PVH's Quarter Says Tariff Refunds Are An Apparel Treasury Story

TL;DR: PVH's first-quarter 2026 results were good enough to sound like a normal apparel beat: revenue rose to $2.025 billion, direct-to-consumer sales grew, and inventory fell 5%. The more useful read is less flattering and more interesting. PVH is showing how much fashion earnings now depend on customs math, shipment timing, and treasury discipline rather than a clean consumer rebound.

The tell sits in management's new full-year outlook. PVH still expects about 8.8% non-GAAP operating margin, even after saying the prolonged Middle East conflict is pressuring EMEA demand, because the company now expects about $100 million of IEEPA tariff refunds to hit in the second quarter. That is not a fashion trend. That is a treasury event.

By the third paragraph, the implication is clear: investors should stop treating tariff refunds as a one-line windfall and start treating them as a temporary operating bridge. They can protect margin, keep marketing and e-commerce spending alive, and buy time for inventory productivity. They do not prove the underlying apparel machine is suddenly easy again.

#The Quarter Looked Better Than The Mall

PVH did enough real work to earn some credit. First-quarter revenue rose 2% to $2.025 billion, direct-to-consumer revenue increased 6%, owned digital commerce rose 11%, and inventory ended the quarter down 5%. Calvin Klein's underwear and denim categories and Tommy Hilfiger's sweaters and outerwear were specifically called out as areas of strength.

That is the surface story. It says the brands are still alive, stores and e-commerce are still functioning, and the company is not buried in excess product.

But the constant-currency view is less cheerful. Wholesale revenue fell 6% on a constant-currency basis, EMEA demand weakened, and management explicitly said the business is balancing stronger brand momentum against a harder macro backdrop. That is not the profile of a company cruising on broad-based demand.

#The Real Relief Came From Customs

This is where the quarter becomes useful.

PVH said its full-year tariff assumptions still include a gross EBIT hit of about $195 million from tariffs on goods coming into the U.S., plus mitigation actions that only partially offset the damage. Then it added the crucial line: the outlook now includes roughly $100 million of tariff refunds, expected to be recognized in the second quarter, worth about 100 basis points of operating margin support and about $1.70 per share.

That means the margin defense is not coming from one magic fix. It is coming from a stack:

- tariff mitigation actions;

- lower product costs and mix help;

- tighter inventory productivity;

- and a refund line that gives the P&L breathing room.

