ServiceTitan Puts $21.7 Billion Of Contractor Revenue On The Invoice Desk

TL;DR: ServiceTitan reported $268.8 million of fiscal first-quarter revenue and $21.7 billion of gross transaction volume through its trades platform, but the more important story is not another software growth print. It is that contractor software is moving closer to the invoice, payment, and job-costing handoff. That makes ServiceTitan less like a seat-count SaaS vendor and more like a financial workflow layer for HVAC, plumbing, electrical, and other field-service businesses.

##What ServiceTitan Reported

ServiceTitan's fiscal first-quarter 2027 results were clean enough to tempt the usual software recap.

Revenue rose 25% year over year to $268.8 million. Platform revenue rose 25% to $260.6 million. Non-GAAP income from operations improved to $40.8 million, or a 15.2% margin, while the GAAP operating loss narrowed to $25.8 million.

Those are useful numbers. They are not the main event.

The better number is $21.7 billion of gross transaction volume, up 23% from a year earlier. ServiceTitan defines that metric as the total dollars invoiced by customers through its platform, which means it is watching the money flow across thousands of contractor jobs, not merely counting logins.

That is the piece casual readers miss. In the trades, the invoice is where software stops being a dashboard and starts becoming economic infrastructure.

##Why The Invoice Matters More Than The Login

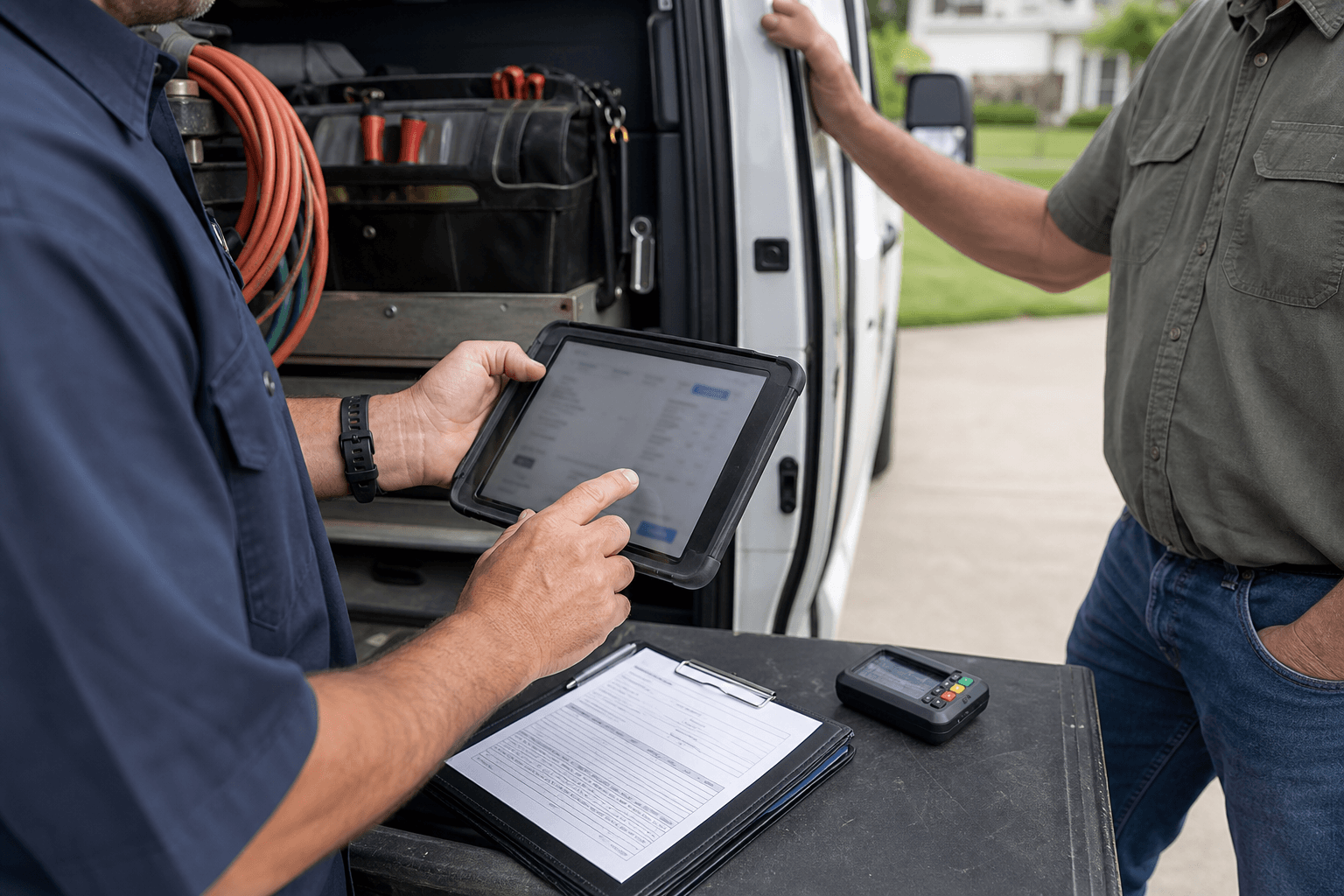

There is a boring desk inside almost every home-services business where the real operating leverage lives.

