Fed Beige Book Shows The Consumer Margin Squeeze Is Now An Operating Problem

TL;DR: The Federal Reserve's June 3, 2026 Beige Book says the U.S. economy is still growing, but the useful signal is narrower: consumer-facing businesses are absorbing higher fuel, shipping, packaging, grocery, and financing costs while many customers are trading down or delaying purchases. The business implication is not a clean recession call. It is a margin squeeze that moves slowly through retailers, auto dealers, banks, and suppliers before it shows up as one dramatic headline.

##What The June 2026 Fed Beige Book Actually Shows

The June 3 Federal Reserve Beige Book is easy to read as a bland "still growing" update. Ten of the twelve Federal Reserve Districts reported slight to moderate growth, one reported no change, and one reported a slight decline.

That is the wrong place to stop.

The sharper point is that the growth is getting more expensive to hold together. The Beige Book describes mixed consumer spending, a wider split between higher-income and lower-income households, more credit card usage, fewer retail visits, and stronger demand for necessities.

That combination matters because it changes where the pressure lands. It is not only the household that feels the bill. The merchant feels it too.

##Why This Is A Margin Story, Not Just A Consumer Story

The Beige Book says prices rose at a moderate to strong pace overall, with energy-related costs spilling into shipping, packaging, groceries, and fertilizer. It also says non-labor input costs continued to rise faster than selling prices.

That is the mechanism investors should care about.

When a store's freight bill rises, the clean textbook answer is to raise prices. But if the customer is already cutting trips, leaning on credit cards, and buying more necessities, the store cannot simply pass along every cost increase without losing volume.

So the business has a short list of bad choices:

- Raise prices and risk weaker traffic.

- Absorb costs and protect traffic at the expense of margin.

- Reduce assortment, service, hours, or promotions.

- Push suppliers harder and move the squeeze upstream.

None of those choices looks dramatic on day one. They show up as a few basis points of gross margin, slower inventory turns, a more cautious hiring plan, or a credit officer asking why delinquencies are ticking higher.

#Why Cost Pass-Through Is Becoming Uneven

The Beige Book is useful because it separates demand by income. Higher-income households were still more resilient, while middle- and lower-income consumers were more visibly strained.

That makes pricing power less universal than a headline inflation number suggests. A premium travel company may still be able to charge. A grocery chain, dollar store, regional restaurant operator, or used-car dealer has to watch the customer much more closely.

The market often talks about "the consumer" as one balance sheet. Operators do not have that luxury. They see the split at the checkout line, the service counter, and the finance desk.

