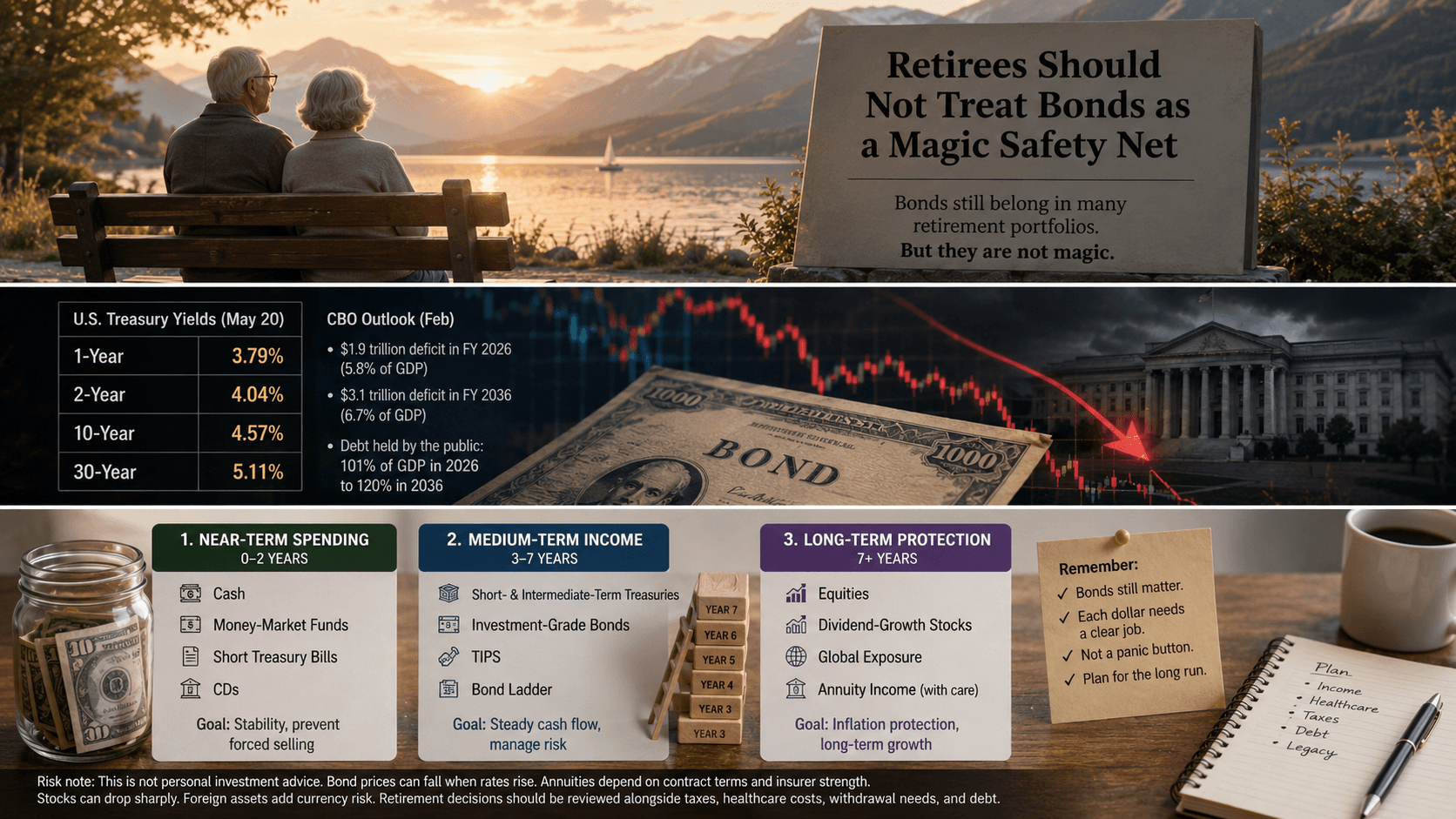

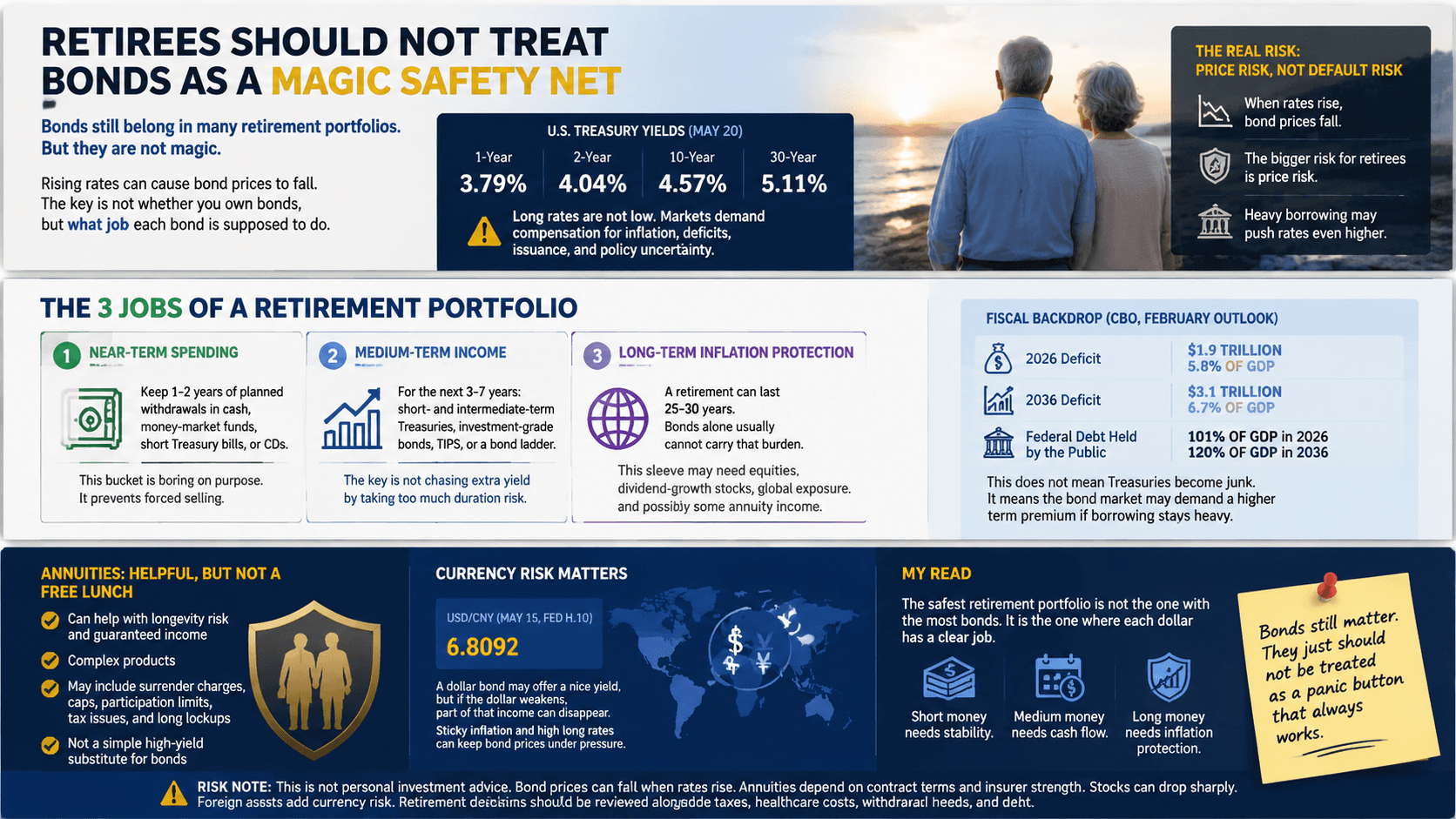

Retirees Should Not Treat Bonds as a Magic Safety Net

Bonds still belong in many retirement portfolios.

But they are not magic.

That is the part many investors learned the hard way after rates moved higher. The old idea was simple: stocks create growth, bonds keep the portfolio calm. Then rates rose, bond funds fell, and a lot of retirees realized their “safe” bucket could still lose money.

So the better question is not whether retirees should own bonds.

The better question is: what job is each bond holding supposed to do?

If the money is needed in the next one or two years, it probably should not be sitting in a long-duration bond fund. That money is spending money. Its job is stability, not heroic return.

Treasury data on May 20 showed the curve still carrying real pressure: 1-year at 3.79%, 2-year at 4.04%, 10-year at 4.57%, and 30-year at 5.11%. Long rates are not low. Markets are still demanding compensation for inflation, deficits, issuance, and policy uncertainty.

That matters for retirees because the risk is not just default risk.

The bigger problem is price risk.

CBO’s February outlook added the fiscal backdrop. It projected a $1.9 trillion federal deficit in fiscal 2026, equal to 5.8% of GDP. By 2036, the deficit is projected to reach $3.1 trillion, or 6.7% of GDP. Federal debt held by the public is projected to rise from 101% of GDP in 2026 to 120% in 2036.

That does not mean Treasuries suddenly become junk.

It does mean the bond market may keep asking for a higher term premium if Washington keeps borrowing heavily.

For retirement planning, I would separate the portfolio into three jobs.

First: near-term spending. Keep one to two years of planned withdrawals in cash, money-market funds, short Treasury bills, or CDs. This bucket is boring on purpose. It prevents forced selling.

