I write about markets, AI, the economy, online business, and the small signals most people miss.

The Most Interesting AI Startup This Week Isn't Trying to Replace You

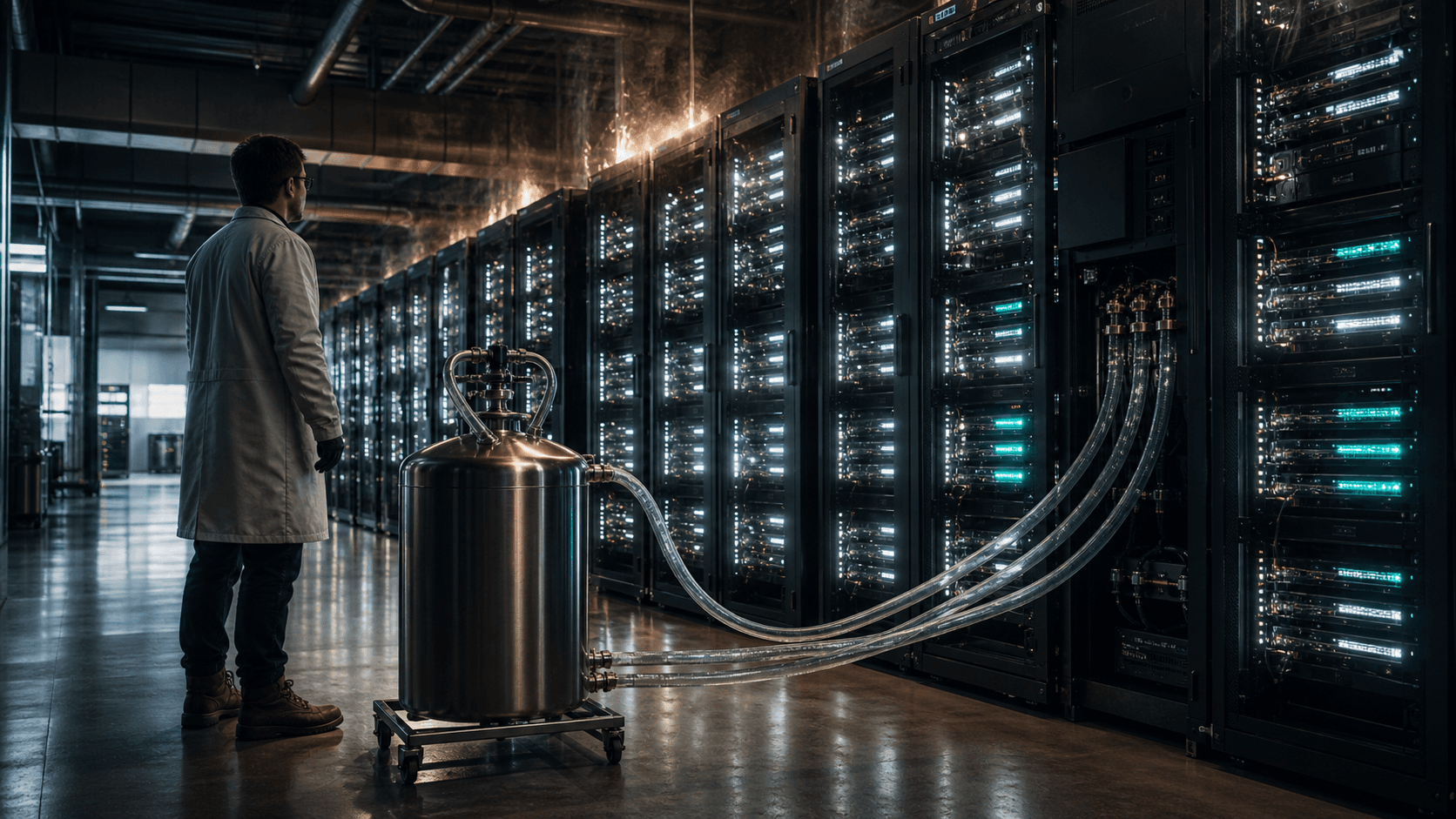

A British ex-DeepMind researcher just raised $50 million to do the least glamorous thing in AI right now: make a new liquid that keeps server racks from cooking themselves. No chatbot. No agent that books your flights. A coolant. And I think it's one of the more honest bets in the whole field. Here's the setup. The AI boom runs on GPUs, and GPUs run hot. Jonathan Godwin, Orbital's CEO, describes a modern GPU rack as packing "basically a supermarket's worth of energy into a filing cabinet." You have to pull that heat out somehow, and one of the best ways the industry found uses a class of chemicals called PFAS. You've heard the other name for them. Forever chemicals. That's the part of this story nobody puts in the funding headline. PFAS don't break down. They show up in roughly 45% of tap water samples tested across the US. They build up in your liver and kidneys over years, and they've been linked to liver damage, thyroid disease, and kidney and testicular cancer. The companies that made these chemicals profitable were rarely the ones drinking the runoff. nihThe Cooling Report So when Orbital says its AI screened hundreds of thousands of candidates to find a coolant that does the job without the forever chemicals, that's not a vanity product. That's pointed straight at a problem that's already in somebody's well water near a chemical plant in North Carolina. Fortune Now the skeptic in me has to speak up, because this field has a track record. Two years back, DeepMind announced its AI had found 2.2 million new crystals, 380,000 of them stable enough to maybe synthesize. Sounded like a new world. Then actual materials scientists opened the database and found over 18,000 of the "discoveries" contained radioactive elements so s

The SEC Wants More IPOs. Investors May Pay the Price

The SEC can make it cheaper for companies to go public without making the whole public market less transparent. Optional semiannual reporting might help some companies a little. But it also creates a real risk: information that used to appear in public filings may start moving into private conversations. The argument sounds simple. The number of public companies has fallen, so disclosure rules must be too heavy. That is why the SEC’s May 2026 proposals try to make life as a public company more flexible. One idea is to let companies replace quarterly 10-Q filings with one semiannual Form 10-S, plus the annual 10-K. For companies, that sounds like more choice. For investors, it changes how the market works. A voluntary earnings release is not the same as a required 10-Q. The 10-Q is not valuable only because it gives investors numbers. It matters because those numbers come in a standard format, under review discipline, with legal responsibility, comparability, and machine-readable structure. Take that away, and the information gap does not