The Consumer Economy Is Becoming a Delay Economy

The most important consumer story in America right now is not that people feel bad. It is that they are learning to delay.

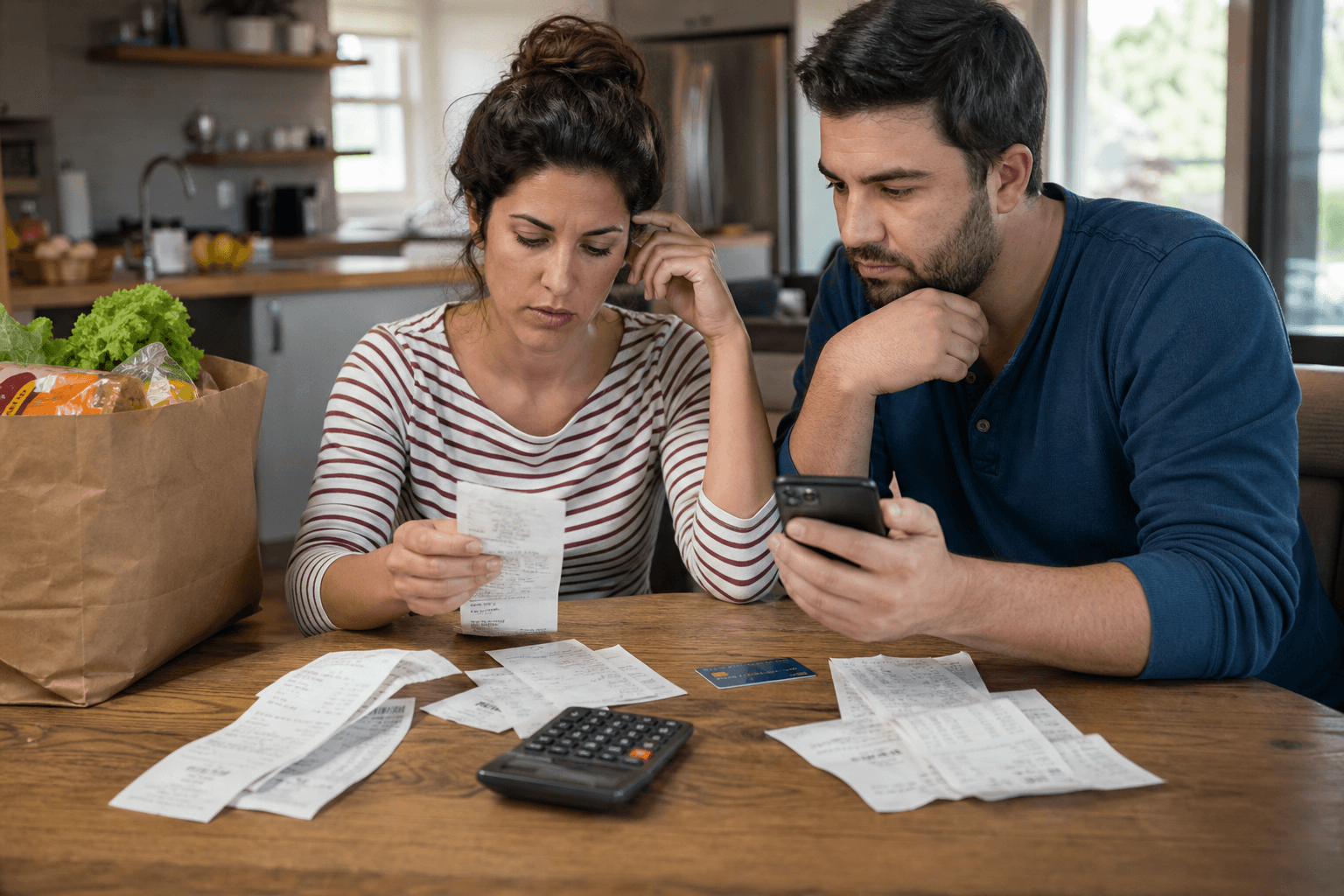

That sounds softer than a recession call, but for business it may matter more. A customer who stops buying is one problem. A customer who keeps showing up while constantly editing the basket, pushing out big purchases, and reordering the monthly budget around gas, groceries, and bills is a different problem. That kind of customer can keep headline spending alive while quietly wrecking margins, product mix, and forecasting.

