Central Garden & Pet's Phillips Deal Moves the Pet Aisle to the Distribution Desk

TL;DR: Central Garden & Pet's pet distribution joint venture with Phillips Pet Food & Supplies matters because it turns a boring warehouse function into a capital-allocation choice. Central keeps a 20% stake in the new platform, gets cash proceeds, and can make the higher-value part of the story about branded pet and garden products instead of owning every truck, pallet, and route sheet.

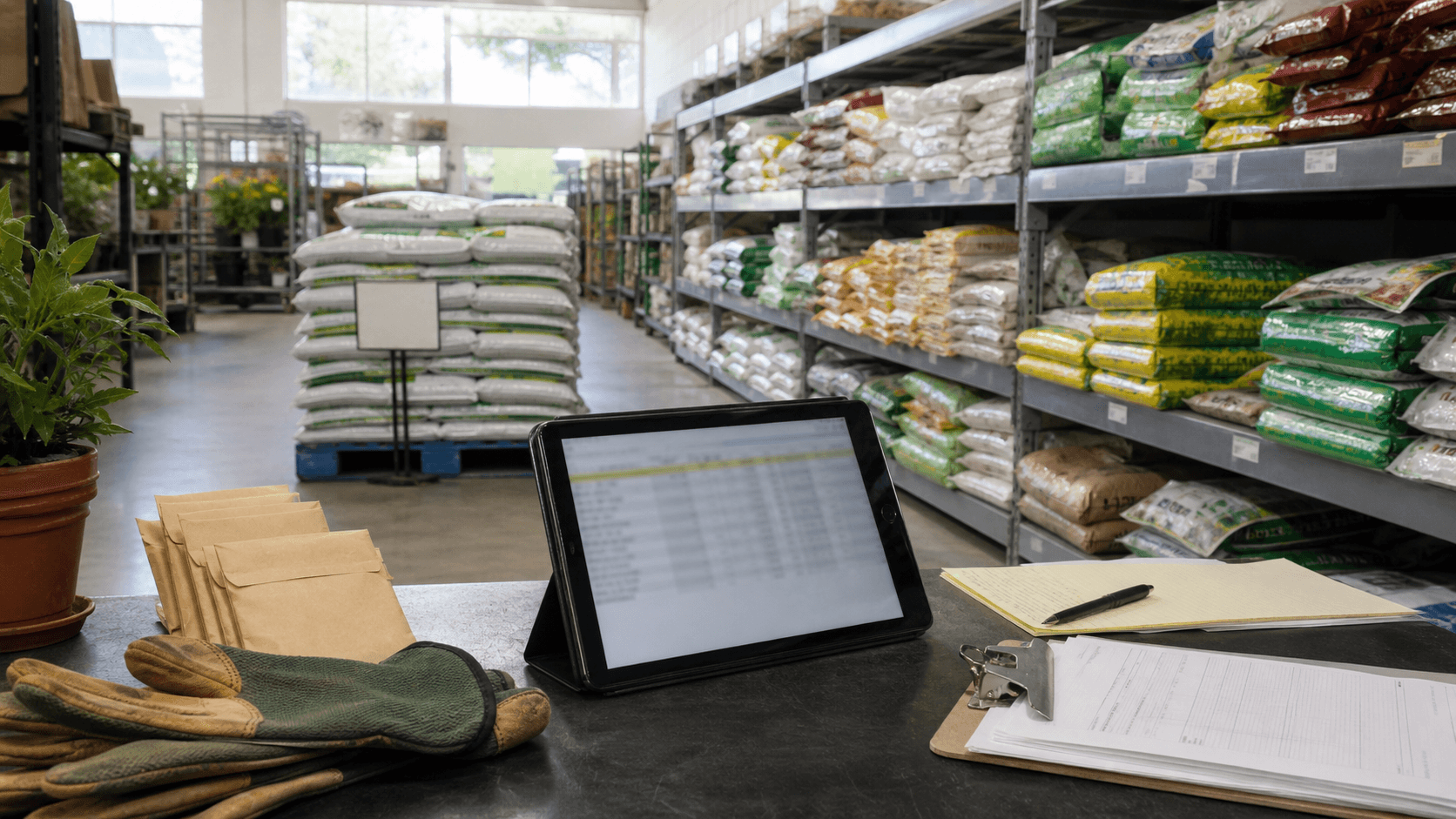

##What Central Garden & Pet Is Really Moving

Central Garden & Pet and Phillips announced an April 2026 pet distribution joint venture, with Central receiving cash proceeds and retaining 20% ownership in the new platform.