##Where The Pressure Shows Up First

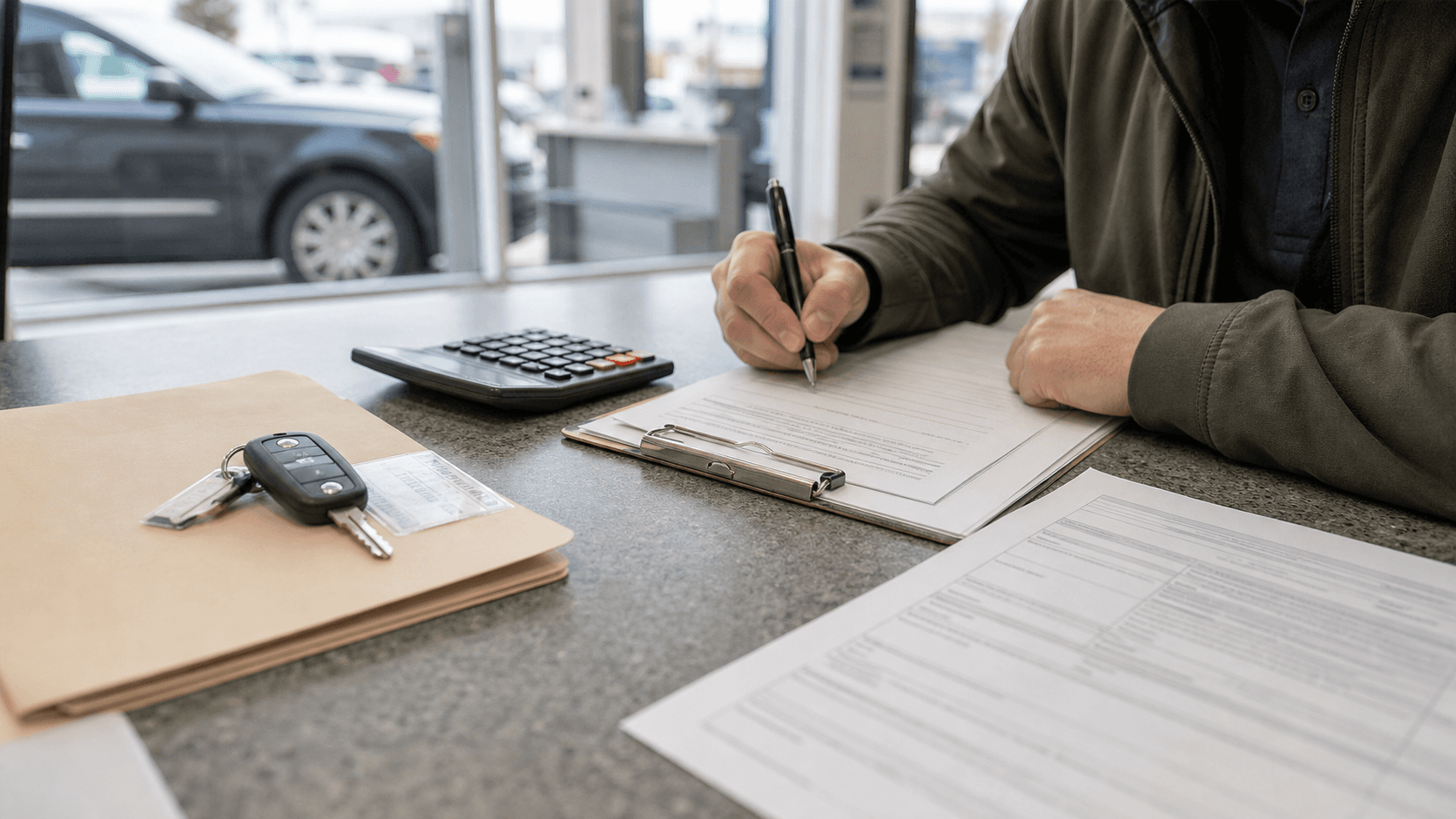

One concrete scene in the Beige Book is the auto lot.

The Fed report says auto dealers saw softer new-vehicle demand tied to affordability and fuel costs, while customers substituted toward used and hybrid vehicles. In the Boston District detail, New Hampshire used-auto sales faced headwinds from high financing and insurance costs, and repair activity was hurt by rising repair costs.

That is not just an auto story. It is a consumer-cash-flow story with several toll booths.

The buyer may still need a car. But the monthly payment, insurance quote, repair estimate, and fuel bill all compete for the same paycheck. A dealer can advertise a discount, yet the customer may still walk away because the all-in ownership cost no longer works.

For banks and lenders, the same scene becomes a credit-quality question. The Beige Book notes that residential mortgage, consumer, and agricultural loan delinquencies were rising in several districts. That does not mean a credit cycle has broken. It means lenders have fewer reasons to treat household strain as purely temporary.

