The Market Is Pricing a Consumer Who Has Learned to Say No

The American consumer is not disappearing. That is the easy, wrong read. The more useful read is that the consumer is becoming a substitution machine.

That matters more for investors than another debate about whether people are "resilient." A household can keep showing up in the spending data while quietly changing the whole profit map underneath retailers, banks, card networks, restaurants, and consumer brands.

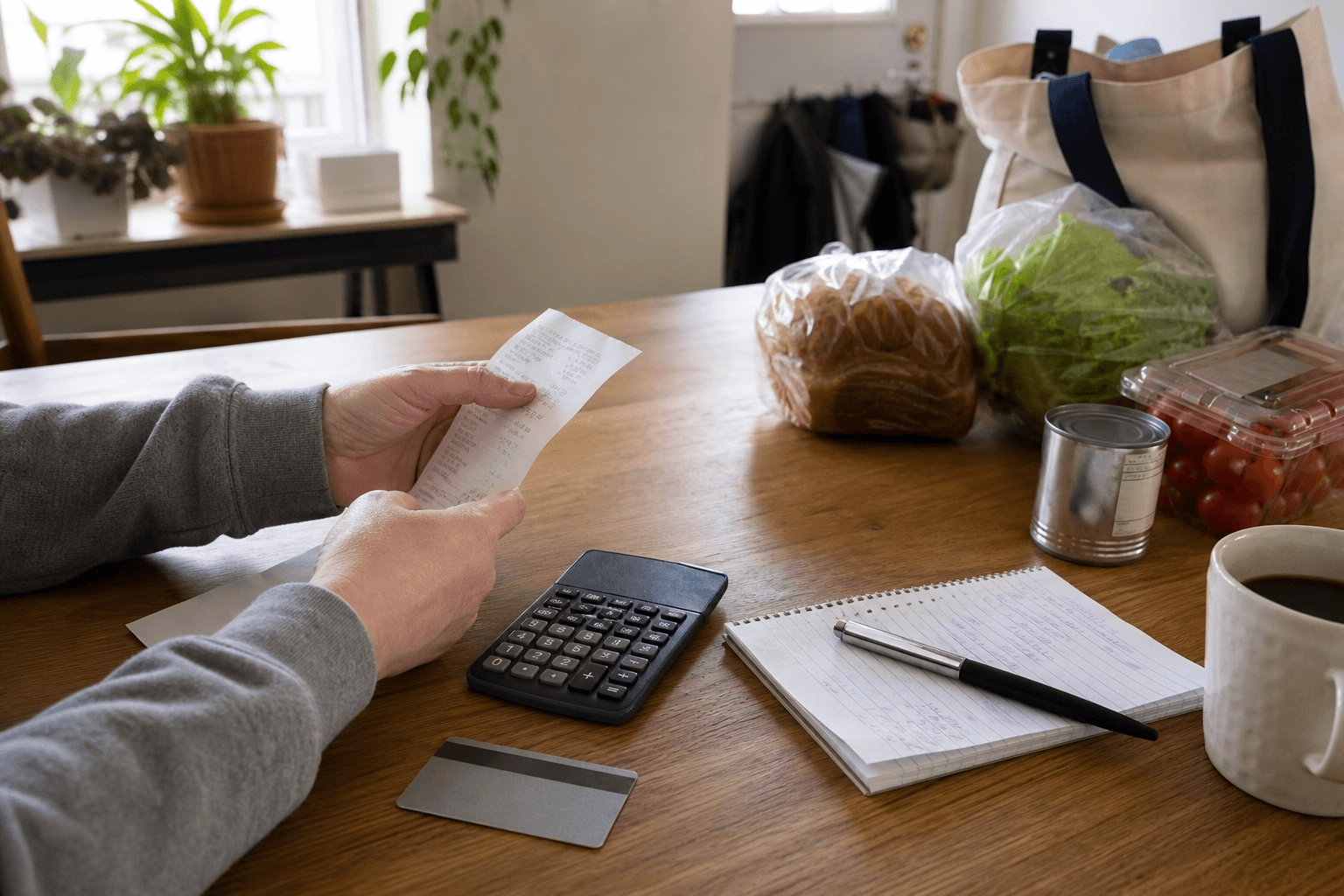

The scene is ordinary. Someone gets home from the store, puts the receipt beside a calculator, and realizes the bill did not explode because they got rich. It stayed manageable because the cart changed.

The brand cereal became store brand. The impulse item disappeared. The larger purchase moved to next month. The family did not stop consuming; it edited the basket.

That is the blind spot in the current market story.

Consumer confidence slipped in May, according to the Conference Board, even as stocks hovered near highs. Its index fell to 93.1 from 93.8. More important than the headline number was the special survey question: roughly two-thirds of consumers said rising prices had caused them to cut back on spending overall.

At the same time, private card data still shows the spending economy has not simply fallen over. Bank of America Institute's latest consumer work points to lower- and middle-income households easing back on discretionary purchases, while higher-income households continue to carry more momentum.

Put those together and the picture is not "strong consumer" or "weak consumer." It is more specific:

- Affluent households are still buying convenience, travel, services, and premium goods.

- Middle-income households are still spending, but with more edits.

- Lower-income households are protecting necessities and stripping out optionality.

That creates a different kind of consumer trade.

The winners are not just the companies with the cheapest price. They are the companies that make substitution feel painless.

A grocery chain with credible private labels is not merely selling cheaper cereal. It is selling permission to downgrade without feeling like a downgrade. A discount retailer with tight inventory is not just moving low-price goods. It is acting like a household budget tool. A payments company is not just processing volume. It is watching the consumer split one life into three ledgers: essentials, delays, and little rewards that keep morale alive.

This is why headline retail sales can mislead. Nominal spending can rise because gasoline, food, insurance, and rent absorb more dollars. That does not mean households are buying more life. It can mean they are paying more tolls before they get to choose.

The market often loves the first part of that sentence. Higher dollars mean revenue. Pricing power keeps margins alive. The consumer has not broken.

But the second part is where the business-model story sits. When consumers start editing baskets, they do not edit evenly.

They cut the product with the weakest habit. They delay the purchase with the least urgency. They switch away from the brand that taught them it was replaceable. They keep paying for the merchant or platform that saves them time, stress, or embarrassment.

This is a quiet test of brand equity. A company does not find out whether it has a real brand when wages are rising and credit is easy. It finds out when the customer is standing at checkout, holding the payment card, deciding which item can go back.

That checkout moment is more useful than a sentiment chart.

For banks, the same shift shows up differently. A consumer who is cutting back may still be leaning on credit for timing. That can support card balances and fee income for a while, but it also makes credit quality more sensitive to gasoline, food, insurance premiums, and rent. The bank is not only underwriting a borrower. It is underwriting the household's room to edit.

For retailers, the game becomes inventory humility. Too much discretionary stock becomes a margin problem. Too little value stock becomes a traffic problem. The operator who guesses the old basket gets punished twice: first by markdowns, then by lost trust.

For consumer brands, the danger is more permanent. Once a household discovers that the cheaper substitute is good enough, the old price ladder does not automatically rebuild itself when confidence improves.

That is the part investors tend to miss. Cutting back is not always a temporary pause. Sometimes it is customer education.

A year from now, if inflation cools and confidence recovers, some spending will come back. Vacations get rebooked. Restaurant visits return. Deferred purchases move forward.

But a portion of the substitution habit will stay. The consumer will remember which premium was worth paying and which one was just inertia with better packaging.

So the sharper question is not whether the consumer is still spending.

The sharper question is: who is teaching the consumer how to spend less and still feel in control?