CordenPharma-AmbioPharm Puts Peptide Capacity Inside The GLP-1 Trade

TL;DR: CordenPharma's agreement to acquire AmbioPharm is a small M&A headline with a large GLP-1 lesson: the obesity-drug boom is not only a brand, patent, or pharmacy-access story. It is also a validated peptide manufacturing story. As Lilly and Novo push more demand into the system, pricing power can move toward the companies that can make complex peptide APIs reliably, document the batch, and release supply without turning quality into the bottleneck.

##What CordenPharma Is Really Buying

CordenPharma said on May 27, 2026 that it had agreed to acquire AmbioPharm, a U.S.-headquartered peptide API contract development and manufacturing organization with sites in North Augusta, South Carolina, and Shanghai.

That sounds like a niche pharmaceutical supply-chain deal. It is not.

AmbioPharm adds peptide API development and manufacturing capacity, including upstream and downstream work, to CordenPharma's existing peptide platform. For drug developers, the attractive part is not a prettier lab brochure. It is more optionality around scale-up, regional supply, synthesis methods, and validated release.

#Why peptide API capacity is different from ordinary capacity

Peptides are not simple commodity inputs. A drug sponsor does not just order more material the way a retailer orders more boxes.

The work has chemistry constraints, purity requirements, documentation requirements, and customer-specific process history. When the product is tied to chronic metabolic demand, a weak manufacturing handoff does not merely delay revenue. It can interrupt prescriptions, payer coverage, and patient continuity.

That is why this deal belongs on a business page, not only a pharma trade page.

##Why GLP-1 Demand Changes The Value Of The Middle

The market has been trained to watch the front door: Lilly, Novo Nordisk, list prices, telehealth channels, compounding fights, and insurance coverage.

The quieter money question sits behind the door. Who can actually make enough compliant peptide material when demand keeps moving?

Lilly reported Q1 2026 revenue of $19.8 billion, up 56%, with growth led by Mounjaro and Zepbound. That kind of number turns manufacturing capacity into strategy. The revenue line may show up in Indianapolis, but the operating pressure travels through procurement teams, quality units, fill-finish schedules, API suppliers, and backup manufacturing networks.

This is the part casual investors often miss: the GLP-1 trade is not just "more patients equals more drug sales." It is also "more patients equals less tolerance for fragile supply."