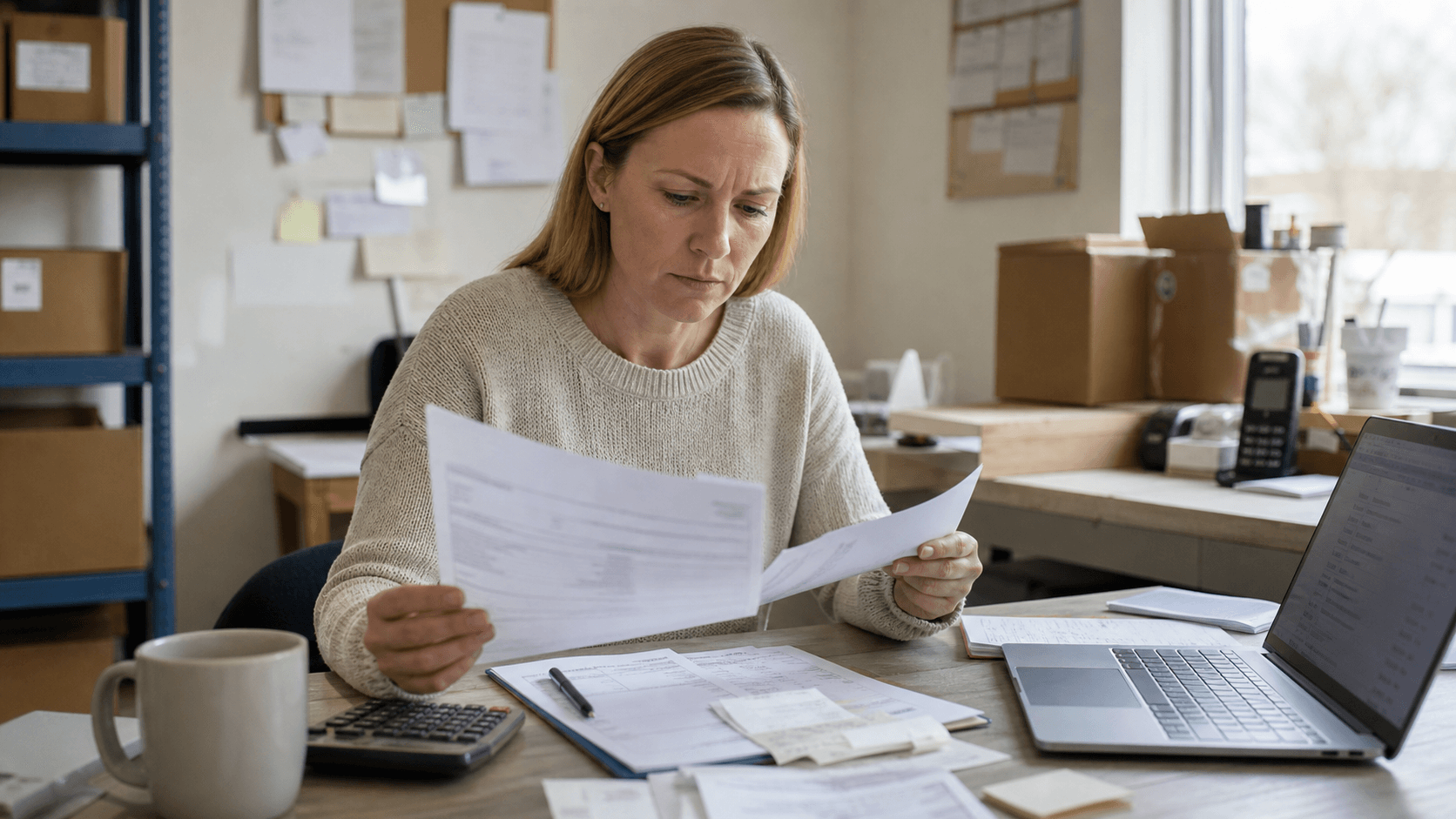

#The Small-Business Desk Is The Better Dashboard

The better dashboard is not a stock chart. It is a small-business manager's desk with invoices, a payroll spreadsheet, a delivery bill, and a pricing sheet open at the same time.

If fuel and shipping rise faster than the price a customer will tolerate, the manager has to decide what to protect: traffic, margin, staff hours, inventory depth, or delivery speed.

That is where macro data becomes operating reality.

##Who Benefits If The Squeeze Persists

The winners are not automatically the companies with the most growth. They are the companies with the most room to choose.

Large retailers with strong private-label programs can rework assortment. Insurers and lenders with better risk selection can reprice faster. Manufacturers tied to defense spending and data centers may face a different demand curve than a consumer discretionary seller. The Beige Book even notes manufacturing strength in several districts, helped by defense-related activity and data center demand.

The weaker position belongs to businesses that need customer traffic but have little control over input costs. That includes parts of restaurants, regional retail, smaller distributors, low-end auto finance, agriculture suppliers, and any operator carrying inventory into uncertain demand.

This is the hidden investment issue: a company can report stable sales while its operating flexibility is quietly shrinking.

##What Investors Should Watch Next

The June Beige Book does not hand investors a single trade. It hands them a filter.

Watch companies that can explain the following without hiding behind vague "macro uncertainty":

- Which costs are rising fastest: freight, energy, insurance, labor, financing, or shrink.

- Whether prices are rising because demand is strong or because costs leave no choice.

- Whether lower-income customers are trading down, buying less, or switching channels.

- Whether credit losses are still normalizing or starting to change underwriting behavior.

The point is not to call the economy strong or weak from one Fed survey. The point is to notice that growth with shrinking pass-through power is a different animal from growth with pricing power.

That is the part of the Beige Book worth underlining. The squeeze does not need to be loud to matter.

#FAQ

Why does the June 2026 Beige Book matter for investors?

It connects consumer strain to company margins. The report shows that some businesses face higher input costs while customers are already more selective, which can pressure profitability before revenue visibly breaks.

Is this a recession signal?

Not by itself. The Beige Book still described growth in most Federal Reserve Districts, but it also showed uneven consumer demand, rising costs, and some delinquency pressure.

Which sectors are most exposed?

Consumer-facing retailers, auto dealers, restaurants, lenders, agriculture-linked businesses, and smaller distributors are most exposed when fuel, financing, insurance, and shipping costs rise faster than customers will accept price increases.