Ingredion's Tate & Lyle Bid Prices The Reformulation Desk

TL;DR: Ingredion is reportedly in advanced talks to buy Tate & Lyle in a deal valued around $3.6 billion, and the interesting part is not just another cross-border food deal. It is a wager that the most valuable real estate in packaged food now sits at the reformulation desk, where brands try to cut sugar, add fiber, replace cocoa, manage tariffs, and protect margins without changing what shoppers taste.

##What Ingredion Is Really Buying

Reuters, citing Bloomberg, reported Sunday that Ingredion is in advanced talks to acquire Britain's Tate & Lyle in a deal valued at about 2.7 billion pounds, or $3.6 billion. The reported terms point to 615 pence per Tate & Lyle share, including cash and permitted dividends.

Ingredion is not buying a consumer brand that can raise shelf prices with a bigger ad budget. It is trying to buy more of the invisible layer inside consumer staples: starches, sweeteners, fibers, texturants, stabilizers, and formulation advice.

This is a business where the invoice is boring and the leverage is real.

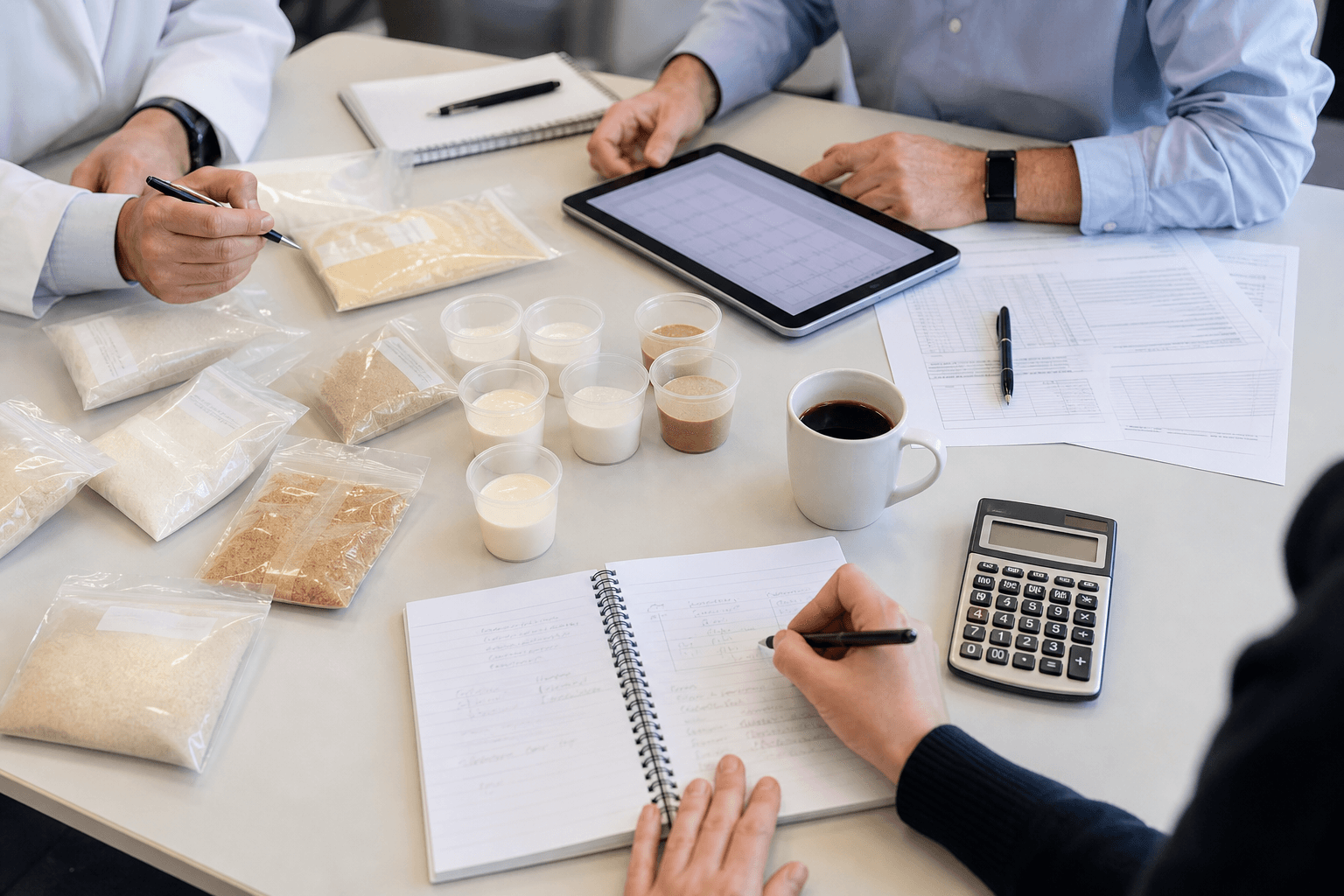

#The deal is about product math, not shelf space

Picture a food-company R&D room with a half-empty tray of snack samples, a spreadsheet of ingredient costs, and a product manager who has been told three things at once:

- reduce sugar,

- avoid a price increase,

- keep the texture exactly the same.

