Kpler's $1 Billion Check Says Commodity Data Is Workflow Infrastructure

TL;DR: Sixth Street's investment of more than $1 billion into Kpler is easy to file under "another data-company funding round." That misses the business point. When private capital uses preferred equity to back a company that tracks ships, cargoes, power flows, and commodity movements in real time, it is effectively saying the expensive thing is not the dataset by itself. The expensive thing is making a trading, hedging, procurement, or credit decision too late.

The sharper read is that commodity intelligence is starting to be financed like workflow infrastructure. Reuters reported the deal values Kpler at more than $3.7 billion and was structured as preferred equity, which gives Sixth Street downside protection if the valuation slips while preserving upside if the company keeps growing. That is not the posture of someone buying a nice information service. It is the posture of someone financing a tool that sits close to real money decisions.

#The Desk That Actually Matters

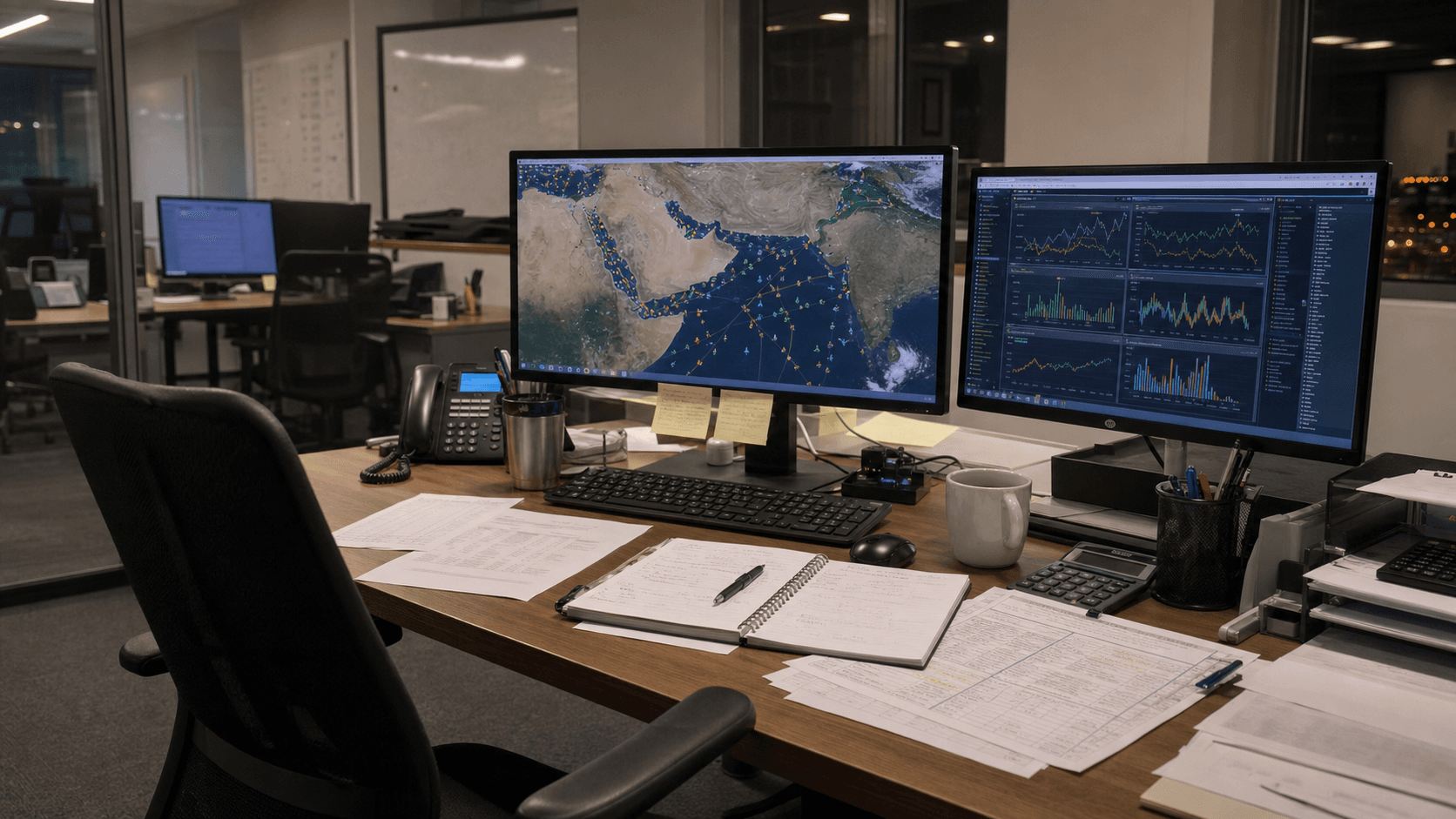

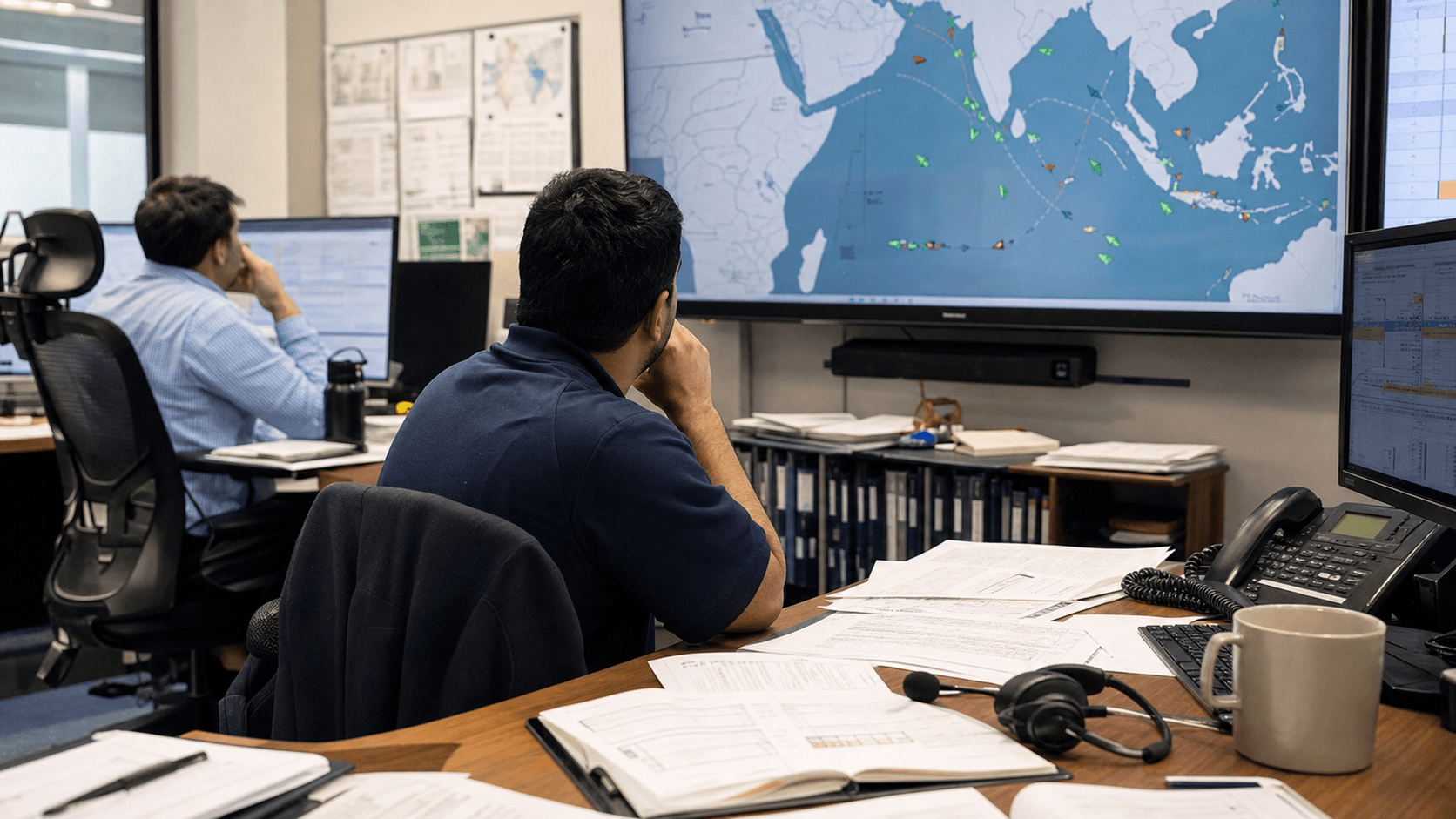

Picture the scene that matters here. Not a glamorous macro chart. A trader, scheduler, or risk manager staring at a vessel screen, a cargo estimate, and a note about whether a refinery outage, sanctions risk, or port congestion just changed the economics of the next move.

