The Consumer Is Splitting Into Two Balance Sheets

The easiest way to get confused by the U.S. economy right now is to assume there is still one consumer.

There is not. There are at least two balance sheets walking around in the same country. One lives at the gas pump, the grocery aisle, and the monthly card statement. The other lives inside a 401(k), an index fund, and a home that still looks expensive on paper. That split is why consumer confidence can sag, two-thirds of households can say they are cutting back, and the S&P 500 can still be setting records in the same week.

That is not just a mood contradiction. It is a business model map.

On Tuesday, the Conference Board said its consumer confidence index dipped to 93.1 in May from 93.8 in April. The present-situation measure fell harder. The share of people saying jobs are plentiful slipped to 25.5%. Two-thirds of consumers said rising prices were making them cut back overall, mostly by buying fewer items and delaying bigger purchases. At the same time, Wall Street pushed the S&P 500 and Nasdaq to fresh highs as the AI trade kept pulling capital toward semis and big tech.

Those are not competing headlines. They belong together.

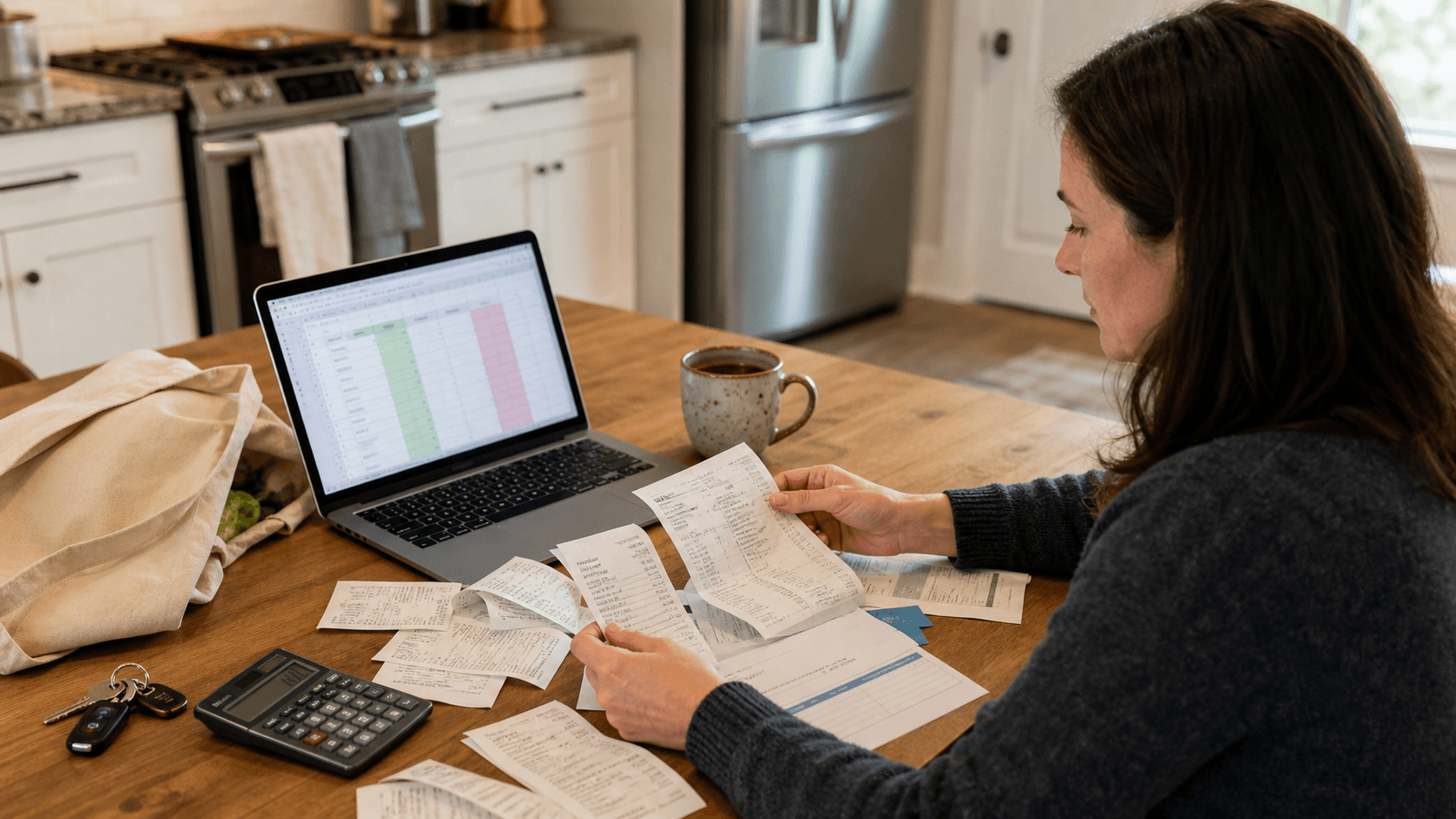

If you want a concrete scene, start with a kitchen table. A household is sorting grocery receipts, looking at a gas bill, and deciding which purchase can wait another month. That is the cash-flow consumer.

Then move one room over. On the same day, the retirement app on the phone shows another green week because Micron just joined the trillion-dollar club and the tech-heavy indexes keep climbing. That is the asset consumer.

The mistake is to average those two people together and call it "the consumer."

For investors and operators, the more useful question is which balance sheet your business is actually exposed to.

Some companies are still tethered to wallet stress. They need the paycheck consumer to feel loose enough to buy one more basket, approve one more repair, or absorb one more price increase. Those businesses should read the May confidence data as a warning that the low-end cushion is getting thinner.

Other companies are increasingly tied to the asset consumer instead:

- Card networks and payments rails collect on nominal spending even when households trade down.

- Large retailers can offset fragile basket economics with ads, memberships, delivery, and marketplace fees.