That is easy to read as a supply-chain housekeeping item. It is more interesting than that.

Central is separating the part of the pet business that looks like a national logistics network from the part investors usually want to pay for: brands, shelf placement, product mix, and seasonal execution.

The bet is not that distribution suddenly becomes unimportant. The bet is that distribution has become too important to keep treating it as background plumbing.

##Why Distribution Is Now a Margin Decision

In consumer products, the warehouse is where brand strategy meets ugly math.

A pet toy or bag of treats can have a nice gross-margin story on a slide. Then it has to move through a distributor, arrive at the right store, avoid out-of-stocks, avoid excess inventory, and support retailers that are increasingly allergic to working-capital surprises.

#The hidden cost is not just freight

The cost is coordination:

- which products get truck space

- which stores get priority when demand shifts

- how much inventory sits between the manufacturer and the shelf

- who pays when service levels disappoint

That is why the Phillips deal is not just a route map. It changes where Central wants to spend managerial attention.

If the joint venture works, Central can still influence pet-channel reach without carrying the full operational weight of every distribution decision inside the core company.

##Where The Q2 Numbers Make The Deal More Telling

Central's latest quarter gives the move more context. The company reported record Q2 fiscal 2026 net sales of $906.2 million, up from $833.5 million a year earlier, and operating income of $114 million.

The garden side was especially seasonal. In its quarterly filing, Central said garden net sales rose 13.0% to $429.3 million for the quarter ended March 28, 2026.

That kind of business is not managed only by brand slogans. It is managed by timing.

Garden demand shows up in a narrow window. Pet demand is steadier, but pet specialty shelves still punish bad execution. A bag that arrives two weeks late is not a revenue asset. It is a pallet with a carrying cost.

#The operating scene is ordinary, but the stakes are not

Picture the receiving table behind a pet store: a scanner, a cart, a stack of food bags, a clipboard no customer ever sees.

That table is where the business model either becomes real or leaks margin. The retailer wants fewer mistakes. The manufacturer wants the right assortment. The distributor wants density and route efficiency. The customer just wants the product in stock.

Central's move recognizes that all four incentives are now too connected to leave distribution as a generic back-office cost.

##Who Should Care Besides Central Shareholders

This is not only a Central Garden & Pet story. It is a useful tell for branded consumer companies with mixed portfolios.

The old investor shortcut was simple: own brands, outsource complexity, and let distributors fight for scale. The newer version is messier. Brands still matter, but the ability to place them reliably across fragmented channels is becoming part of the margin moat.

Retailers should care because fewer distribution handoffs can improve service levels. Competitors should care because national reach can make it harder for smaller suppliers to win attention. Investors should care because cash proceeds and a retained stake can look tidy, but the real test is whether service improves without dulling Central's channel control.

##What The Market May Be Missing

The market often treats distribution as a lower-quality business than branded products. That is usually fair.

But in pet and garden, distribution is also the control surface. It decides how fast a product gets from a supplier promise to a shelf result.

Central's Phillips joint venture is a reminder that the next margin improvement in consumer products may not come from a louder brand campaign. It may come from deciding which operational burden belongs inside the company, which one belongs in a scaled platform, and which one should be shared with a partner that lives closer to the route.

That is a less glamorous story than a new product launch. It is also the sort of story that can quietly decide whether the new product ever gets a fair shot on the shelf.

#FAQ

What did Central Garden & Pet announce with Phillips?

Central Garden & Pet announced a strategic pet distribution joint venture with Phillips Pet Food & Supplies. Central said it would receive cash proceeds and retain a 20% ownership stake in the new platform.

Why is this financially important?

The deal can shift capital and management attention away from owning every distribution function while preserving access to national pet-channel reach. The financial question is whether that improves operating efficiency without weakening Central's control over customer service and shelf execution.

Is this mainly a pet story or a broader consumer-products story?

It starts in pet distribution, but the broader lesson applies to branded consumer companies with complex channels. When retailers demand better service and lower inventory risk, distribution becomes part of the margin strategy, not just a cost line.