The new Conference Board reading captured the split neatly. Consumer confidence slipped to 93.1 in May from 93.8 in April. That is not a collapse. But it came with a more telling detail: two-thirds of respondents said higher prices were making them cut back, and many said they were delaying larger purchases.

That is the part too many market takes miss. This is no longer just an argument about whether the consumer is "resilient." It is an argument about what kind of consumer is left.

Picture the scene. A driver stares at a pump showing roughly $4.49 a gallon, up sharply from just under $3 before the late-February Middle East shock. Then that same household walks into a store or opens a shopping app already knowing something else has to give. Maybe it is shoes. Maybe toys. Maybe the extra cart item that used to feel harmless.

Businesses built for that extra item should be nervous.

The AP's report on the survey had another useful detail: confidence rose among households earning at least $100,000 and fell for most others. That matters because it explains why the stock market and the mall can send opposite signals on the same day. Asset owners can keep spending and keep buying stocks. Everyone else starts acting like a part-time procurement officer in their own kitchen.

This is why I think the real consumer trade is shifting away from broad demand calls and toward budget control.

Winners in this environment are not simply the cheapest brands or the fanciest brands. They are the businesses that insert themselves into the budgeting workflow:

- The retailer that becomes the default refill trip, not the aspirational splurge.

- The platform that helps a household smooth cash flow, compare prices, or postpone pain.

- The merchant that can protect margin even when the basket gets smaller and more deliberate.

Losers are the businesses still assuming the consumer decision starts with desire. In a delay economy, the decision starts with subtraction.

The labor market is adding to the tension. The share of consumers saying jobs are plentiful fell to 25.5%, the lowest in three years. At the same time, only 18.6% said jobs were hard to get, which sounds healthy until you realize what it implies: this is a low-fire, low-hire market. People may still have work, but fewer feel confident enough to behave loosely.

That psychology can hit revenue before it hits payrolls.

You can already see the outlines in the official data. Inflation accelerated to 3.8% in April, the highest in three years. Real average hourly earnings shrank from a year earlier for the first time in three years. Adjusted for inflation, retail sales declined in April after a stronger March. None of those numbers alone says crash. Together they say households are losing room.

That is a very different setup from the old bull case that consumers will either keep spending or suddenly break. The middle zone is the dangerous one. A household can keep spending enough to prevent a clean recession signal while becoming far more selective, promotional, and timing-sensitive. That is poison for businesses that depend on impulse, premium add-ons, and forgiving price tolerance.

It also means investors should stop treating "consumer resilience" as one trade. There are at least three:

- Traffic businesses that monetize necessity, repeat visits, or refill behavior.

- Budget intermediaries such as payments, lending, and software products that help households manage timing.

- Discretionary sellers that need emotional momentum and full-price confidence.

Those three businesses will not live in the same economy, even if Washington reports one.

The twist is that a delay economy can flatter top-line stability for longer than bears expect. People do not disappear. They optimize. They trade down, wait, defer, split the purchase, or buy one item instead of three. That keeps activity visible enough for optimistic headlines while pushing pain deeper into mix, margin, and planning.

So I would watch fewer sentiment charts and more evidence of budget choreography: refill frequency, deferred big-ticket purchases, payment-plan usage, promotional intensity, and which companies are becoming part of the household control panel.

When two-thirds of consumers say they are cutting back, the biggest opportunity may not be selling them more. It may be owning the moment when they decide what to cut.