A technician finishes a water-heater job. The office has to confirm the parts, labor time, dispatch history, warranty status, tax, customer approval, financing option, and payment. If that step lives across paper, a spreadsheet, a phone call, and a separate card terminal, the owner does not have clean economics. The owner has a pile of jobs that may or may not become cash on time.

ServiceTitan's opportunity is to make that handoff harder to leave.

#How gross transaction volume changes the SaaS story

Seat-based software is easier to replace than payment-adjacent workflow.

If a vendor only manages schedules, a contractor can compare subscription costs. If the vendor also becomes the place where invoices are created, payments are captured, technicians are measured, and managers see which jobs made money, the switching cost moves from "train the staff again" to "rebuild the operating record."

That is a much stickier problem.

For investors, $21.7 billion of GTV says the platform is touching the customer's revenue engine. The company still has to prove durable free cash flow, but the quality of the attachment is different from a normal software tool that sits one layer away from money.

##Where The Margin Mechanism Shows Up

ServiceTitan also gave investors a margin story, though it should be read carefully.

The company's non-GAAP operating margin improved from 7.5% a year earlier to 15.2% in the April quarter. GAAP cash used in operating activities improved to $1.6 million from $14.6 million, while non-GAAP free cash flow was still negative $9.6 million.

That combination is not a victory lap. It is a test.

The business is telling the market that it can grow, absorb product investment, and move toward better operating economics at the same time. But the reason that argument is plausible is not just subscription scale. It is usage revenue tied to a contractor workflow that becomes more valuable as more work passes through it.

#The hidden customer math

A trades owner does not wake up excited to buy "agentic operating systems." That language is for investor decks.

The owner cares about simpler questions:

- Did the technician arrive on time?

- Did the invoice include all labor, materials, and warranty details?

- Did the customer pay before the truck left the driveway?

- Did the manager know which jobs were profitable before payroll was due?

Software that answers those questions has a better shot at budget survival than software that merely promises productivity.

##Who Pays And Who Gets Leverage

The immediate customer is the contractor. The economic pressure comes from several directions at once.

Homeowners are rate-sensitive. Labor is tight. Parts costs can move quickly. A small HVAC or plumbing company may have enough demand but still leak margin through callbacks, underpriced jobs, delayed invoices, or weak collection discipline.

That is why ServiceTitan belongs in a Gainbrief finance lane, not a pure tech lane. This is a small-business cash-conversion story.

The more jobs that flow through one system, the more the software vendor can sell adjacent pieces: payments, financing, analytics, marketing, call-center workflow, and AI-assisted office work. The contractor pays because fragmented administration is expensive. ServiceTitan gets leverage because the administrative mess sits next to revenue.

The risk is also clear. If usage revenue depends on transaction activity, then macro pressure on homeowners and commercial property maintenance can show up in the platform's growth rate. A software company attached to real-world invoices gets real-world cyclicality as part of the package.

##What Investors Should Watch Next

ServiceTitan's Form 8-K says the company expects fiscal 2027 revenue of $1.13 billion to $1.14 billion and non-GAAP income from operations of $142 million to $147 million.

That guide matters, but it is not the sharpest scoreboard.

The better watchlist is simpler:

- Whether gross transaction volume keeps growing faster than contractor headcount or software seats.

- Whether usage revenue expands without forcing contractors into products they do not trust.

- Whether free cash flow turns positive while ServiceTitan keeps investing in onboarding, AI, and vertical-specific workflows.

- Whether commercial and residential trades behave differently as rates, housing turnover, and maintenance budgets shift.

The stock market will probably argue about software multiples. The operating story is more physical. It is about whether a contractor's messy workday can be turned into a reliable financial record.

That is a harder thing to copy than a prettier dashboard.

#FAQ

Why does ServiceTitan's gross transaction volume matter?

Gross transaction volume shows how much customer revenue is invoiced through the platform. For ServiceTitan, $21.7 billion of GTV suggests the software is close to contractor cash flow, not just back-office recordkeeping.

Is this just another enterprise software earnings story?

No. The useful angle is that ServiceTitan is attached to field-service invoices, payments, and job economics. That makes the business more exposed to real contractor activity than a generic seat-based SaaS tool.

What is the main risk for investors?

The same workflow attachment that creates stickiness can also import cyclicality. If homeowners delay repairs, commercial maintenance budgets tighten, or contractors slow hiring, ServiceTitan's usage-linked economics can feel that pressure.