Healthcare Affordability Is Becoming a Membership Business

The interesting part of GoodRx's new $14.99-a-month Companion plan is not the price. It is the admission hiding inside the product. A large and growing slice of American healthcare is no longer being sold as insurance. It is being sold as a membership.

That is the business story investors should watch. When a company built on coupons, cash-pay prescriptions, and price transparency starts bundling cheap generics, telehealth visits, and dental and vision savings into one monthly plan, it is not just launching another subscription. It is telling you where the real demand is sitting: in the gap between having coverage and being able to use the system comfortably.

The usual healthcare debate is about who will pay. The newer commercial question is who can organize the out-of-pocket mess.

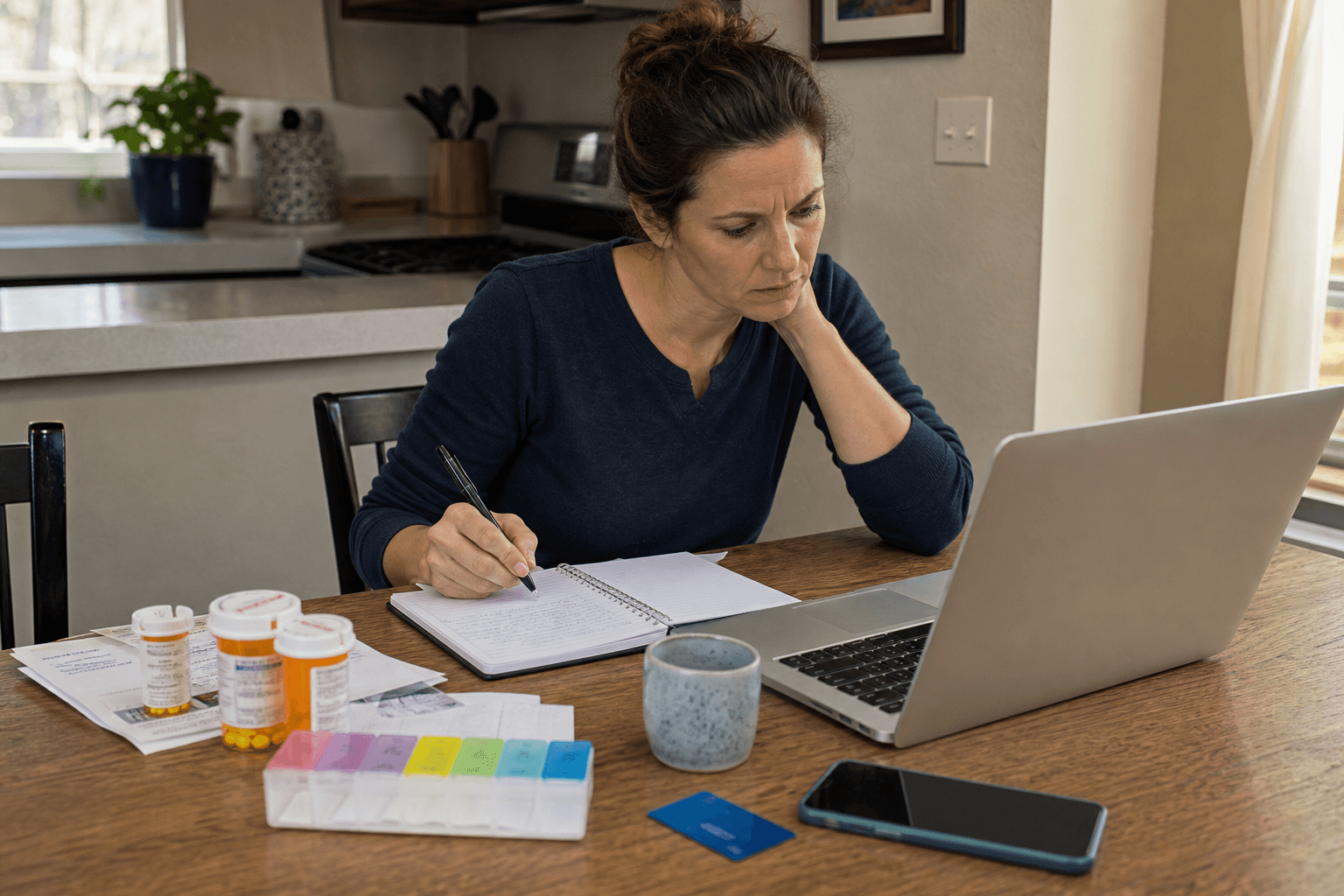

Picture the pharmacy counter. A customer has an insurance card in one hand and a phone in the other. The pharmacist is not explaining a breakthrough drug. They are explaining why one path runs through the deductible, another runs through a coupon, and a third might simply be cheaper in cash.

That scene used to feel like friction around the real product. It is starting to look like the product itself.

GoodRx's own numbers point in that direction. In first-quarter 2026 results released on May 6, the company said total revenue fell 4% to $194 million and prescription-transactions revenue dropped 24% to $113.7 million as parts of the retail-pharmacy landscape weakened. But subscription revenue rose 16% to $24.4 million, and Pharma Direct revenue jumped 82% to $52.2 million. On May 27, GoodRx followed that with Companion, a new membership built around low-cost generics, online visits, and everyday-care discounts.

The easy read is that GoodRx is trying more products because the old coupon business is maturing. True enough.

The more important read is that healthcare affordability is being unbundled into retail components. Consumers are being asked to navigate drugs, primary care, specialty access, vision, labs, and routine treatment like a stack of separate purchase decisions. Once that happens, the company that bundles savings, navigation, and convenience starts looking less like a marketing layer and more like a benefits manager for the underinsured middle.

That shift matters beyond GoodRx.

- It creates room for healthcare companies to monetize navigation, not just treatment.

- It turns price transparency into a recurring service, not a one-time search tool.