That is where Kpler lives. The company says it covers more than 40 markets across commodities, power, dry bulk, and maritime transport. On its own site, Kpler frames itself as the "definitive intelligence platform for global physical trade" with 1.3 billion-plus AIS signals per day and more than 255,000 proprietary sources.

The distinction matters because physical markets punish delay differently from ordinary software categories.

- If a CFO gets a budgeting dashboard late, the pain is usually annoyance.

- If a crude trader, shipping desk, utility buyer, or commodity lender gets location or flow intelligence late, the pain can show up in basis risk, inventory mistakes, hedging errors, or bad credit judgment.

That is why this deal feels more like infrastructure financing than a classic growth-equity round.

#Why Preferred Equity Is The Tell

The preferred-equity structure is the giveaway. Reuters said the security gives Sixth Street priority over common holders and includes downside protection if Kpler's valuation falls, while still preserving upside participation. That is a financing shape you use when the asset is attractive, but you still want to respect execution risk.

In plain English, Sixth Street appears to be saying two things at once.

- This company is strategically important enough to back at scale.

- This company is still operating in a market where valuation discipline matters.

That is a healthy combination. It suggests the new scarcity in data is not "AI can summarize PDFs." The scarcity is owning proprietary, operationally messy, hard-to-recreate inputs that plug directly into workflows where a mistake costs real money.

#Why that matters for investors

A lot of AI-era valuation talk still treats data as generic model fuel. But Kpler is closer to a toll road than a textbook data vendor. The user is not paying just to know something interesting. The user is paying to reduce decision latency in businesses where timing and physical positioning change cash outcomes.

That is also why Reuters' framing that buyers are paying up for high-quality proprietary datasets that can support AI and automated decision-making matters. The workflow comes first. AI is the amplifier, not the core product.

#Kpler Has Been Building The Stack, Not Just The Screen

Kpler did not arrive here by staying narrow. The company says it was founded in 2014, started in LNG, and then expanded into oil, dry bulk, power, defense intelligence, and maritime. It also says it hit $100 million in annual recurring revenue in January 2024, after a run of acquisitions including ClipperData, JBC Energy, COR-e, MarineTraffic, FleetMon, and ChartDesk.

More recently, Kpler used M&A again. Its May 20 press release on acquiring CITAC described the deal as a way to deepen on-the-ground coverage in African energy markets. That is the pattern to watch.

Kpler is not merely collecting more rows of data. It is buying visibility into places where markets remain fragmented, opaque, and operationally difficult. In physical trade, that kind of visibility is often more valuable than another layer of polished interface.

#The hidden business-model shift

The real shift is that customers increasingly buy this kind of product the way they buy mission-critical workflow.

- Traders use it to position risk.

- Lenders use it to judge exposures.

- Logistics teams use it to reroute around disruption.

- Governments use it to watch sanctions, supply security, and defense-related flows.

Once a product sits in those loops, churn should not be benchmarked against ordinary software convenience. It should be benchmarked against the cost of flying blind.

#The Twist Is That This Is Also A Credit Story

That is the part I think casual readers are missing. A preferred-equity check into a trade-intelligence company is also a quiet credit-market opinion on where durable pricing power lives.

The market has spent two years obsessing over AI chips, power connections, and data-center leases. Fair enough. But the businesses that tell money where goods are moving, where cargoes are delayed, or where compliance risk is hiding may turn out to have a cleaner commercial position than many flashy model wrappers.

If you own a scarce workflow in a market where every bad decision is expensive, customers do not evaluate you like an optional research subscription. They evaluate you like operating equipment.

#FAQ

What happened in the Kpler deal?

Kpler announced on June 3, 2026 that it secured more than $1 billion of minority growth equity from Sixth Street. Reuters separately reported the transaction values Kpler at more than $3.7 billion and uses a preferred-equity structure.

Why does a commodities-data deal matter to U.S. investors?

Because it shows where private capital thinks pricing power sits. Tools that reduce trading, inventory, logistics, and compliance mistakes in physical markets can become embedded operating infrastructure, not just another software expense line.

Is this mainly an AI story?

Only partly. AI helps organize and automate interpretation, and both Reuters and Kpler point to AI as part of the value proposition. But the more durable moat is the proprietary, workflow-ready data feeding real-time decisions in energy, shipping, trade, and credit.