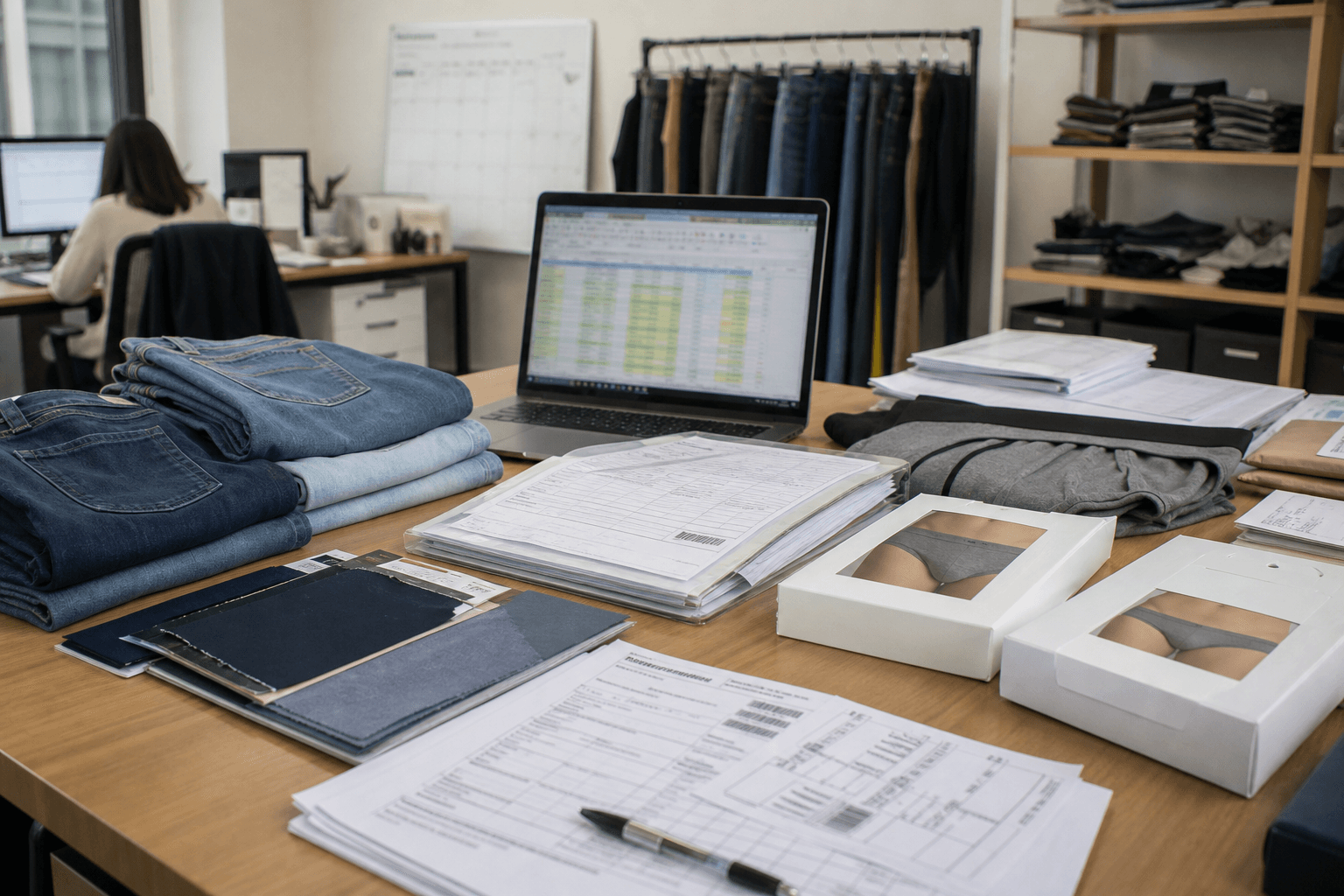

The scene to picture is not a runway show. It is a merchandising table with denim samples, customs paperwork, shipping schedules, and a finance team deciding how much margin can be protected without choking demand. In apparel, gross margin is increasingly being negotiated in logistics and tax files before it is celebrated in a store comp.

#Why The Refund Matters So Much

A $100 million refund matters because it keeps other choices open. It lets PVH absorb some external pressure from EMEA weakness, maintain brand investment, and avoid overreacting with blunt cost cuts that could weaken the brands later.

That is valuable. It is also temporary.

#This Is A Treasury Story, Not A Fashion Story

If you only read the headline beats, you might conclude PVH has already solved the tariff problem. The company's own release argues for a narrower interpretation.

Gross margin was flat at 58.6%, and PVH said the quarter still absorbed higher U.S. tariffs and a more promotional environment. The company offset that with mitigation, lower product costs, and favorable mix. In other words, the machine held together, but it held together through operating discipline, not through a suddenly forgiving consumer.

That distinction matters because fashion investors often overread any quarter where inventory is down and direct-to-consumer is up. Those are good signs, but they can coexist with a fragile earnings structure. If a big part of your annual protection comes from refunds tied to already-paid tariffs, you are borrowing stability from the calendar.

#What The Market May Be Missing

The overlooked risk is not that PVH made a bad quarter look good. The risk is that investors may treat a bridge as a floor.

Refunds can smooth a year. They cannot permanently solve wholesale softness, regional demand pressure, or the need to keep product, marketing, and channel investments aligned. Once the refund is recognized, the business still has to earn the next dollar the old-fashioned way.

#What Investors Should Watch Next

The next important question is not whether Calvin Klein denim or Tommy sweaters had one good quarter. It is whether PVH can keep inventory productive and direct-to-consumer momentum healthy after the refund benefit passes through.

Three signals matter most:

- whether wholesale weakness stays a timing issue or becomes a deeper demand problem;

- whether EMEA pressure spreads into a wider profitability drag;

- whether tariff mitigation and sourcing discipline can keep doing real work once the refund tailwind is gone.

If those hold, PVH's quarter will look like proof of a sturdier operating model.

If they do not, this quarter may end up looking like a well-managed customs reprieve.

#FAQ

Did PVH raise its 2026 margin outlook?

No. PVH kept its full-year non-GAAP operating margin outlook at about 8.8%, but the composition changed because tariff refunds now help offset macro pressure in EMEA.

Why are tariff refunds such a big deal for an apparel company?

Because they do not just add accounting profit. They can fund brand spending, protect near-term margin, and reduce the need for harsher inventory or pricing actions while management adjusts sourcing, shipments, and promotions.