vanish. It just moves somewhere else. Big institutions can pay for alternative data, talk to management teams, and rebuild the missing picture. Retail investors usually do not have that luxury. They depend on public filings. When required disclosure gets weaker, the market becomes easier for insiders and more expensive for everyone else. The global evidence also does not prove that lighter rules magically bring IPOs back. The UK changed its listing rules in 2024, but IPO activity was still mostly flat from 2023 to 2025 before picking up late in 2025. Australia has also tried to make IPOs easier, but even there, the slowdown looks partly cyclical, not just regulatory. The U.S. already tried one version of the “more listings, lighter disclosure” idea. It was called SPACs. The result was not exactly beautiful. Renaissance Capital found that of 199 companies that went public through SPAC mergers in 2021, only 11% were trading above their offer price by April 2022. The

SoFi Looks Cheaper, But the Market Wants Bank-Level Proof

SoFi is not a “last chance to buy cheap” story. It is a cleaner but harder question: has the market started valuing SoFi as a real digital bank before it has fully stopped judging it like a volatile fintech story? At around $16, the stock is no longer priced like pure euphoria. But it is not an obvious bargain either. The company is growing fast, profitable, and increasingly funded by a large deposit base. That is the bullish case. The catch is that investors are now asking for bank-like proof: credit quality, durable margins, and fewer surprises in the parts of the business that used to carry the fintech premium. The first-quarter numbers were strong. SoFi reported about $1.1 billion in adjusted net revenue, up 41% year over year. Net income reached roughly $167 million. Members climbed to 14.7 million, products reached 22.2 million, and total loan originations hit $12.2 billion. That is not a weak company being rescued by a good headline. It is a business that has crossed into scale. The more important detail is funding. Deposits reached about $40.2 billion, and average deposits made up more than 90% of average liabilities. That matters because SoFi’s bank charter is no longer just a strategic talking point. It is lowering funding costs and giving the lending business more room to compound. This is where the bull case gets real. SoFi is not merely adding users. It is turning more users into multi-product customers, pushing financial services products higher, and using deposits to support a more profitable lending engine. If that loop keeps working, the business can grow into a valuation that still looks demanding on today’s earnings. But there is a reason the stock fell after good results. Management did not raise full-year guidance. For an ordinary company, reaffirming guidance after a strong quarter is fine. For a high-expectation stock, it can feel like a warning label. Investors heard: yes, the quarter was excellent, but not enough has changed for management to promise more. The second issue is th