Second: medium-term income. For the next three to seven years, short- and intermediate-term Treasuries, investment-grade bonds, TIPS, or a bond ladder can make sense. The key is not chasing a little extra yield by taking too much duration risk.

Third: long-term inflation protection. A retirement can last 25 or 30 years. Bonds alone usually cannot carry that burden. This sleeve may need equities, dividend-growth stocks, global exposure, and possibly some annuity income.

Annuities can help, but they are not a free lunch.

FINRA warns that annuities can be complex. Indexed and variable annuities may include surrender charges, caps, participation limits, tax issues, and long lockups. They can be useful for longevity risk and guaranteed income, but they should not be sold as a simple high-yield substitute for bonds.

For investors outside the U.S., currency risk also matters.

Fed H.10 data showed USD/CNY at 6.8092 on May 15. A dollar bond may offer a nice yield, but if the dollar weakens, part of that income can disappear in FX translation. If U.S. inflation stays sticky and long rates remain high, longer-duration bond prices may also stay under pressure.

My read: the safest retirement portfolio is not the one with the most bonds.

It is the one where each dollar has a clear job.

Short money needs stability. Medium money needs cash flow. Long money needs inflation protection.

Bonds still matter.

They just should not be treated as a panic button that always works.

Risk note: this is not personal investment advice. Bond prices can fall when rates rise. Annuities depend on contract terms and insurer strength. Stocks can drop sharply. Foreign assets add currency risk. Retirement decisions should be reviewed alongside taxes, healthcare costs, withdrawal needs, and debt.