The Consumer Economy Has Split Into a Portfolio and a Fuel Bill

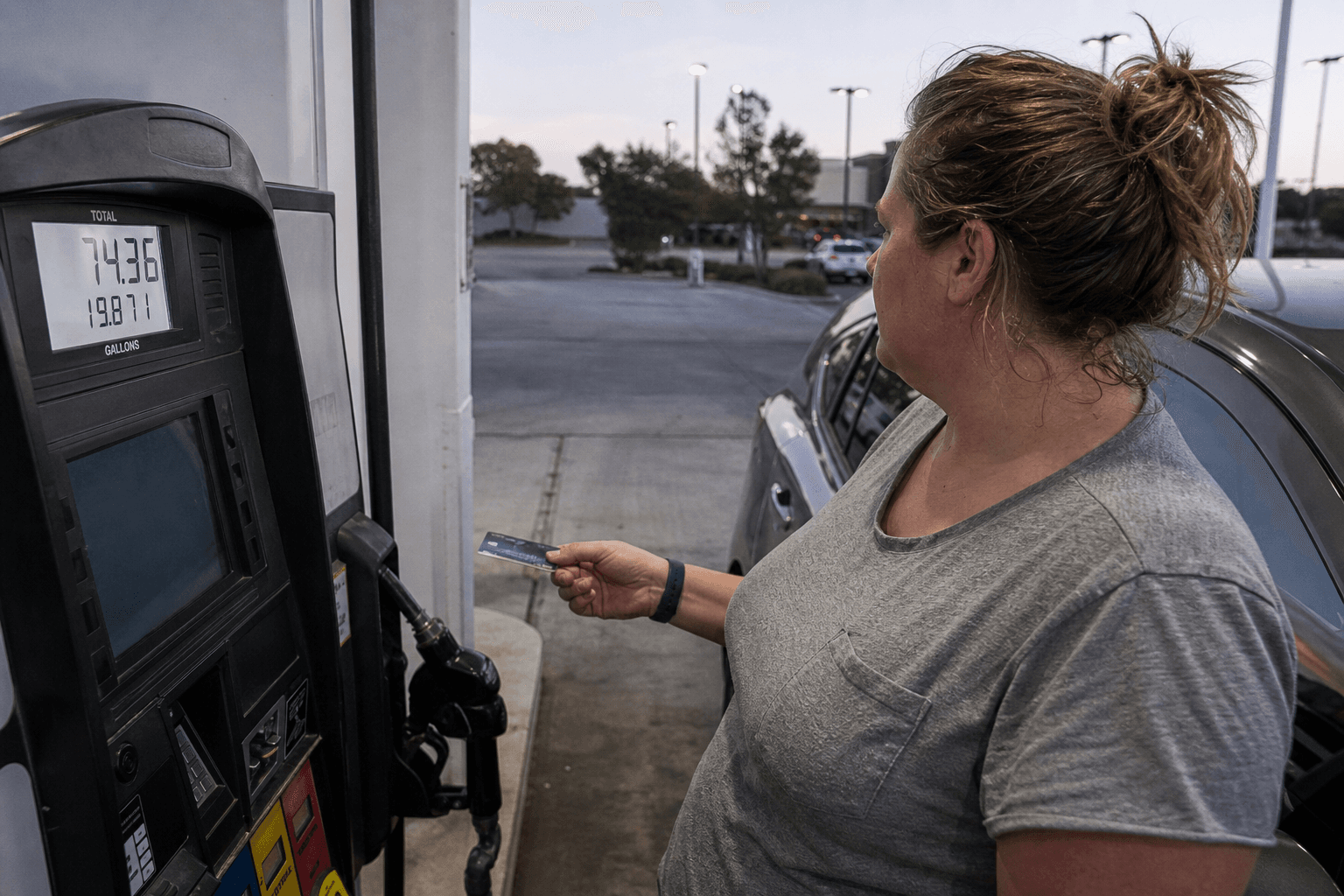

At a gas station, the total flips past $70 before the nozzle clicks off. Ten minutes later, the same driver is in a big-box parking lot deciding which items still make the cart and which ones wait another week.

That is the consumer story right now. Not “resilient.” Not “cracking.” Split.

The market keeps talking about the American consumer as if it is one balance sheet. It is not. It is two very different cash-flow systems living in the same retail data. One household can absorb higher fuel and food bills because its 401(k), brokerage account, or home equity still creates psychological room to spend. The other household is using more of its paycheck just to stay mobile.

That is why the latest numbers look sturdier than they feel.

April retail sales rose 0.5%, according to Commerce Department data reported by Reuters. Gas-station receipts were up 2.8% in the month after a huge jump in March, while online sales and electronics also moved higher. On paper, that looks like a consumer who is still alive and kicking.

But sales are nominal. They count dollars, not relief.

Reuters also noted that some economists think sales adjusted for inflation dipped in April, and that the saving rate had already fallen to 3.6% in March, the lowest since October 2022. Larger tax refunds and strong stock gains helped keep spending moving. That is not the same thing as broad comfort. It is a temporary brace.

Today’s confidence data makes the split harder to ignore. The Conference Board’s consumer confidence index slipped to 93.1 in May, according to AP, while Reuters separately reported that worries about inflation tied to higher energy costs weighed on households. Last week, the University of Michigan’s sentiment gauge hit a record low for May. People are still transacting. They just do not feel richer while doing it.

This is why I think investors are still using the wrong retail lens.

The common question is whether higher gas prices will finally “break” the consumer. That framing misses what is already happening. The break is not a cliff event. It is an allocation event.

Money is being pushed away from optional purchases and toward mobility, staples, and merchants that help households compress decision-making. A warehouse club, a value grocer, a refill-heavy beauty basket, a delayed apparel purchase, a smaller restaurant check, a buy-now household repair instead of a weekend trip. That is how pressure shows up before it becomes a recession statistic.

Walmart’s latest quarter fit that logic better than the bullish headlines did. AP reported that the company kept drawing a broader mix of shoppers with low prices and faster delivery even as spending on essentials, especially gasoline, stayed heavy. Reuters, looking ahead to the next batch of retailer earnings, flagged elevated gas prices as the thing investors are watching to see whether they are eating into other categories.

That is the key point: the winners here are not simply “discount retailers.” They are toll-road operators inside household budgeting.

If a chain can help a customer solve three problems at once, cheap basket, fewer trips, faster fulfillment, it is not merely taking market share. It is selling cash-flow efficiency. In an inflationary stretch, that is a more durable moat than brand heat.

The losers are not just luxury names or weak merchants. They are businesses that rely on wandering, incremental spending from customers who now arrive with a tighter mission. When the gas bill gets louder, browsing gets quieter.

There is a market implication here, too. Wall Street keeps celebrating strong equity prices and decent top-line retail data as proof that the consumer is in good shape. But part of that strength is a wealth-effect subsidy flowing to the upper leg of the economy, exactly the “K-shaped” pattern Reuters highlighted. That support is real, but it is narrow. It can keep aggregate spending up while making the underlying retail mix much more defensive.

So the consumer economy is not sending one message.

It is sending three at once:

- Aggregate spending can still look healthy even when lower-income households are losing room.

- Retail share will keep moving toward businesses that save time, trips, and mental bandwidth, not just dollars.

- The next real margin fight is not about demand destruction alone. It is about whether merchants are positioned on the “portfolio” side of the consumer or the “fuel bill” side.

That is a much sharper distinction than bulls want to admit.

If gas stays high and wage growth keeps lagging prices, the question is not whether the consumer disappears. The question is which version of the consumer your business model was secretly built for.