,786. Bronze-plan selection climbed from 30% to 40% of enrollees, while silver fell below half for the first time.

That is not just a consumer pain story. It is a commercial roadmap. When households trade down from richer coverage to thinner coverage, carriers can preserve enrollment by selling a cheaper-looking front-end product while shifting more of the real cost to deductibles, narrower networks, and benefit design. In other words, the affordability crisis does not automatically destroy the marketplace business. It can actually reward insurers that are best at engineering a lower monthly sticker price.

That is why the new CMS rule matters more than the headline fee cut. Yes, lower exchange user fees should help somewhat: CMS said the federal fee will fall to 1.9% from 2.5%, and the fee for state-based exchanges on the federal platform will drop to 1.5% from 2.0%. But the more important move is structural. CMS is removing the requirement that HealthCare.gov insurers offer standardized plan options and is also removing limits on the number of non-standardized plans they can sell.

That opens the door to a familiar insurance tactic: compete less on making coverage simpler and more on segmenting the customer. Standardized plans made comparison shopping easier because benefits lined up more cleanly across carriers. A looser menu lets insurers differentiate through network design, cost-sharing quirks, and plan architecture. For carriers, that can be a feature, not a bug, in a market where the winning product may be the one that screens best on monthly premium even if it becomes expensive to use.

The result is a subtle but important shift in who wins. The old bullish ACA thesis was that scale and subsidy expansion would keep pulling more people into exchange coverage. The new version may be narrower: the winners are the carriers, brokers, and pricing teams that know how to operate in a more brittle, price-sensitive market where bronze migration and enrollment churn matter more than broad coverage growth. This starts to look less like a pure health-policy story and more like consumer finance, where the sale depends on the payment shoppers notice first.

There are offsets. Tighter verification could reduce improper enrollments. Lower user fees should put at least some downward pressure on premiums. And more plan flexibility can help some insurers tailor products to local needs. But that does not change the bigger direction of travel.

The ACA exchange business is increasingly being asked to solve an affordability problem without actually lowering the cost of care. When that happens, the market tends to route the pressure into product design. If premiums are the number that gets advertised and deductibles are the number that gets delayed, insurers have every incentive to optimize the first one harder than the second.

That is the real takeaway from the latest CMS rule and the latest enrollment data. The marketplace is not just shrinking at the margin. It is being remade into a place where complexity does more of the commercial work.