- Insurers, brokers, and wealth platforms can benefit from asset inflation even when household sentiment sounds miserable.

- Mega-cap tech keeps attracting capital because investors treat AI spending less like a cyclical splurge and more like a toll road to future earnings power.

That is why broad "consumer strength" commentary keeps missing the point. The market is no longer paying for a single clean story about household demand. It is paying for exposure to whichever layer of the household balance sheet still has pricing power.

This also helps explain why confidence surveys feel weak without immediately producing a market crack.

The people cutting clothing purchases, delaying hobby spending, and hesitating on discretionary buys are real. They matter a lot for merchants, restaurants, travel tiers, and lenders exposed to thinner savings buffers. But they do not have to be the same people setting the marginal price of the S&P 500. That price is being set by flows into a narrow set of businesses that benefit from AI capex, market concentration, and asset-price resilience.

In other words, the stock market is not ignoring the consumer. It is choosing which consumer counts.

That has two business consequences.

First, executive teams should stop treating confidence data as a simple top-line demand signal. It is now a mix of cash-flow strain, asset inflation, and category-specific postponement. A company selling essentials may still hold up. A company selling financed wants may be walking into a harder summer than the index suggests.

Second, investors should get more precise about what "defensive" means. In this environment, defense is not just cheap staples or old-school bonds. It can mean owning toll collectors on constrained behavior: processors, platforms, distributors, and companies that make money when households optimize, not just when they splurge.

The twist is that this split can make the economy look healthier from the top down than it feels from the checkout line.

That usually lasts longer than skeptics expect. It also breaks faster than index charts imply once asset prices stop doing the emotional heavy lifting for upper-income households.

So when two-thirds of Americans say they are cutting back while the market prints highs, I do not hear a recession call. I hear a more uncomfortable question: how many public companies are really selling to the paycheck consumer, and how many are just renting the asset consumer's optimism for one more quarter?