- It rewards businesses that can package fragmented care into something that feels predictable enough to budget.

Investors often describe American healthcare as a payer system. For millions of households, it functions more like a checkout system. The insurance card is still present, but it does not settle the question that matters most in the moment: what will this actually cost me this week?

That is why the membership framing is so revealing. It takes a category that was supposed to be protected by insurance and recasts it as a consumer-finance workflow.

The customer is not buying prestige. They are buying fewer surprises.

This is also why I do not think the best comparison is Amazon Prime or Costco. Those are convenience memberships built on abundance. What GoodRx and similar models are building is closer to a defensive household operating system. The value is not that you get more. The value is that you can keep the routine parts of healthcare from blowing up the monthly budget.

There is a deeper market implication here. If routine affordability keeps moving into subscription bundles, then parts of healthcare that used to rely on opaque reimbursement may be forced to become more legible consumer products. Drug makers will try direct pricing. Telehealth will keep collapsing simple visits into fixed-price packages. Pharmacies and intermediaries will fight for the right to own the search, payment, and refill relationship.

In other words, the industry's margin pool may keep drifting toward whoever controls the decision moment before care is purchased.

That is a very different business from traditional insurance. Insurance wins by pooling risk and negotiating networks. A membership business wins by reducing cognitive load and making scattered prices feel manageable. One is built around catastrophe. The other is built around repetition.

And repetition is where loyalty lives.

GoodRx says nearly 25 million unique consumers used its platform in 2025 and that it helped drive about $17 billion in consumer savings. If even a modest share of those users can be moved from occasional bargain-hunting into recurring membership behavior, the company gets something much more valuable than traffic. It gets a steadier claim on the household budget.

That is the twist in this story. American healthcare has spent years training consumers to shop around because the system is too fragmented and too expensive to trust blindly. Now the next generation of healthcare businesses may get paid for cleaning up the behavior that fragmentation created.

The insurance card is still in the wallet.

But the real battleground may be the membership fee that sits on top of it.