##Where The Bottleneck Shows Up

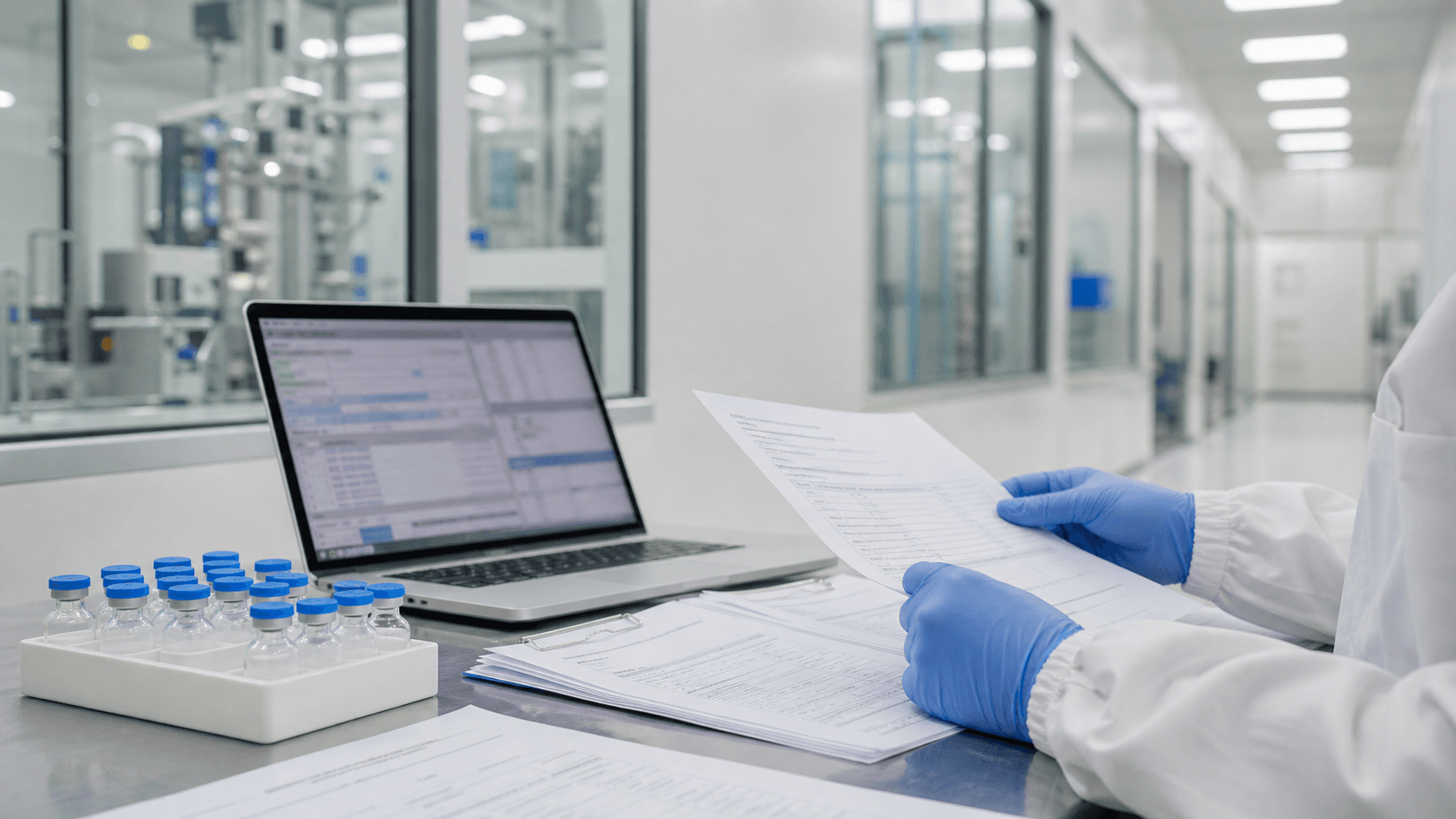

Picture a quality-release desk, not a trading screen.

A batch record lands on a desk beside sample vials and a laptop. Someone has to confirm what was made, where it was made, whether the specs held, whether deviations were handled, and whether the material can move into the next step. If that process is slow, the bottleneck is no longer a reactor. It is trust.

#The operating mechanism investors should watch

The useful question is not whether peptide demand is large. It plainly is.

The sharper question is which firms can convert demand into dependable throughput. In this market, the margin line can be influenced by boring things:

- qualified manufacturing slots

- regional redundancy between the U.S., Europe, and Asia

- process transfer speed from clinical to commercial scale

- batch-release discipline and quality documentation

- customer confidence that a second supplier will not create a regulatory mess

Those are not glamorous. They are exactly the places where pricing power hides.

##Who Benefits If Capacity Becomes Scarce Again

CordenPharma is privately held and backed by Astorg, while AmbioPharm has been Carlyle-sponsored. The public-market read-through is therefore indirect.

But the mechanism matters for public investors anyway.

If GLP-1 brands keep growing, drugmakers with secure peptide supply chains protect revenue better than drugmakers that discover their commercial plan depends on a single fragile handoff. CDMOs with scarce peptide expertise can become more important counterparties. Smaller biotech companies developing peptide drugs may face harder choices about whether to reserve manufacturing capacity early, pay up, or partner before they would like to.

The buyer in this story is not just buying plants. It is buying a place in customers' contingency plans.

##Why The FDA Angle Raises The Stakes

The FDA has been tightening the GLP-1 gray zone. In April, the agency clarified policies for compounders as national GLP-1 supply stabilized and reminded compounders about restrictions on making copies of FDA-approved drugs.

That matters because it pushes the market back toward approved products and regulated supply chains.

When shortage-era flexibility fades, the official manufacturing system has to carry more of the load. That is good for branded drugmakers if they can meet demand. It is also good for specialized suppliers whose main product is not a vial, but confidence that the vial can be made, documented, and released.

This is the twist: GLP-1 supply stabilization does not make manufacturing less important. It makes the approved manufacturing chain more important.

##What The Market Should Take Away

The easy GLP-1 story is about winners at the brand layer. Lilly sells more. Novo fights harder. Telehealth players adjust. Insurers complain.

The better business story is that the boom is pulling value into the industrial layer beneath the prescription.

CordenPharma's AmbioPharm deal is one more sign that peptide capacity is becoming a strategic asset class inside healthcare. Not because every CDMO becomes a miracle compounder, and not because every capacity announcement deserves a valuation premium. Most do not.

But when a market grows fast enough, the unglamorous supplier with the validated process can become the party everyone has to call before the revenue forecast becomes real.

#FAQ

Why does the CordenPharma-AmbioPharm deal matter for U.S. investors?

It shows that GLP-1 economics extend beyond Lilly and Novo Nordisk. U.S. investors should watch peptide API capacity, CDMO pricing power, and supply-chain redundancy because those factors can affect drug availability, launch speed, and gross-margin protection.

Is this mainly a GLP-1 drug story?

No. GLP-1 demand is the clearest commercial pressure point, but peptide API capacity also matters for broader metabolic, oncology, rare-disease, and specialty-drug pipelines that need complex manufacturing.

What is the biggest risk in reading too much into this deal?

The risk is treating every peptide capacity move as automatically bullish. Capacity only has financial value if customers trust the process, regulators accept the documentation, and demand remains strong enough to keep specialized assets utilized.