That is where a specialty ingredient supplier earns its margin. The brand owns the shopper relationship, but the ingredient partner can own the workaround.

If cocoa gets expensive, a cookie recipe needs help. If consumers want more protein or fiber, a drink needs help. If a tariff or crop shock moves an input cost, a plant manager needs a substitute that will not break production.

Ingredion wants more seats at that table.

##Why It Matters For Consumer-Staples Margins

The old packaged-food margin story was mostly about procurement scale. Buy corn, sugar, cocoa, dairy, packaging, and freight more efficiently than the next company. Then pass through what you can.

That still matters. But it is less complete now.

Consumers have been trained to notice price increases. Retailers push back on supplier pricing. Regulators and health-focused shoppers keep raising the bar on labels. The result is a quieter margin fight: companies need to change the recipe without making the customer feel the change.

Ingredion's own numbers show why the target matters. In the first quarter of 2026, Ingredion reported net sales of $1.792 billion, down 1%, and adjusted operating income down 22%. Its U.S./Canada Food & Industrial Ingredients segment was hit hard by operational challenges at the Argo facility.

But its Texture & Healthful Solutions segment was steadier: $617 million of first-quarter net sales, up 2%, and $100 million of operating income.

That contrast is the whole point. Commodity-like ingredients can get dragged around by plant reliability, price mix, and input cycles. Specialty formulation work has a better shot at becoming embedded in the customer's product roadmap.

##Where Tate & Lyle Fits

Tate & Lyle has already been repositioning itself around specialty food and beverage solutions. Its fiscal 2026 presentation showed pro forma revenue of 2.006 billion pounds, pro forma adjusted EBITDA of 415 million pounds, free cash flow of 164 million pounds, and net debt of 939 million pounds at March 31, 2026.

Those are not hypergrowth software numbers. They are the numbers of a company trying to make an old industrial ingredients platform more specialized.

The useful clue is in Tate & Lyle's own priorities: deliver the benefits of CP Kelco, target higher-growth subcategories, and focus customer-facing teams on buyers with greater growth potential.

In plain English: stop being just a supplier of stuff and become harder to remove from the customer's product-development process.

#CP Kelco makes the bid more operational than romantic

Tate & Lyle completed the CP Kelco acquisition before this approach, so any buyer is not just buying a clean, finished story. It is buying integration work, debt, plant complexity, and customer overlap.

That is why the deal should not be read as a simple confidence vote in food demand. It is also a bet that Ingredion can run the combined portfolio better than Tate & Lyle can on its own.

If Ingredion is wrong, it buys complexity while customers are already cautious. If Ingredion is right, it gets a deeper toolkit for the exact problem food companies are paying to solve: protecting margin without making products feel cheaper.

##Who Pays And Who Benefits

The affected parties are not just Ingredion and Tate & Lyle shareholders.

Large packaged-food companies may benefit if a combined supplier can solve formulation problems faster. Retailers benefit if brands can hold prices or improve private-label products without sacrificing quality. Consumers may never know the supplier's name, but they will feel the outcome in texture, sweetness, shelf life, and package size.

The risk sits with Ingredion investors.

The company is already managing a weaker U.S./Canada operating segment and expects capital expenditures of about $400 million to $440 million for 2026. Adding a 2.7 billion-pound acquisition would make execution the story, not just strategy.

There is also a customer-concentration logic to watch. If global food companies want fewer suppliers with broader technical capabilities, scale helps. If those same customers use that scale to squeeze suppliers harder, the margin uplift gets shared away.

##What Investors Should Watch Next

Ingredion has until 5:00 p.m. London time on June 11, 2026 under the UK Takeover Code to announce a firm intention to bid or walk away, unless the deadline is extended.

The next question is not whether food ingredients are important. They are.

The sharper question is whether specialty ingredients are important enough to offset deal debt, integration costs, and a tougher selling environment.

Watch three things:

- whether a firm offer keeps the 615 pence headline intact or adjusts for risk,

- whether Ingredion explains cost synergies or customer synergies with real operating detail,

- whether investors treat Tate & Lyle as a specialty upgrade or as another integration burden.

The deal makes sense only if the hidden formulation desk is becoming more valuable than the commodity plant behind it.

That is the bet. The shopper may never see it, but the gross margin line will.

#FAQ

Why would Ingredion want Tate & Lyle?

Ingredion would gain specialty ingredients, formulation capability, and customer relationships in food and beverage categories where brands need help with texture, sugar reduction, fiber, stabilizers, and cost substitution.

Is this mainly a consumer-staples story or a merger-arbitrage story?

For Gainbrief, it is mainly a consumer-staples margin story. The deal mechanics matter, but the larger issue is how food companies protect margins when shoppers resist higher prices and ingredient costs keep moving.

What is the biggest risk for Ingredion?

The biggest risk is paying for specialty scale while inheriting integration work, debt, and operational complexity. If customers capture most of the savings or growth through tougher purchasing terms, the strategic logic could look better than the financial result.